Paradoxes of energy dominance. European military Keynesianism. Champagne in trouble.

Great links, images, and reading from Chartbook Newsletter by Adam Tooze

Thank you for opening your Chartbook email.

Germaine Richier La Chauve-souris, 1955

The trouble with energy dominance

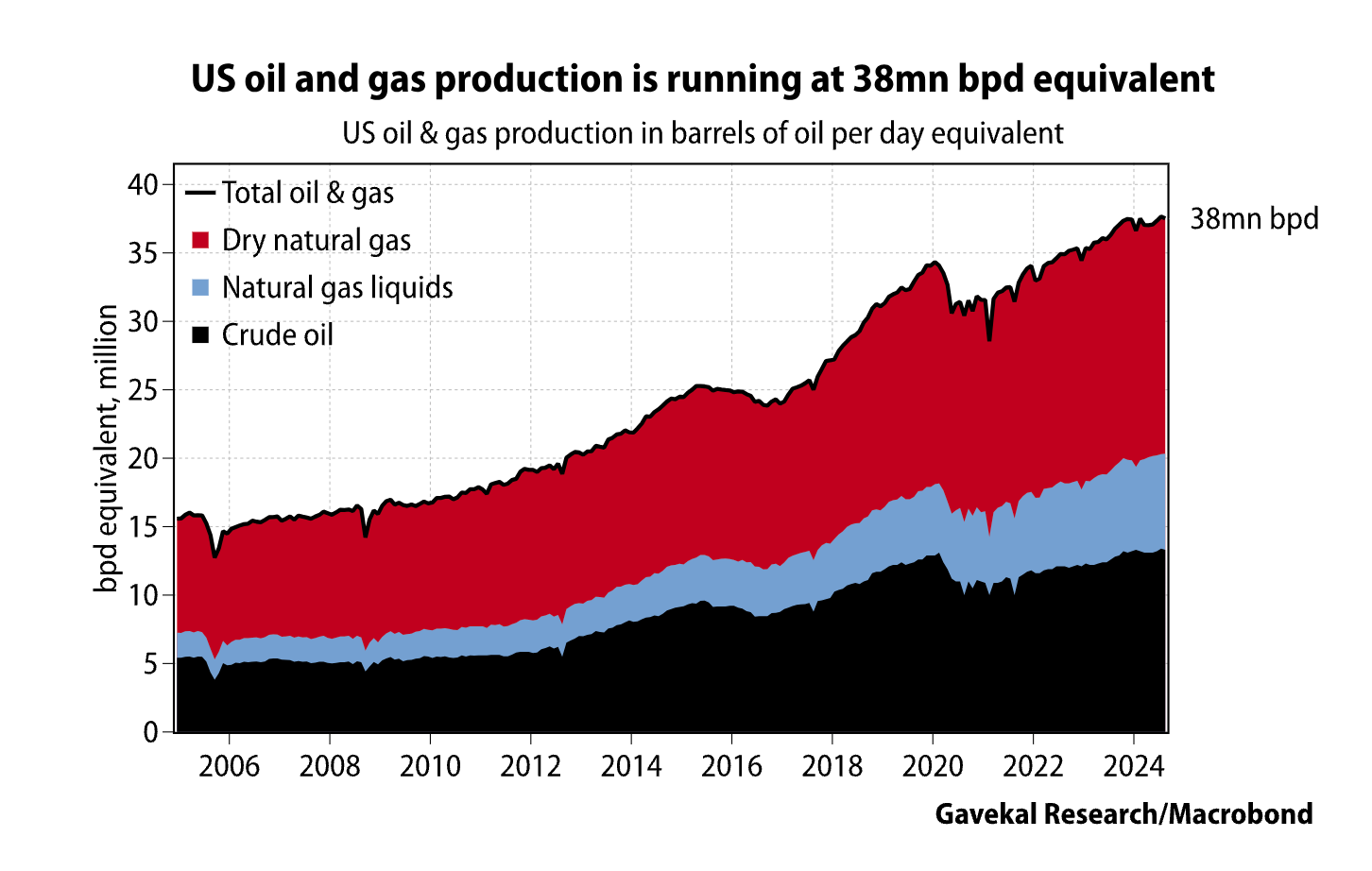

Incoming Treasury secretary Scott Bessent has talked of targeting an energy production increase equivalent to 3mn barrels of oil a day, while the Trump team has talked of achieving prices of US$50/bbl for oil and US$2/gal at the pumps for gasoline. With US crude oil production currently running close to record levels at 13.5mn bpd, at first an expansion of 3mn bpd sounds highly ambitious. It would be as much as US crude production has grown over the last seven years. But when you also factor in US production of natural gas liquids and dry natural gas, US oil and gas producers are currently pumping the equivalent of 38mn bpd of oil. In those terms, an extra 3mn bpd looks eminently attainable. It is equal to the production growth recorded in the last two years.

So it is quite feasible that over the next two or three years US producers could boost their oil and gas output by the targeted 3mn bpd equivalent. But it does not follow that this production increase would result in substantially lower energy prices for US consumers, especially if Trump’s administration vigorously pursues its other aim of global energy dominance. … drilling new wells is profitable at an oil price of US$62/bbl or a natural gas price of US$3.69/MMBtu. So, with WTI at US$76/bbl, drilling for oil is modestly profitable. And with natural gas at US$3.75/MMBtu, drilling for gas is barely breaking even. It is little surprise, therefore, that producers are not focusing on drilling new wells, but on wringing greater productivity out of their existing operations. To substantially increase their drilling, producers say they would need to see WTI averaging US$84/bbl, and natural gas at an average US$4.66/MMBtu.

