Chartbook X Unhedged Debating Multipolarity

Good morning. Today is the second of three weekly collaborations with the FT’s Unhedged newsletter put out by robert.armstrong@ft.com and ethan.wu@ft.com which is essential daily reading.

If you want to read more from Unhedged -- usually for Premium FT subscribers only -- you can get a free 30 day trial by clicking here. The newsletter is also now available as a standalone subscription for just $8 per month.

In each of our installments, the Unhedged team kick off and then I reply.

Today the topic is the multipolarity thesis: the idea that the world has shifted from unipolar US leadership, or a bipolar world organised around “Chimerica,” into a world of multiple, shifting, partial, often temporary alliances. If multipolarity is indeed gaining momentum, the consequences will be large.

***

In a recent series of articles, the FT described multipolarity in terms of “the rise of the middle powers” or, more pithily, the “à la carte world.” A quote from Nader Mousavizadeh gives one neat summary of what that means:

The fact that the relationship between Washington and Beijing has become adversarial rather than competitive has opened up space for other actors to develop more effective bilateral relationships with each of the big powers but also to develop deeper strategic relationships with each other.

Unhedged has its doubts. It is true that the inclination of the US to project power around the globe seems to have diminished a bit under the last three presidents. But does the multipolarity thesis really add much to this basic observation?

Politics is not our area, however. What we can argue with some confidence is that in the realms of finance and markets, the world is as unipolar as ever and possibly more so. Here, the US remains indispensable, and we do not see this changing any time soon. This is not, we hasten to add, necessarily a good thing for the US or the world. But it remains a fact, and a fact of major economic and political significance.

