Chartbook newsletter #4 by Adam Tooze

Financial Stability Three Ways

How stable is the financial system?

At least twice a year, the world’s central banks and international financial institutions like the IMF and the Financial Stability Board set themselves to answering this question. A typical rhythm is to publish two reports a year, one in the spring and one in the autumn. National central banks cover their respective territories. The IMF and the Financial Stability Report take a global view. In the last few weeks, we have had the reports from the IMF, the Fed and the ECB. The Bank of England does a very interesting report. So too does the Bank of Japan.

These are rich documents, stuffed with data, charts and commentary, a treasure trove for us to plunder for months on end. For today’s newsletter I thought it would be interesting to compare the reports issued by the Fed, the ECB and the IMF as documenting different points of view at this dramatic moment in the development of the world economy.

The Fed’s report breathes the air of 2008 and Dodd-Frank. It is an elegant, stripped down document that focuses on the essentials of financial stability i.e. credit risks arising from loans made to businesses and households and funding risks arising from the sources of funding used by banks, investment funds and insurers. The commentary is sparse. The Fed presumably does not want to give too much away. Nor does it want to find itself in hot political water. There are a limited number of box-inserts, which address themes of particular interest. The November 2020 issue has a fascinating box on the dramatic events in the US Treasury market this March, to which we will return in a forthcoming newsletter.

The European Central Bank’s report is strikingly different in tone. It takes a much more comprehensive approach to evaluating the macroeconomic position of the Euro Area. It is frankly political, issuing warnings on fiscal policy and corona support measures. It is more adventurous in analytical terms than the Fed and more wide-ranging in its coverage, reflecting the way in which the remit of the ECB has exploded in recent years.

The IMF’s Financial Stability Report is a true wonk fest, written by economics PhDs for an audience that may include a high percentage of the same. It includes wide-ranging chapters on a variety of thematic issues, reflecting the Fund’s research. This issue highlights the instruments used by Emerging Markets to navigate the recent financial turmoil and a chapter on issues of financial risk and climate change, an issue which America’s Federal Reserve is only just daring to touch.

What do the reports tell us about financial stability?

The Fed’s report is the most guarded but also the most sanguine. Since the tremors in March the US financial system has shown resilience. America’s banks are so well capitalized in the Fed’s view that they can withstand even a worst-case scenario. The points of risk in America’s financial system that the report points to are:

Commercial real estate remains a source of worry for the Fed. Lending standards that tightened with a bang in the spring have not eased much since.

The small business sector, about which the Fed is alarmed, but about which it does not present data.

The insurance system, where it fears a build-up of maturity mismatch between short-term liabilities and increasingly illiquid assets. This, presumably, is driven by the desperate search on the part of fund managers to find yield in a world of ultra-low interest rates.

