I love sending the newsletter for free to tens of thousands of readers around the world. But what sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters, press this button and pick one of the three options.

Several times per week, paying subscribers to the Newsletter receive the full Top Links email with great links, reading and images.

There are three subscription models:

The annual subscription: $50 annually

The standard monthly subscription: $5 monthly - which gives you a bit more flexibility.

Founders club:$ 120 annually, or another amount at your discretion - for those who really love Chartbook Newsletter, or read it in a professional setting in which you regularly pay for subscriptions, please consider signing up for the Founders Club.

To get the full Top Links and become a supporter of Chartbook, click here

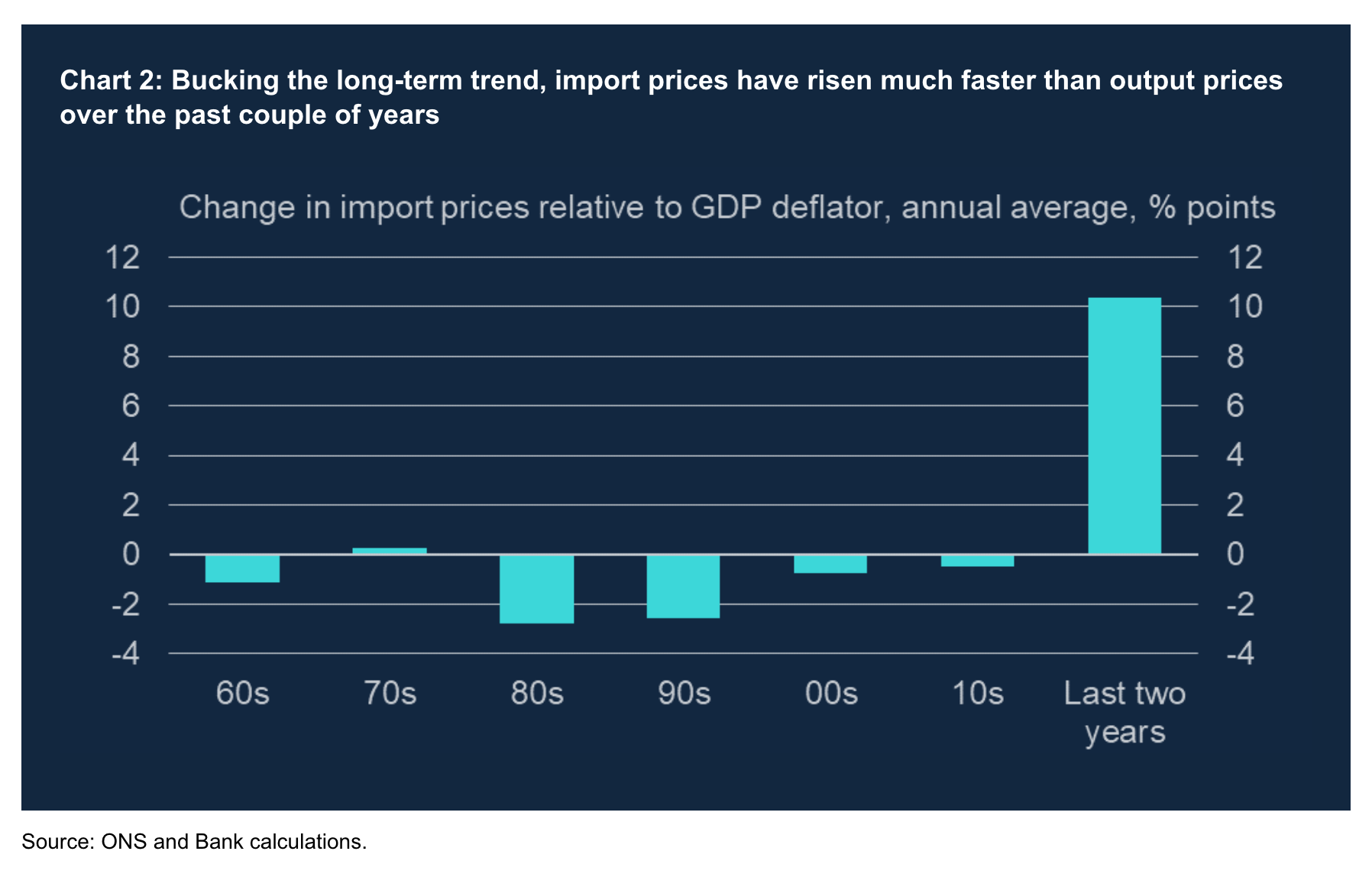

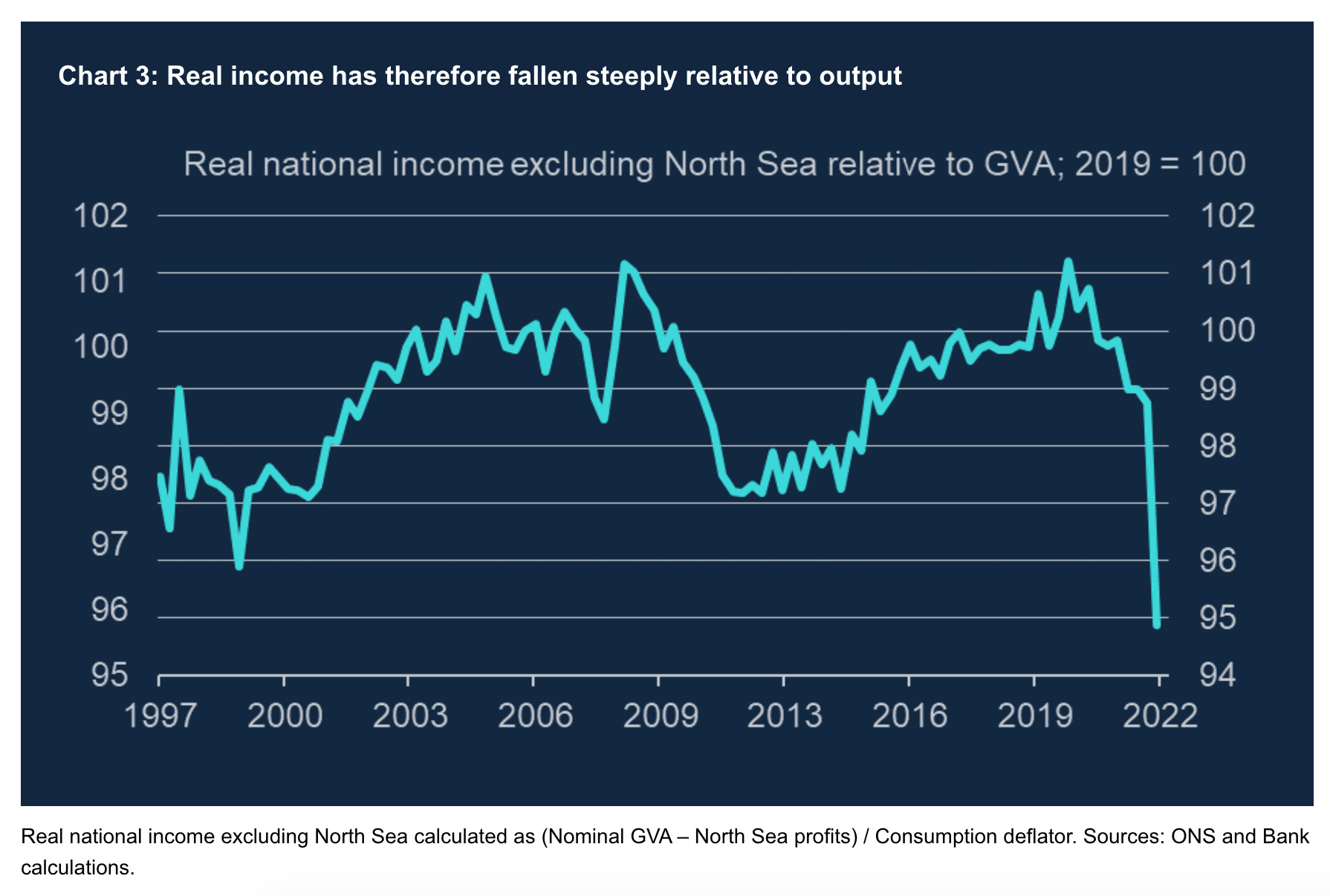

As a result of the surge in import prices, real income for the non-North Sea (oil) economy as a whole – how much the UK’s collective output is actually worth, in consumption terms – has fallen by over 5% since the end of 2019.

UK GDP will probably be only slightly below where it was in the last quarter of 2019, immediately before the pandemic. Yet real household income is likely to be over 3% lower, with real corporate profits down by more than 5% (around 10% if you exclude the North Sea).

For the time being, a better short-hand description is this: the pandemic and the war have led jointly to higher inflation and lower real incomes; the MPC will ensure the inflationary effects do not persist into the medium term; but the real-income hit exists either way, and will be reversed only to the extent the underlying shocks themselves go away.

The question is how far this hit to real incomes will trigger “second-round” efforts to compensate by raising wages and prices. The 1970s raised fears of a wage-price spiral but in Britain in 2022 this no longer seems relevant.