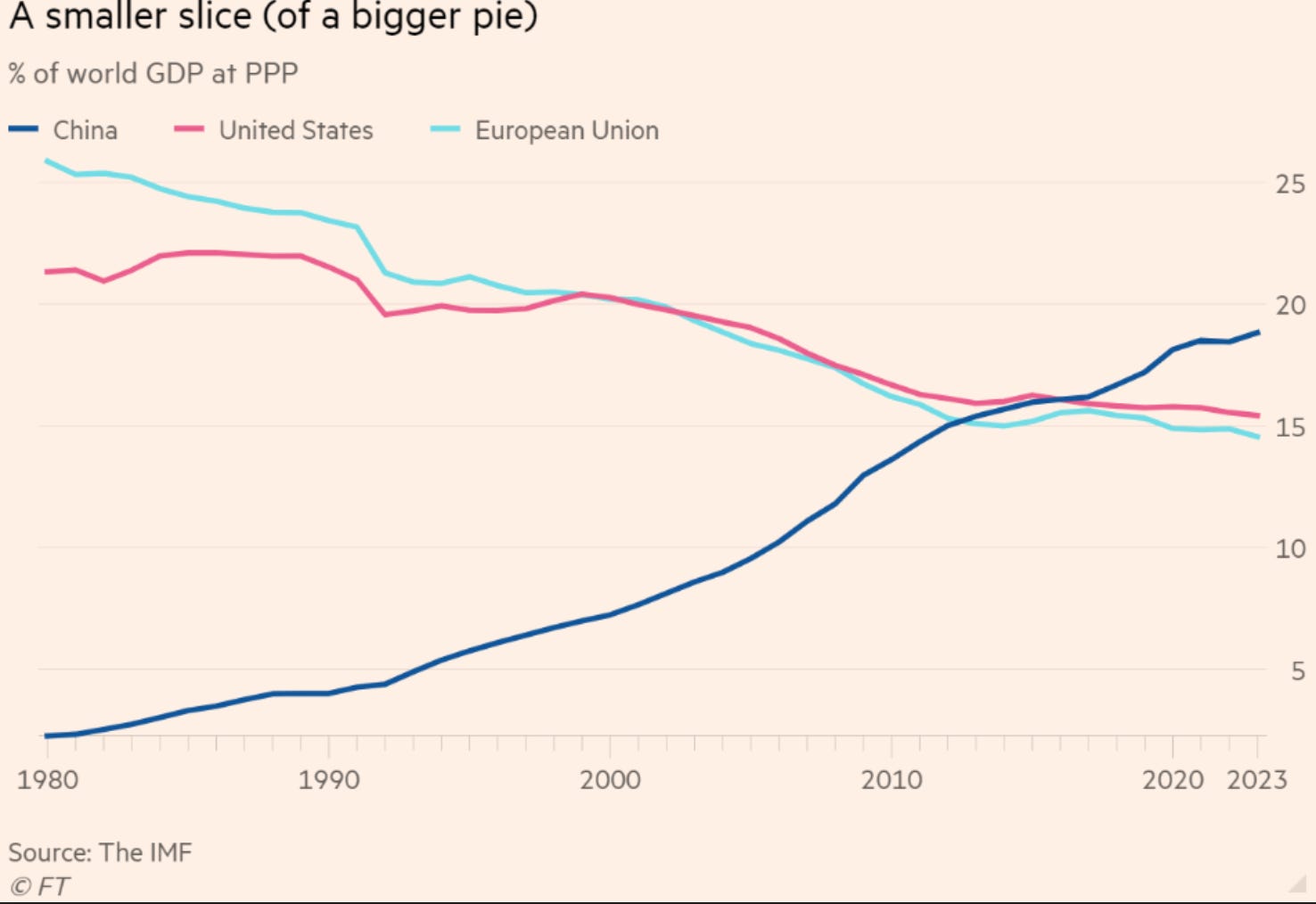

Part of the appeal of the multipolarity thesis stems from the fact that US share of global output has shrunk. This is inarguable, but neither new nor accelerating; in fact, it is an old trend that has stalled in recent years, when multipolarity has (in theory) taken hold. In the past decade the US and euro area share of world GDP has fallen less than a percentage point each:

In any case, too much is made of relative output shares. What is more important to global markets is the centrality of the US financial system and the dollar.

To understand the dollar’s power, consider the ideal features of a globally dominant currency. Karthik Sankaran, an FX markets veteran, says it must be “unfailing”: a Universal and Fungible Asset, Invoicing and Liability currency. That is, it must be widely accepted, fungible between financial assets and real-world goods and services, and useful for invoicing transactions and underwriting loans across borders.

Once a currency boasts these features, network effects make it sticky. So it is with the dollar and, to a lesser extent, the euro. Take invoicing, how cross-border trade gets settled. Even if a transaction is happening far away from the US, both sides have an incentive to agree on a standard “vehicle currency”, to minimise volatility and transaction costs. Once a global invoicing standard is set, it is annoying and expensive to change. This is why both the dollar and the euro have seen rising invoicing use, even as the US and euro area become less significant trading partners. In cross-border lending, too, the dollar’s real competitor is not the renminbi, but the euro:

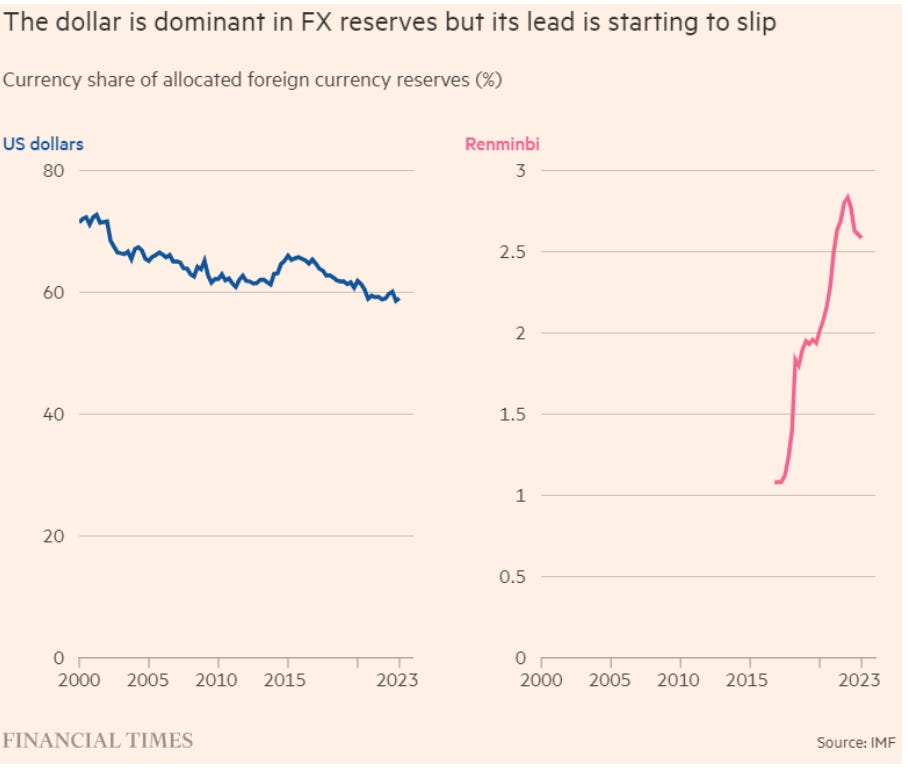

Some dedollarisation proponents point to the renminbi’s rising share of global central bank FX reserves. This chart ran in the FT in August:

This is an important change, perhaps accelerated by US sanctions policy, and some analysts believe the dollar share dip is deeper than the chart above indicates. But the move is not yet decisive, and it’s worth remembering that central bank reserves exist less as discretionary investments than as tools to defend a country’s home currency. The dollar makes up one leg of 88 per cent of all FX transactions, compared with 31 per cent for the euro and 7 per cent for the renminbi. As long as that remains broadly true, the dollar share of reserves can only fall so far.