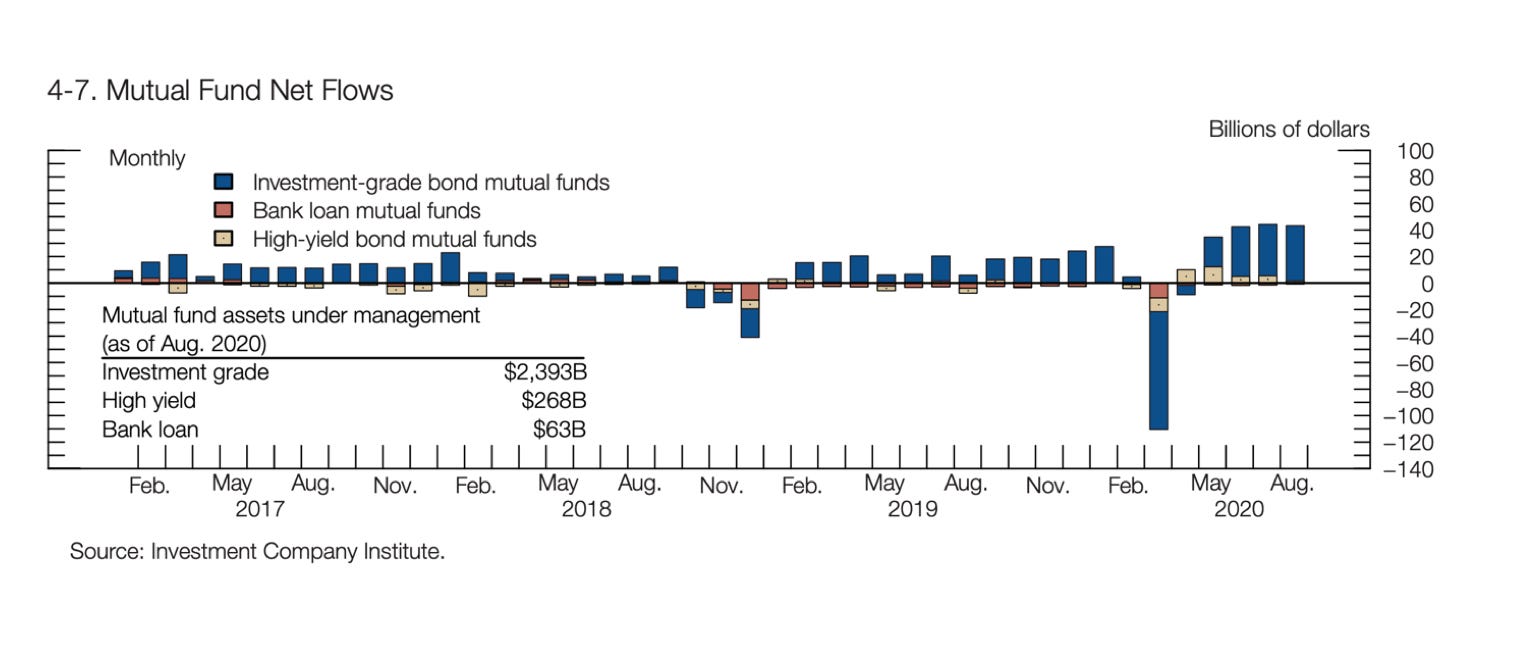

Finally, the key point that arises from the March troubles is the need to look at the regulation of open-ended bond funds. These vehicles offer affluent Americans a means to invest in relatively illiquid assets like corporate debt, including high yield junk bonds, whilst at the same time guaranteeing the right to daily redemption. Their holdings of corporate debt have grown rapidly since 2008 when yields on US Treasuries plunged.

When redemptions amount to only a trickle, this can be managed by holding reserves of more liquid assets like US Treasuries. But, when the going gets rough, as in March, they become drivers of fire sales adding to instability in bond markets.

Fundamentally, any entity that takes short-term funding and puts it into illiquid assets that have to be held over the long-run, is engaged in maturity transformation. It is, thus, exposed to run risk. After the March events there are likely to be calls for more reporting and tighter regulation.

Teams of Fed experts are at work on devising tools with which to monitor surges in stress in these funds.

Source: Fed

The Fed is tight-lipped when it comes to making any broader statements about the likely future development of risks and stresses in the financial system.

To move from the Fed report to the ECB’s Financial Stability Review is to enter a different world. The ECB’s entire report is framed by deep concerns about the growth prospects for the Euro area, the likely course of fiscal stimulus and its impact on households and businesses. That in turn will affect their ability to service the debts they owe to the banking system, about which the ECB expresses considerable concern.

The European banks have been ailing since 2008. So, the difference between the Fed and the ECB’s reports is not merely a matter of analytical approach or tone. A gulf separates the likes of JP Morgan from Deutsche Bank. But there are also in Europe huge political issues at stake. Despite the creation of the Next Generation EU fund, the ECB has no fiscal counterpart. It must hope that national governments find ways of continuing the support that they currently deliver. There is every reason to fear that they will not. Indeed, the ECB has handily compiled their budgetary plans for 2021 and they suggest a serious contraction, which will further weaken the recovery.

As the ECB states in bolded text: “An abrupt end to government policy support schemes would pose cliff-edge risks to the debt servicing capacity of euro area firms and households. The materialisation of such risks could have a knock-on effect on economic activity and an adverse impact on banks’ balance sheets and capitalisation.”

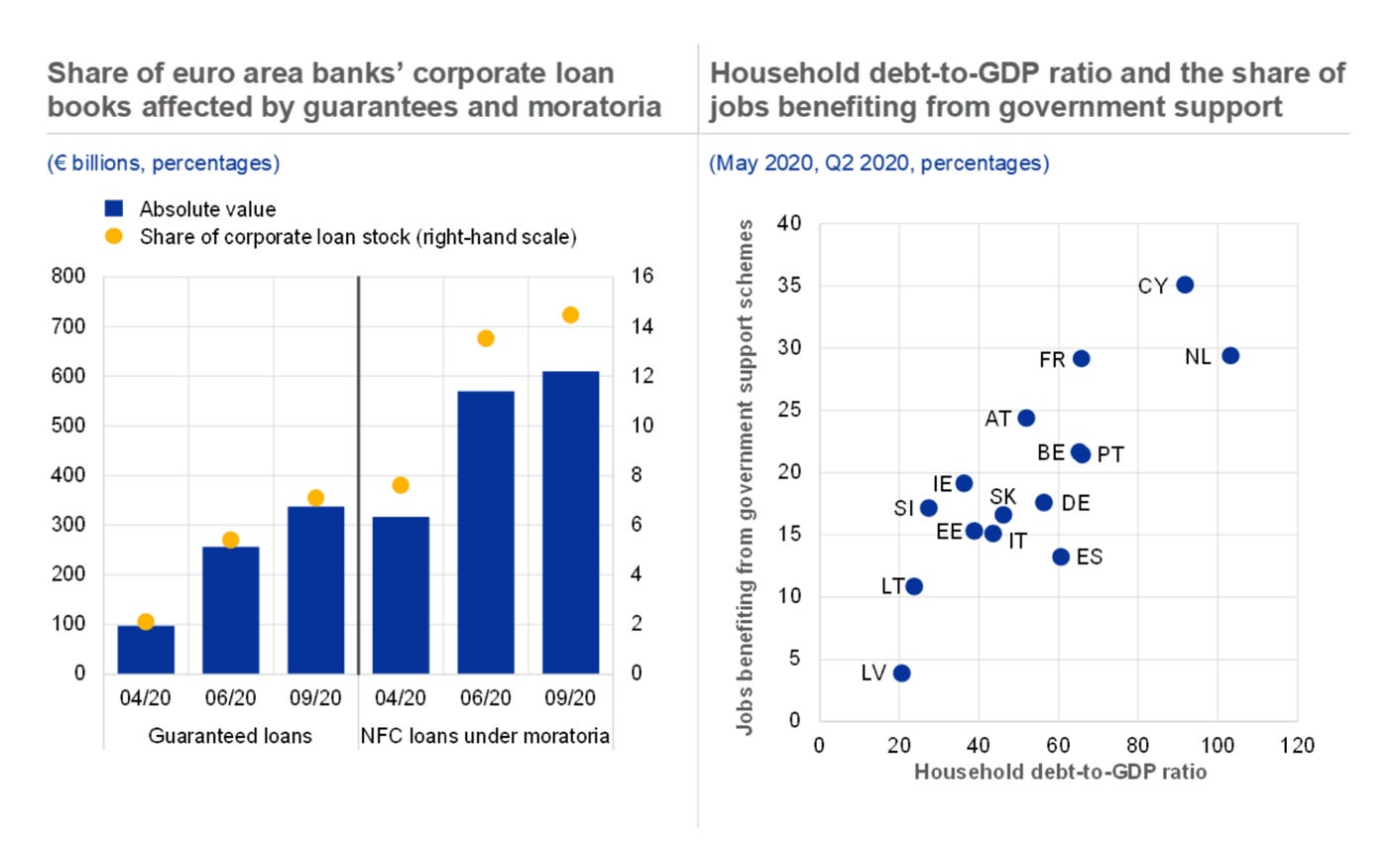

Cliff-edge risks are very bad news for financial systems because they produce discontinuities, tipping point effects, which are difficult to insure against and can induce run risk. To illustrate its point the ECB includes a handy graph which shows side by side the extent to which business loans, jobs and household credit in the Euro area are currently dependent on special corona measures. This is a highly political use of graphics if ever there was one!

For those interested, I will elaborate on this scenario in a column for Social Europe out next week.

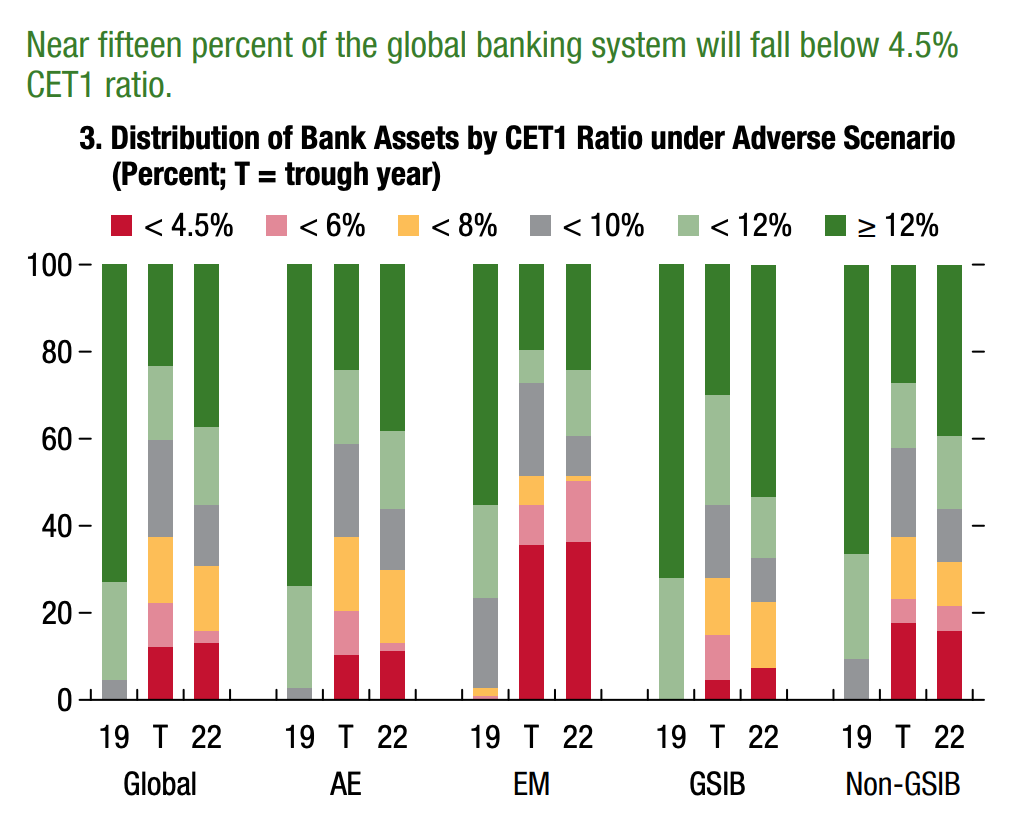

The IMF’s Global Financial Stability Report report is similar to that of the ECB in spelling out explicitly the way in which its outlook on the macroeconomy is connected to its assessment of financial balance sheets. But the IMF does this for the entire world economy. In fact, its economists are touting a brand new model that allows them to project the likely impact on the capital-ratios of “350 banks from 29 jurisdictions, accounting for 73 percent of global banking assets” (see the Online Annex).

This is a dizzying exercise in what is called macro-financial modeling. Whereas there was once a deep trench that divided macroeconomic modeling from financial analysis, the IMF can now use its models to move from its forecast for national economies to make specific forecasts for particular business balance sheets. The results are anonymized, but the IMF has in fact modeled what it thinks the development of the balance sheet of JP Morgan, HSBC, Deutsche Bank and Barclays will be, depending on the forecasts of global economic development made by the Fund’s own macroeconomics team. Most of the national central banks do this for “their” banks. The IMF does it on the basis of publicly available information for the global financial system.

The calculations are, of course, no more than provisional estimates, highly educated guesses, but nonetheless interesting for that. The Fund’s results are a dramatic warning against complacency.

The analysis shows that capital ratios would decline as a result of the COVID-19 crisis, but remain, on average, comfortably above regulatory minimums. However, there are differences across and within regions. A weak tail of banks, accounting for almost 15 percent of assets in the baseline adverse scenario, might fail to meet minimum regulatory capital requirements in an adverse scenario.

That is an awful lot of bad apples. And in the EM in an adverse scenario, the numbers are very large indeed. More than a third of bank assets in the EM could be sliding towards the danger zone 2022. That would unleash a disastrous doom-loop.

For this reason, amongst others, at least some voices in the IMF are calling for governments to maintain spending, though as I noted in newsletter #3, when looked at in detail IMF country programs are in fact demanding austerity from 2021. One way of reconciling that contradiction is that very few of the world’s biggest 350 banks are located in country’s in receipt of IMF emergency assistance.

For those at the epicenter of the financial system the IMF recommends a suite of support measures targeted at the banks including “government loan guarantees and other bank-specific policies help relieve the decline of reported capital ratios and reduce bank capital shortfalls”.

This no more than a first taste of these fascinating documents. Much more to come!

In the mean time …

New on adamtooze.com this week:

A piece in the Guardian locating the Biden Presidency’s political predicament in historical context.

A discussion with David Runciman and Helen Thompson, old friends from Cambridge, on one of my favorite podcasts Talking Politics