Source: Research Gavekal

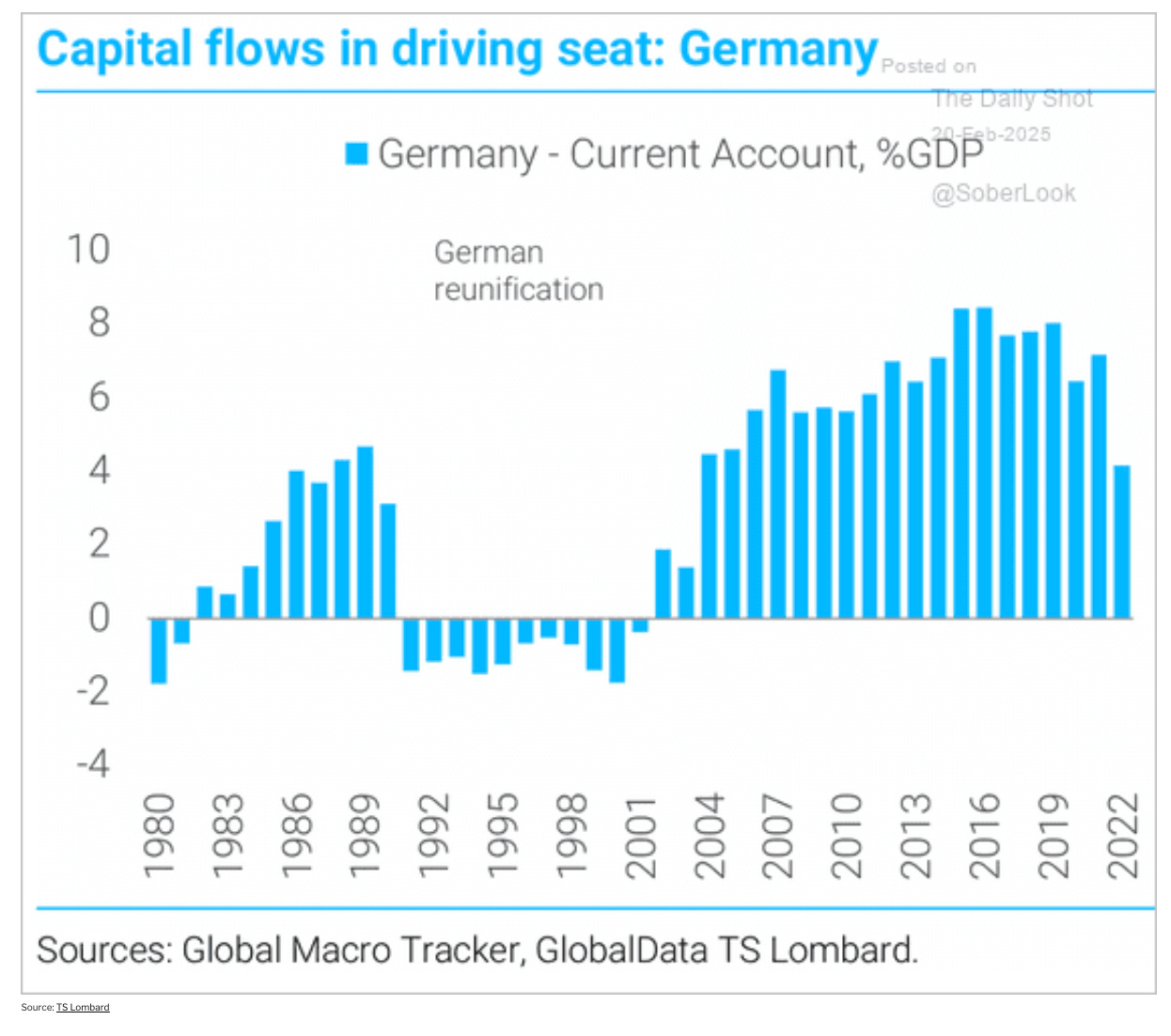

How Germany’s current account flips from surplus to deficit and back again … and no it is NOT a story of competitiveness, but of the macroeconomic balance. In the early 1990s Germany saw a huge boom in investment driven by reunification.