Almost as important as the dollar are US Treasuries, the ultimate safe asset, indispensable as a haven, benchmark and collateral. The notion that American political or fiscal folly is about to unseat the Treasury is decades old, but has become popular again in the last year or two as US deficits have ballooned and Treasury yields have risen. But Treasuries will retain their crown; the pretenders to the throne are not up to the job. Europe has no Treasury equivalent because of its lack of a true federal structure. China’s closed capital account and opaque markets make its debt unappealing to global investors. Japan’s capital markets are too shallow to rival the US.

If you want to own a nation’s liabilities, you have to think about the political stability and growth profile of that country. What nation offers a better combination than the US?

The final bulwark of US financial dominance is deep, open, stable capital markets that are home to the greatest companies in the world. The premium that investors are willing to pay to own the equity of US corporations (and of international corporations listed on US exchanges) have only grown in recent years:

Correspondingly, over the past 10 years, US companies’ share of global market capitalisation has grown from 37 to 42 per cent, according to Finra. Yes, China’s IPO market has grown to rival or surpass the US’s in volume, and large regional companies like Saudi Aramco choose local markets to list. But when a truly global company comes to market, there is only one option. Witness the recent US listing of Arm, formerly a UK technological “champion”.

The openness and depth of US markets, and the legal stability they provide, and the sheer size of the US economy — along with the fact that countries such as China and Germany have built export-driven, surplus economies — make the US the centre of gravity for global capital. Money wants to come to America. The size of foreign claims on US assets is unlike anywhere else in the world:

As Michael Pettis convincingly argues, the flip side of this is massive US public and private debt, so America’s capital gravity is at best a mixed blessing for Americans. But nonetheless it makes clear the indispensable role of the US in the global financial system.

Adam, we are keen to hear if you think the multipolarity thesis is true outside (or inside!) the financial domain, and how the financial and political/economic pictures fits together.

Chartbook Replies

You make an excellent case for the continued dominance of the dollar in the global financial system. Like you I’m a sceptic when it comes to dedollarisation. The dollar’s centrality confers considerable power on the US. The impact of sanctions can be seen from Venezuela to Russia and Iran. Short of outright confrontation, the global dollar cycle shapes the fortunes of the entire world economy. China’s economy developed from the 1980s onwards, like that of Japan and postwar western Europe before it, within a world economy centred on the US.

But none of this means that multipolarity is a myth. Power is always relative. Even in the 1990s, the era we now think of as unipolar, it was China that decided to fix its exchange rate against the dollar at an extremely competitive rate, creating what some analysts dubbed Bretton Woods 2. That was a decision taken in Beijing not Washington, and China stuck to its guns despite considerable pressure from the US. A quarter of a century later, China’s exchange controls are as effective as ever, marking a major carve-out within the dollar system. And Russia has just tightened its capital controls to enable it to continue its war economy in the face of western sanctions.

Capital controls are certainly no panacea. As you note, they limit the attractiveness of China’s financial assets and can lead to painful macroeconomic imbalances. But they also give Beijing (and now Moscow) a degree of control over the balance of payments. They limit the dollar’s influence and that in turn radiates out to the large array of countries that trade intensively with China, whether that be Russia, Brazil or Saudi Arabia.

China was able to uphold its position not only because of its authoritarian regime, but also because in the 1990s and 2000s its strategy of cheap exports and trade surpluses sucked American interests in. US businesses, consumers and taxpayers learned to like a world of “twin deficits”. So deep was the symbiosis that Niall Ferguson and Moritz Schularick coined the phrase Chimerica.

The best way to think of today’s multipolarity is as the shattering of Chimerica. China’s ramified network of raw material supplies are no longer seen as efficient parts of global supply chains, but as a sinister geoeconomic network of influence. The boon of cheap imports morphs into the “China shock” that has forced America and its allies into a defensive crouch. Meanwhile, Brazil and South Africa tout the Brics bloc as an alternative to western power and African borrowers’ attempt to balance China against the west.

Much of this multipolarity talk is clearly exaggerated. I agree that we should be sceptical about rather artificial measures such as purchasing power parity-adjusted GDP. But the huge shift in the balance of the world economy is undeniable. Take the climate crisis. Emissions of CO₂ directly reflect industrial activity, energy use and land clearance. Today, developing and emerging market economies account for 63 per cent of CO₂ emissions. India’s total emissions exceed those of the EU. China’s emissions are twice those of the US. This is multipolarity written in the starkest terms. And it has huge implications for the future. If we actually achieve an energy transition it will by necessity be multipolar and its main drivers will be China and the emerging markets. Western investors and technology may play a supporting role. But for all the talk about “climate finance” very little money has materialised. Right now, Chinese investment and low-cost technology are dominating the energy transition, which has triggered a defensive reaction from Europe and the US.

Multipolarity brings into the open what the Chimerica vision buried, namely political and geopolitical differences. The South China Sea has become a militarised zone. And the old battlefields of the cold war have sprung back to life, from Ukraine to Yemen by way of the Caucasus, Syria, Israel and Palestine. On the face of it, this is another dimension of power in which the US actually has huge superiority. But as you note there is little appetite in Washington to actually use that power and that is hardly surprising after the disastrous experiences in Afghanistan and Iraq. Others are more willing to take risks. Regional players like the Saudis and Emiratis know they can count on US connivance and support. Others like Russia’s Vladimir Putin, or Turkey’s Recep Tayyip Erdoğan, simply feel strong enough to flaunt or even directly challenge the US.

Multipolarity reveals itself in trials of strength. It consists in being able to uphold an independent strategy with considerable impact at least in your immediate neighbourhood. That does not depend on global metrics. It certainly does not depend on achieving parity with the US, let alone overtaking it. It depends on having relative freedom of action in your immediate neighbourhood and being able to outlast your local antagonists and the bigger powers that may be interested. The dollar system does indeed remain powerful, but barring the imposition of a new geopolitical order, that is not by itself sufficient to contain the forces of uneven and combined development.

***

Unhedged make the mistake of equating spreadsheets with real resource activity. The true story of "multipolarity" won't take place on a spreadsheet -- it will take place in "meatspace" or "real resource land." Don't just follow the money; follow the molecules ...

"Multipolarity brings into the open what the Chimerica vision buried, namely political and geopolitical differences. The South China Sea has become a militarised zone. And the old battlefields of the cold war have sprung back to life, from Ukraine to Yemen by way of the Caucasus, Syria, Israel and Palestine. On the face of it, this is another dimension of power in which the US actually has huge superiority."

The issue with Chimerica was/is that the Chinese refused to allow their assets to be purchased with funny money generated from thin air by the Wall Street. As was/is with the Russians, who, after 2000 took back control of their resources and economy. The Americans tought they were on the top of the world and had the rug pulled from under their feet, and now it is they that are lashing out.

Malaysia and Indonesia have agreed to not use dollars in trade between them and with other countries in ASEAN. What it matters in real world is how the real economy works, what the "global investors" do with their surpluses is less important, since ultimately, states can impose capital controls, and generate themselves investment. Especially when China is now a good source of technology for the vast majority of the world. Have you seen the high speed double decker train built by the Chinese?

John Kirby just spoke the devastating quiet part aloud in yesterday’s press conference, admitting that they’re at the “end of the rope” in respect of supporting Ukraine. As Obama said, Russia has escalating dominance in Ukraine. China has escalating dominance in her part of the world.

Plutocrats/oligarchs everywhere hold on to the dollar empire, and hate with their guts any "authoritarian" regime that keeps them under a modicum of control, and this is why they love the US which is a plutocracy, and for the most part of its history was a plutocracy:

"The contemporary US is a plutocracy – the term is not intended polemically, but as a statement substantiated by the facts and accepted by most informed commentators. It simply describes a country in which networks of corporate interests set the policy agenda via lobbying and political donation, and where hard data show that, over decades, in literally every translation of advocacy into legislative acts, the interests of the wealthy prevail. Plutocracy in fact is the form that rule typically takes in the US; most states, says Turchin, have a form of rule to which they revert over centuries after crisis periods, and ‘culture is persistent’ here. The US is reverting to type after the crisis of the Great Depression spurred elites, in their own self-interest, to turn off the wealth pump; this new co-operative instinct was consolidated by the experience of World War II, so that the decades from the early 1930s saw ‘the Great Compression’, with the gap between the wealthiest in society and ordinary citizens narrowing. Reversal of this trend is a reversion to type."

https://drb.ie/articles/there-will-be-blood-2/