The second point I want to make is that we are inevitably having to learn, to some degree, about the scale of these “second-round” effects. The Monetary Policy Committee has raised interest rates faster than at any time in its history but obviously more gradually than inflation itself. In the main, this is because the direct effects of the jumps in traded goods and energy prices, as violent as they are, are likely to fade before policy could really do much about them. The exact timing and scale of the peak rate of retail energy price inflation will obviously depend (amongst others) on the nature and duration of government support. But in the absence of further (and equally steep) rises in wholesale gas prices, and even without any such support, inflation in retail energy bills is likely to be materially lower a couple of years from now than it is today. Inflation in the areas most affected by the pandemic seems already to have peaked. However, it’s also because we are relatively unfamiliar with the second-round effects of these things. They very clearly existed in the past, before inflation targeting was put in place in 1992. Economists long recognised that, in the presence of “real income resistance”, negative shocks – from, say, higher import prices or higher taxes – could generate inflation in wages and domestic prices. Estimates of these effects using the historical data, from before the 1990s, were reasonably sizeable. But they then began to decline, a phenomenon many attributed to greater flexibility in the labour market. So although there were occasions after 1992 when real incomes were squeezed – the big rise in import prices immediately after the financial crisis was one obvious case, so too perhaps the period of weak productivity growth that followed – there was very little sign of any second-round response of domestic inflation.

Energy prices are driving the EU trade balance into deficit

For subscribers only.

Italy v. UK: Net International Investment Position

For subscribers only.

Bond market dead …

For the fourth straight session, none of the latest issue of 10-year Japanese government bonds traded on Wednesday October 2012. According to Japan Bond Trading Co., it was the longest streak since March 1999, when comparable data became available. The responsibility for making a normally large market wither away into nothing belongs to the Bank of Japan, which on days such as these is offering a higher price for the 10-year bond than any private firm is willing to pay. That means trading between financial institutions, the kind tracked by market-data firms, dries up.

Source: WSJ

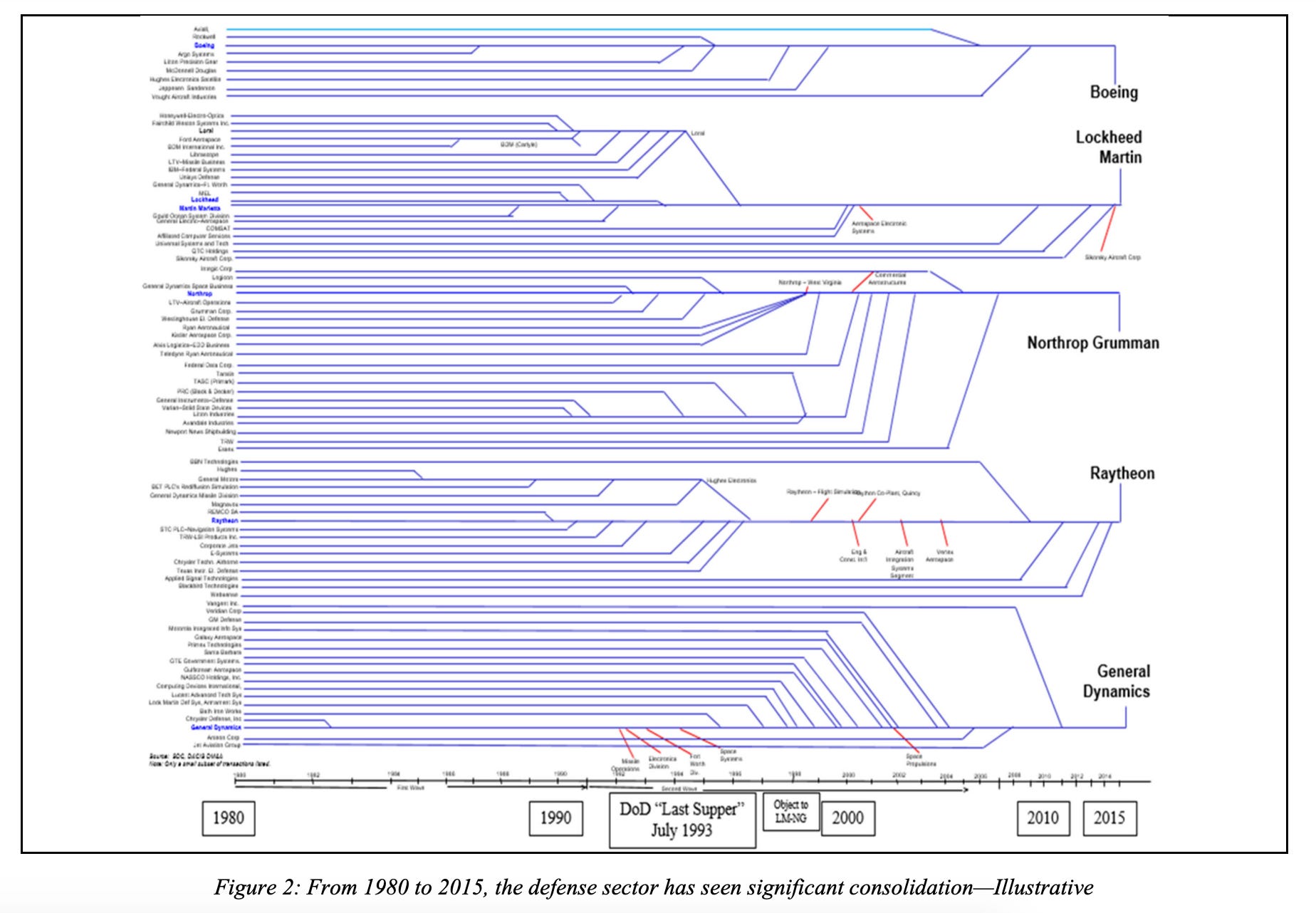

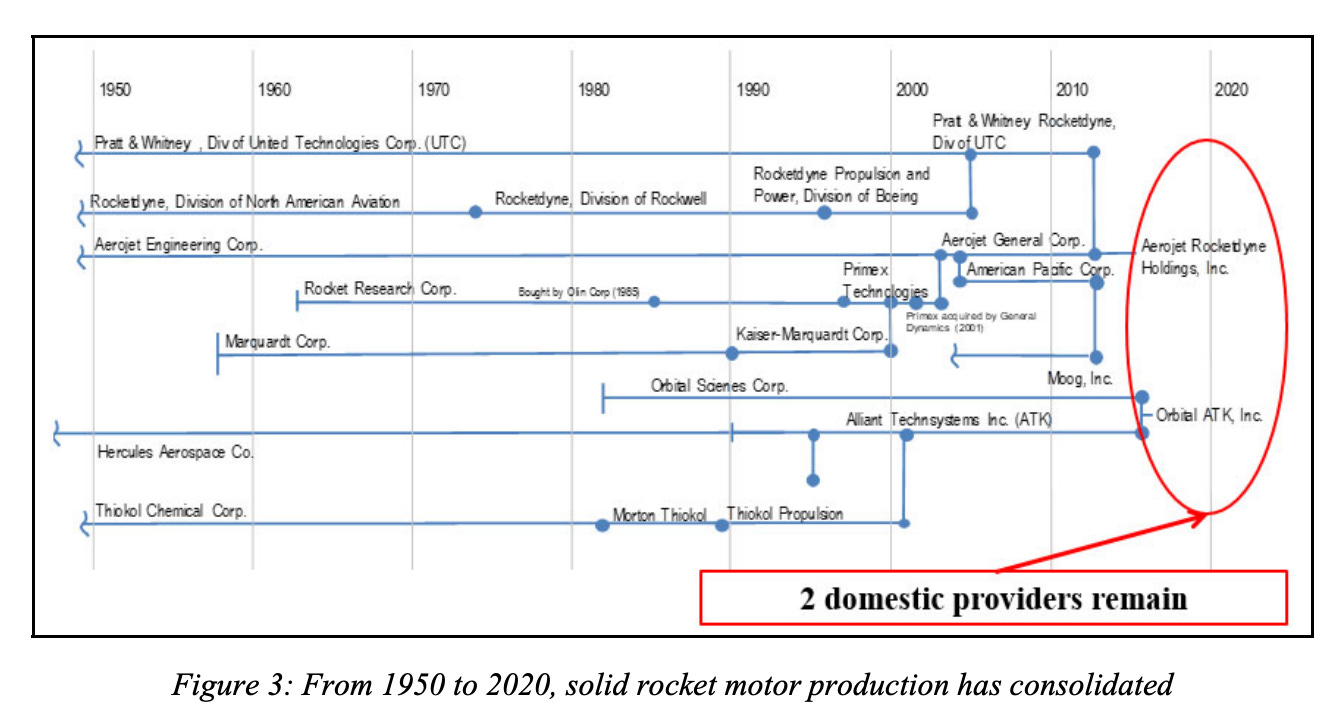

Merging the military-industrial complex

"[T]he total number of U.S.-based prime contractors declining from 51 in 1993 to 5 in 2000."

And then there were five. How the US military-industrial complex consolidated

Figure 3: From 1950 to 2020, solid rocket motor production has consolidated