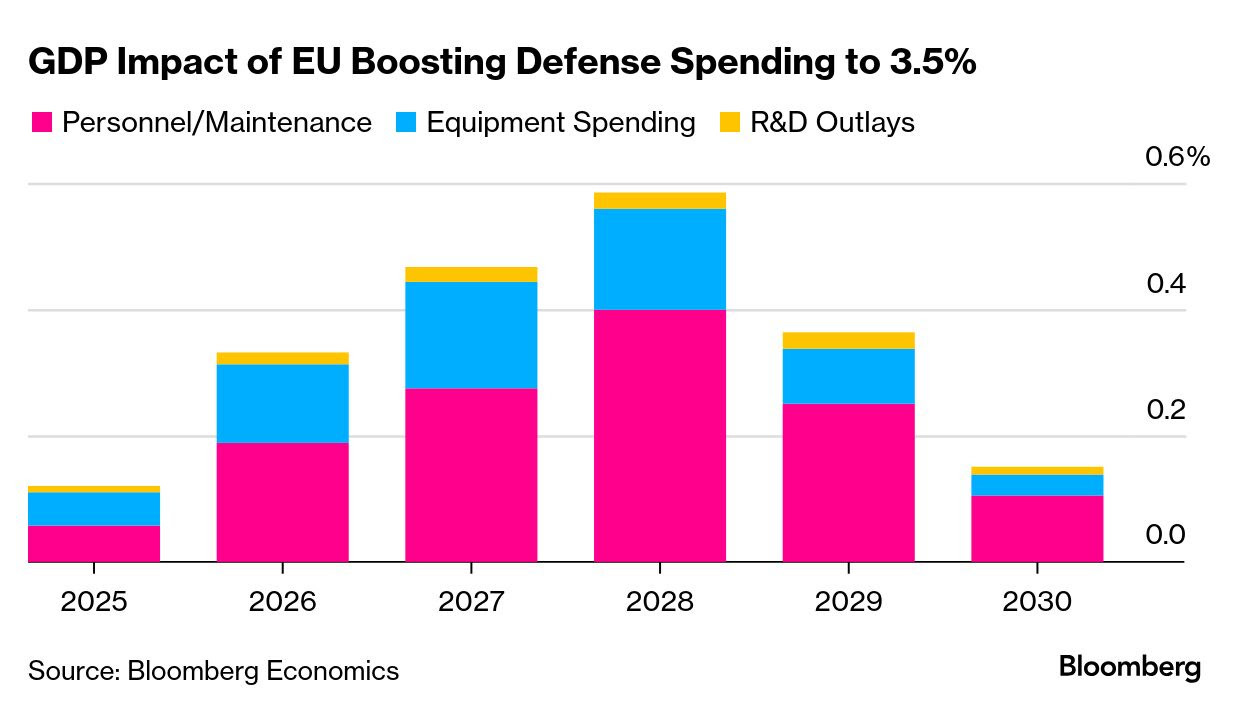

The potential of military Keynesianism for Europe

Jamie Rush, chief European economist at Bloomberg Economics, has mapped out the economic implications of an increase to 3.5% of GDP over the next few years (from about 1.9% in 2024), financed by higher debt sales. He noted that if the spending were funded with tax increases, or cuts in other areas, that could wipe out any positive impact—or worse.

One factor limiting the stimulus to be had from rearmament is that Europe buys much of its military gear from American suppliers. Former European Central Bank President Mario Draghi’s competitiveness report estimated that 78% of purchases come from production outside the EU—and 63% from the US alone. That means any “multiplier” effect of stepped-up spending on growth would be low. What’s more, recruiting more Europeans to the military and defense industry would bring down unemployment, possibly fueling inflationary pressures that would lead to higher interest rates. In all, Rush calculates that EU economic output might be higher by about 0.6% in 2028, “which implies a modest nudge up in GDP growth in the next few years.” See his full note on the Bloomberg terminal here.

But what if the EU increased its own defense-industry production? That could bring the GDP boost closer to 1%, Rush says. Another consideration is that, if other industries are losing jobs, the inflationary impact of a defense build-out may not be so large. Germany’s automobile industry is a case in point. Having fallen behind in global competitiveness, it’s in downsizing mode, with Volkswagen alone envisioning tens of thousands of job losses in coming years. The flipside of that: a pool of skilled workers available for the defense industry. Bloomberg reported on one example last month: radar maker Hensoldt was in talks to hire two full teams from two separate auto-parts suppliers—in one case, involving up to 100 people.

Source: Bloomberg

HEY READERS,

THANK YOU for opening the Chartbook email. I hope it brightens your day.

I enjoy putting out the newsletter, but tbh what keeps this flow going is the generosity of those readers who clicked the subscription button.

If you are a regular reader of long-form Chartbook and Chartbook Top Links, or just enthusiastic about the project, why not think about joining that group? Chip in the equivalent of one cup of coffee per month and help to keep this flow of excellent content coming.

If you are persuaded to click, please consider the annual subscription of $50. It is both better value for you and a much better deal for me, as it involves only one credit card charge. Why feed the payments companies if we don’t have to.

And when you sign up, there are no more irritating “paywalls”

Alan Beattie on the strange story of how a Republican Presidency launched a new phase of American internationalism

For contributing subscribers only.

