Chartbook Newsletter #7

Revisiting The Role of Hedge Funds In The March 2020 Treasury Market Turmoil

Last week’s newsletter #5 on the turmoil in the all-important US Treasury market in March 2020 generated some interesting reactions, specifically with regard to the role of hedge funds. Was selling by hedge funds more important than I had suggested?

I based newsletter #5 on two sources from the Fed: a speech by Lorie Logan of the New York Fed and the Financial Stability Report. They have in common that they deemphasized selling pressure coming from hedge funds, emphasizing, instead, the role of foreign reserve managers and mutual funds.

As the Fed remarked:

“In sum, the reduction in hedge fund Treasury positions may have contributed notably to Treasury market volatility in mid-March amid a massive repositioning by a wide range of investors. However, so far, the evidence that large-scale deleveraging of hedge fund Treasury positions was the primary driver of the turmoil remains weak.”

Empirically, this assessment is heavily shaped by a paper by Vissing-Jorgensen. This suggested that selling by hedge funds was the smallest of the three groups of sellers.

But, is this persuasive?

A source at one of the major banks close to the action in March 2020 remarked that the quantitative balance was less important than the nature of the selling. Hedge fund selling was more destabilizing, this source argued, because it was more opaque, more urgent and more “scary”. From the point of view of the broker-dealers, it was not clear how much the hedge funds would need to sell and how desperate the selling might become.

Another question was raised by a source at the Office of Financial Research (Treasury). Was the scale of hedge fund selling larger than the Fed and its sources were allowing?

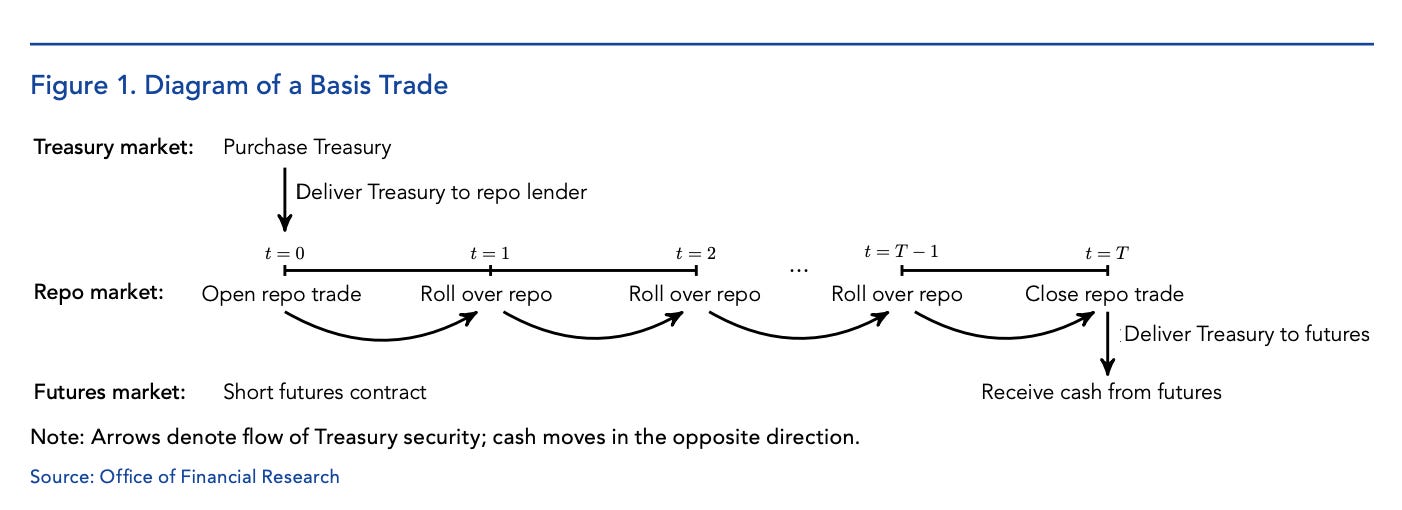

In July, the OFR published an important study of hedge fund Basis Trades and Treasury market illiquidity by Daniel Barth and Jay Kahn. This is recommended reading on every aspect of this branch of hedge fund business.

Barth and Kahn emphasize the huge surge in hedge fund transactions in Treasuries that began in 2018.

In their view, this was driven by the huge surge in Treasury issuance as a result of the deficits of the Trump administration and declining foreign interest in US Treasuries. This points to the macrofinancial forces that were at work in setting up the instability in Treasury markets both in 2019 and 2020. It is a point to which we will return.

In addition, the basis trade business migrated from banks to the hedge funds. As Barth and Kahn put it:

“Hedge funds and other proprietary traders are not explicitly limited to maximum leverage ratios in the same way banks are. Standards imposed after the 2007-09 financial crisis put direct leverage limits on banking institutions, typically requiring a capital-to-asset ratio of at least 5 percent, which implies a maximum leverage ratio of 20 to 1.7 Hedge fund leverage is constrained only by the haircuts on the collateral, and for Treasury securities haircuts are typically around 2 percent. This implies a maximum leverage ratio for hedge funds of 50 to 1. Because the basis trade profits from tiny differences in spreads, high leverage is necessary to make the trade worthwhile. Basis trade activity may therefore have migrated from banks to hedge funds and other less-regulated traders because leverage limits made the basis trade unprofitable for banks. Anecdotal evidence supports this; the Financial Times has reported that many of the lead traders executing these trades at banks have left to join hedge funds.”

This set up an overhang of leveraged hedge fund exposure to Treasuries that was anchored on futures contracts and repo funding.

When the panic hit in March 2020, a surge in volatility in Treasury markets triggered clauses in derivative contracts which required hedge funds to post more collateral. At the same time funding costs in repo markets stiffened. It was this double squeeze that triggered the hedge fund selling.

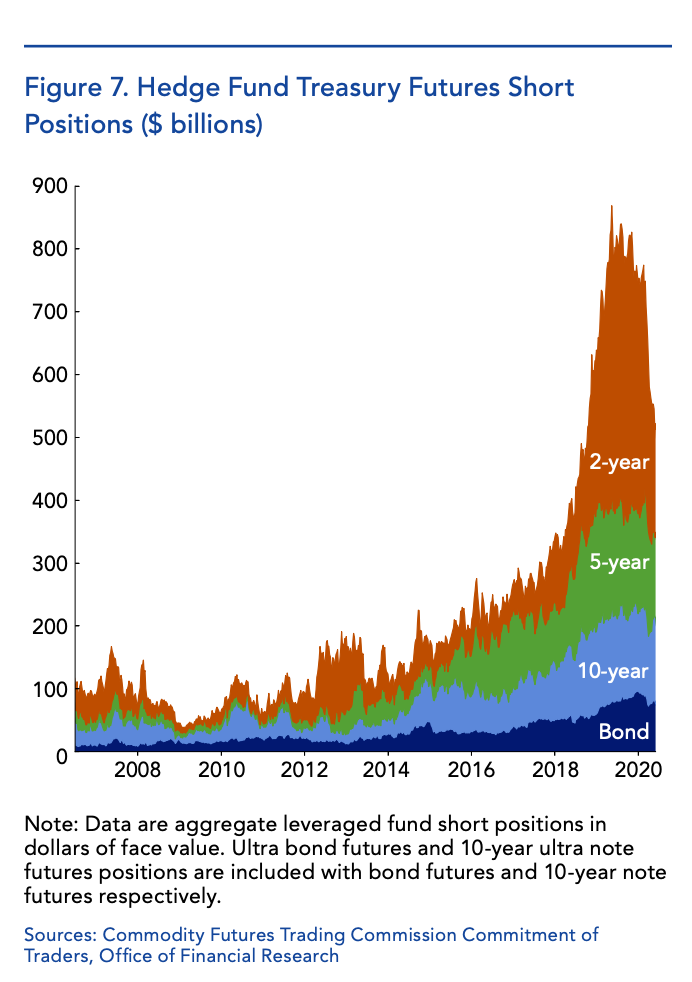

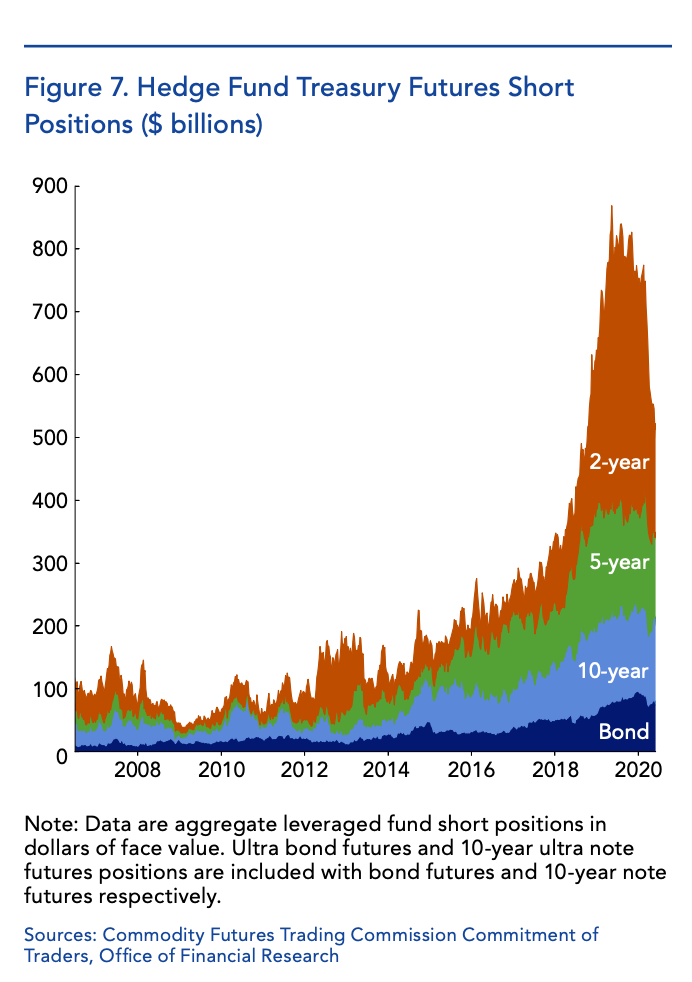

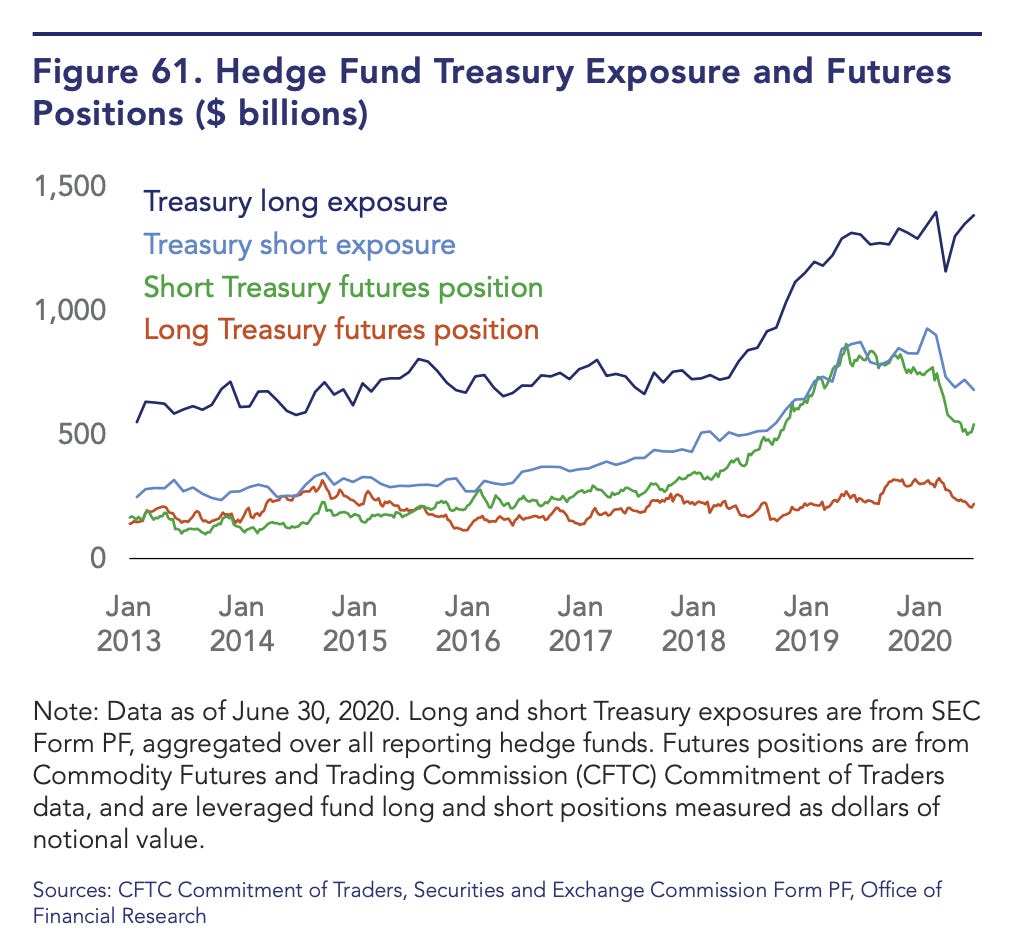

Altogether, the OFR’s Annual Report estimates that long Treasury exposure for hedge funds fell by $242 billion (17 percent) during March.

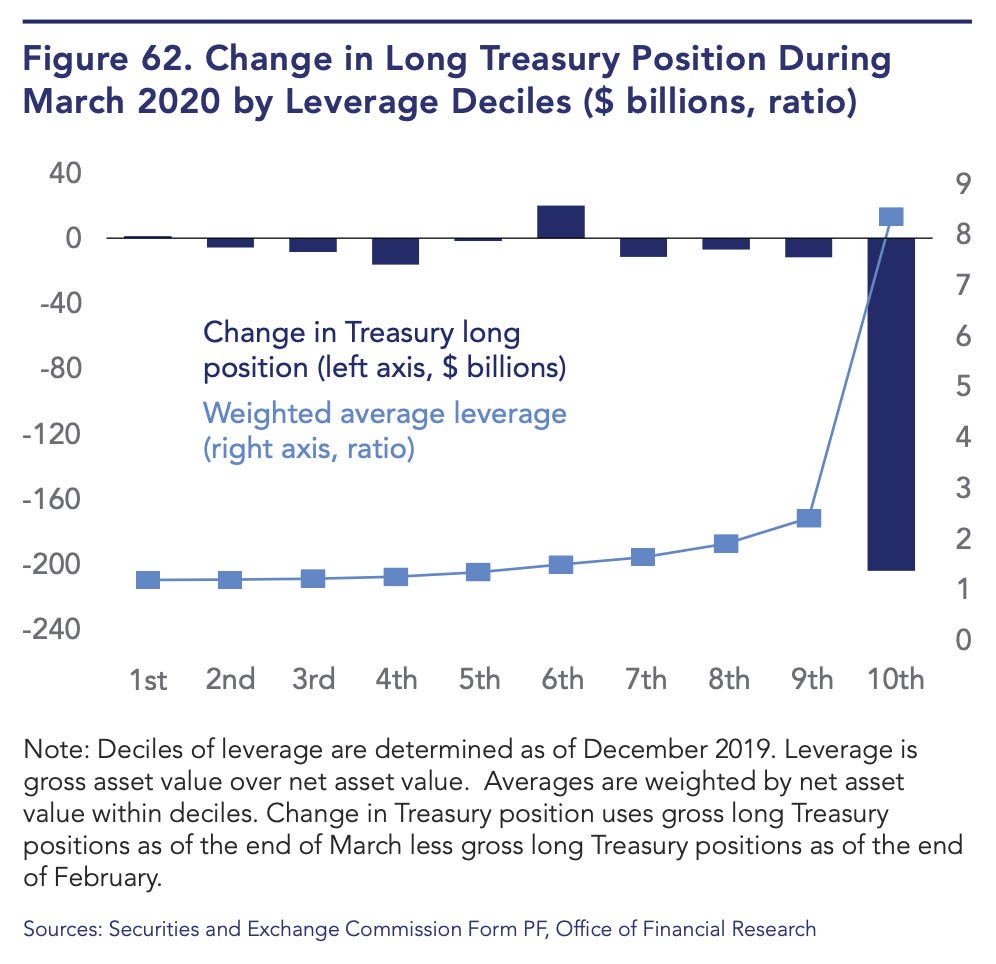

The selling was heaviest amongst those hedge funds that were carrying the greatest degree of leverage.

$ 242 billion is a lot more than Vissing-Jorgensen’s data suggest.

Importantly, the OFR emphasizes that it was not only cash-future basis trades that were unwinding, but a variety of different hedge fund strategies all driving Treasury sales.

Lorie Logan of the New York Fed remarked that she regarded hedge fund sales as “an important contributing factor, but not the sole source of the challenges” in the Treasury market.

Reviewing the OFR data would suggest that the hedge funds were a very important “contributing factor” indeed.