Germaine Richier (French, 1904-1959) Untitled, c. 1950

King Charles Drops Champagne Brands, Adding Pressure to Luxury Sector

Queen Victoria first made Champagne Lanson an official supplier to the Royal Court of England in 1900. Now, 125 years later, King Charles III has revoked the so-called warrant, and the French producer will soon discover the true economic value underpinning the highly coveted status. Lanson’s absence from the monarch’s wide-ranging list of goods and service suppliers published last month by the Royal Warrant Holders Association came as a surprise to the Champagne house founded in 1760. Luxury conglomerate LVMH’s high-end Krug label and Pernod Ricard SA’s Mumm were also stripped of the distinction, which grants the right to display the coats of arms on bottles and “By appointment to...” as well as reap any financial benefit that comes from the endorsement. A spokeswoman for Lanson acknowledged the decision and declined to comment, as did LVMH. Pernod Ricard said in a statement: “As of this year Mumm is no longer among the list of Royal Warrant holders, but we remain a proud supplier to the royal household with the emblematic Dubonnet.” … Lanson-BCC is listed on the Paris stock market and controlled by Bruno Paillard, who has built up a Champagne empire over four decades, starting with an eponymous brand and then through acquisitions including Lanson and Philipponnat.

Champagne has long held sway over the royal court in the UK, which was the sector’s second-largest export market in 2023 by number of bottles, just after the US. Under King Charles, the bubbly wine makers still comprise about a third of all of the producers of alcoholic drinks granted warrants, dwarfing whisky, gin, port and cognac makers. Six French Champagne labels held on to their royal warrants: Bollinger — first awarded the status in 1884 — Laurent-Perrier, Louis Roederer, Pol Roger, LVMH’s Moet & Chandon and Veuve Clicquot. English sparkling wine maker Camel Valley also got the seal of approval. For Champagne producers that didn’t make the cut, the news is compounded by a worsening downturn, with shipments for the whole sector falling 9.2% last year. In its most recent fiscal year, Pernod Ricard reported a double-digit decline in sales for Mumm. King Charles and Queen Camilla have granted warrants to 542 suppliers so far, significantly less than the 800 or so under Queen Elizabeth II. … The monarchy’s choice of suppliers reflects what is served during official functions and personal tastes. The late Queen was reported to drink a glass of champagne every evening. In 2021, she granted a royal warrant to Dubonnet, which when mixed with gin and lemon was reputed to be her and the Queen Mother’s favorite cocktail. The tipple had its warrant renewed by King Charles.

Source: Bloomberg

Sam Greene on different views of Russian public opinion is highly illuminating.

In the 15 December 2024 TL;DRussia that kicked off this current discussion looked at some Levada Center data that have consistently shown that most Russians do not believe the state is governed in their interests. At the time, I noted in passing that this that trend had begun to shift and promised to return to it. Thus, in the 19 January 2025 edition I did exactly that, suggesting that the a “rally ‘round the flag” effect, driven in this case by the peculiar politics of collective avoidance, had led to a generalized uptick in Russians’ sense of connection with their state and one another. In the process, though, I kicked down the road an obvious follow-up question: if Russians have suddenly started to believe that Putin represents their actual interests, what happens when they stop believing that? That, then, is the focus of this final installment in the TL;DRussia public opinion mini-series. As the kerfuffle over Maria Snegovaya’s Atlantic Council paper on Russian public opinion laid bare, the popular and political discussion of what Russians think and whether it matters what Russians think is fairly dysfunctional, descending easily into acrimony and name-calling, and shedding precious little genuine light on the matter. This dysfunction stems, in my view, from the fact that the loudest voices in this discussion belong to people whose views are based on ideology, rather than analysis. On the one hand, you have those who believe that Russian opinion polls showing consistent support for the war are an accurate reflection of reality not because they have delved deeply into the data and the methodology, but because they are convinced that ordinary Russians are committed imperialists and/or fascists. On the other, you have those who reject such survey results out of hand, likewise not because they have delved deeply into the data and the methodology, but because they are personally and professionally committed to the belief that Russians’ expressed views are more or less exclusively the result of propaganda and repression.\

RICHIER, GERMAINE: Konvolut.

If you’ve scrolled this far, you know you want to click: