Chartbook 449: Voldemort on Threadneedle street. The Bank of England and the "haunted house" of English politics.

Imagine the scene:

In some Harry Potter version of 21st-century London, a group of deathless UK Treasury officials gathered from across the last century huddle over warm pints and glasses of Chardonnay. Around the table there are officials from the 1920s, the 1930s, the 1970s, 2022 and today.

Inevitably, in May 2026, the subject of conversation is the disintegration of the current Labour government. Despite its huge majority in parliament, it has been reduced to tatters by catastrophic local election result. These exposed the fact that rather than having a government with a clear popular majority, the UK is like most other modern societies divided into 5 segments each of which commands between 26 and 16 percent of the vote.

Perhaps unsurprisingly, the leadership at Nos 10 and 11 Downing Street - where the Prime Minister and the Chancellor (Treasury Secretary) work - seem paralyzed. They are caught between mounting discontent over unfairness and the cost of living, and tough fiscal strictures that push them into making unpopular spending decisions.

In the London pub, the Treasury officials from across the ages, can barely hide their satisfaction at the latest display of democratic politics caught in the vice-grip of financial logic.

“Remember the mur d’argent and the banker’s ramp?”

“Just like yesterday!”

There are smirks around the table.

Then the representative of 2026 pipes up:

“One thing you have to say about the current lot (referring to the latest hapless Labour government), you don’t have to teach them about the bond market!”

There is a murmur of ascent from the Treasury Mandarins.

The trauma of the fiscal crisis of September-October 2022 sits deep.

Back then, in the final stages of Tory decay, a ‘mini budget’ that challenged fiscal orthodoxy led to a brief but fierce panic in one of the oldest government bond markets in the world (aka gilt market). Now all you have to do is to mention the “bond market” to hush debate.

“And the funny thing is”, the young man in the huddle continues, “they don’t even want to talk about … ”.

There is a sudden hush. Significant looks are exchanged around the table.

About?

One of the senior figures puts down his glass with a decisive “clink”.

He-Who-Must-Not-Be-Named has entered their thoughts.

Meanwhile, a few miles away in a grubby pub in Bloomsbury, two conspirators from the camp of Critical Macrofinance huddle over cans of low-alcohol IPA.

They look at each other and blurt out loud:

“The Bank!”

“Everyone in the bloody Labour party is talking about the bond market. But why aren’t they even mentioning … the Bank of England!?”

“Why is no one talking about Voldemort?”

In Paul Mason’s blogpost, after much chest-thumping about basic fiscal logic, the basic point about the Bank of England is buried in the fine print at #3 in his list of suggestions as to what a radical Labour government might actually be able to do!

Back in Bloomsbury they shake their heads and ask: “Didn’t we learn anything from the Eurozone crisis?”

Meanwhile, as if summoned to the conversation by some higher force, the “pink pages” announce:

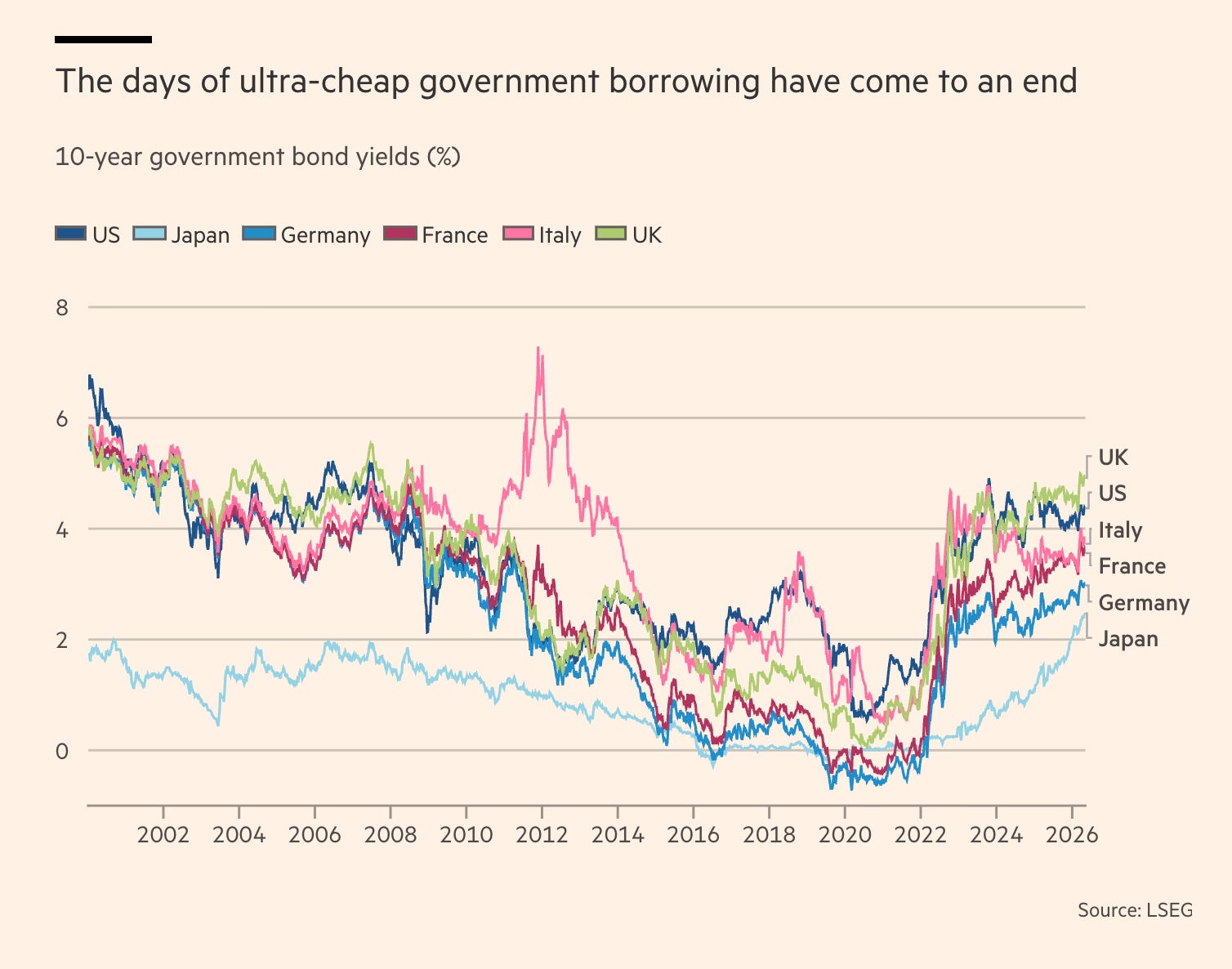

“The days of ultra-cheap government borrowing have come to an end” and Martin “Whizzard” Wolf publishes the graph of the season

Look at the UK in 2026, perilously positioned on the upper edge of the pack. No wonder no one in London needs any lessons about the “bond market”.

But, look again. Imagine how they feel in Rome.

What is London’s nightmare in 2026? The nightmare is that you end up like Italy in the early 2010s during the Eurozone crisis. Once comfortably situated in the middle of the pack, watching with horror as your ten-year yields explode to 7 percent and “spreads” become a national nightmare. One of the largest economies in Europe, a founding member of the euro, stigmatized.

But the message of the Italian experience is ambiguous.

After all, the stigma didn’t last. In 2026, Italy borrows at rates lower not only than the UK but the US. The US, which, as everyone knows, enjoys the “exorbitant privilege” of being the issuer of reserve, safe asets.

What kind of magic is this? How did Italy, in the space of fifteen years, go from being good, to bad and back again?

Which brings us back to our dissident friends in their Bloombury boozer and their memories of the Eurozone crisis.

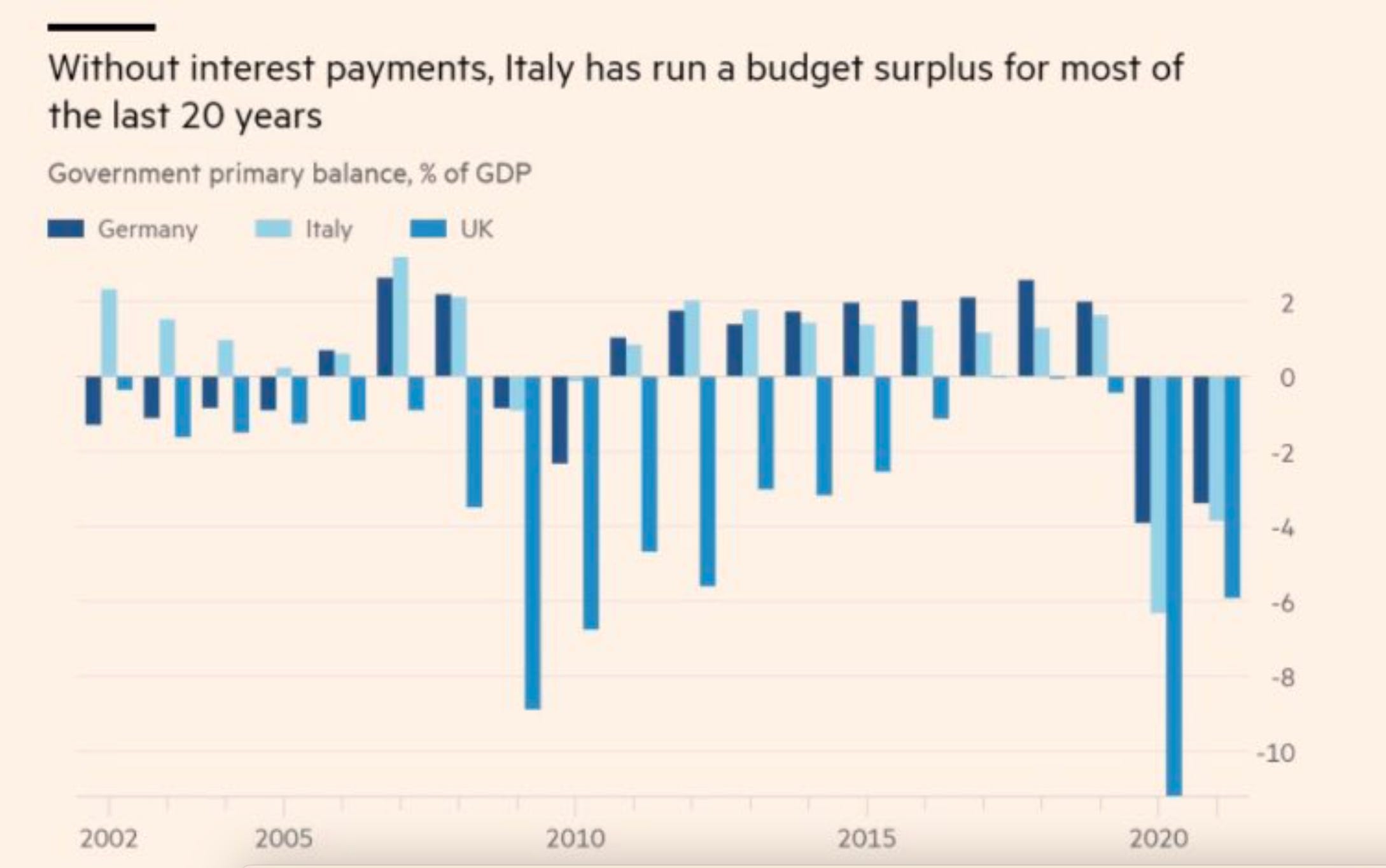

Italy never was Britain - with its ongoing fiscal deficits.

Without interest payments, on primary balance, from 2000 to 2020 Italy ran a tight fiscal ship. Even in 2008 it barely went into deficit and when it was being put on the rack in the early 20210s its primary surplus matched that of austere Germany.

So, what happened? How did it end up stigmatized?

Of course Italian politics didn’t help. Berlusconi was at the helm and he had legal issues.

But amongst friends in the Bloomsbury pub, Berlusconi is a sideshow, the name we whisper to each other is “Trichet”.

From 2004 to 2011 the ECB was headed by Jean-Claude Trichet, ex of the French Treasury, more German than the Germans. After 2009 as the news of the Greek fiscal disaster broke, the European bond markets wento into panic mode and Trichet began a brutal game of cat and mouse. Between 2009 and 2011, Trichet intervened in the bond market to help, only when he thought he had compliance with austerity. When he thought they were uncooperative, he withdrew. In the summer of 2011, he even made direct suggestions to his Italian counterparts in Rome, as to how Italy should be governed.

It was this cat and mouse game that drove the bond markets crazy and exposed Italy to a violent squeeze.

When Mario Draghi took over the ECB at the end of 2011 and declared “whatever it takes”, the pressure on Italy, gradually eased. It is that starring role that has made Draghi into the towering figure in European politics that he remains today.

So now you see why voices in London hush when it comes to the Bank of England.

“The bond market” isn’t an irresistible objective force like the weather or an avalanche.

It can appear like that. But that depends on the way it is being handled, or not handled by the central bank.

Which is why the silence about the Bank of England in London right now is so significant.

If you think this all sounds a bit fishy, coming from a left-liberal Keynesian like myself, well, let me introduce you to Robin Brooks, who, to put it mildly, plays on a different quidditch team to me. Here, from the position of a fiscal hawk is Robin’s celebratory account of the Bank of England’s role since 2022;

In October 2022, at the height of the bond market blow-up in the UK, something incredible happened. Governor Andrew Bailey told British pension funds the Bank of England would end its support program for the country’s fragile gilt market, drawing a line under how much help the central bank was willing to give to exposed pension funds and - implicitly - the government. By the end of that week, Kwasi Kwarteng - the finance minister - had resigned. Prime Minister Liz Truss would soon follow. This episode is so incredible because it contrasts with what happened in the Euro zone earlier that year. Bond markets in Spain and Italy were under pressure amid high inflation and rising interest rates. In the middle of this, Mario Draghi - Italy’s Prime Minister - resigned, compounding pressure on bond markets of high-debt countries on the Euro periphery. Unlike the Bank of England, the ECB caved. It bought Italian and Spanish government bonds in an effort to cap yields and introduced a new tool that signaled to markets it might do such caps more frequently going forward. Faced with pressure on bond markets, the ECB capitulated to political pressure from high-debt countries like Italy and Spain. The Bank of England stood its ground and toppled the Truss government. This kind of thing has long-lasting consequences. It means markets price a higher probability of yield caps in the Euro zone, which keeps Italian and Spanish yields artificially low, while markets feel free to push up UK yields without fear of central bank intervention. As I flagged in yesterday’s post, this means you really can’t compare UK yields to those of other high-debt countries. The UK looks worse, but only because its central bank isn’t interfering with markets.

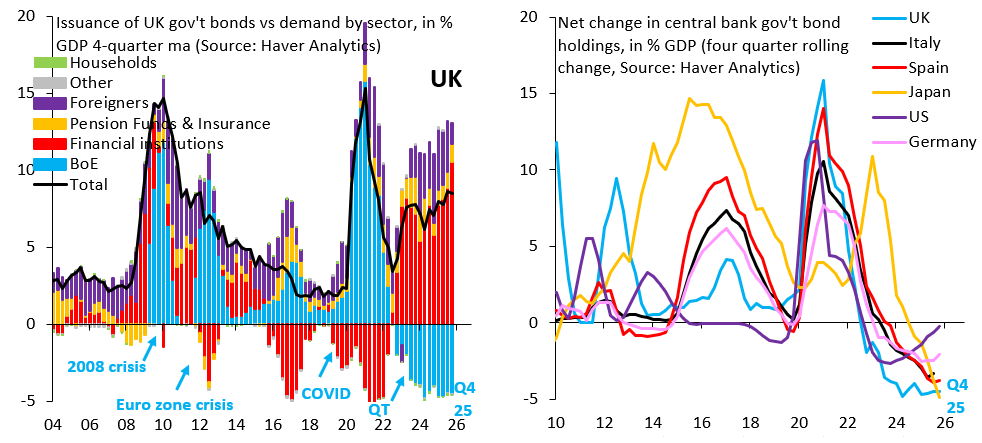

There’s more to this than just that 2022 episode. The Bank of England has also been much more aggressive in its quantitative tightening (QT) than other central banks. If one motivation for quantitative easing (QE) is to lower bond yields - especially longer-dated ones - then it stands to reason QT pushes yields up. The left chart above shows a four-quarter moving average of UK government debt issuance (black line) in percent of GDP and which sectors absorb this issuance, including the Bank of England (blue bars). The right chart above compares the Bank of England’s accumulation or run-off of government bonds (blue line) with that of other central banks, where this blue line is the same as the blue bars in the left chart. The Bank of England was quicker and more aggressive than other central banks in downsizing its bond holdings, so UK yields will have risen more than elsewhere also for this reason, not just because of Governor Andrew Bailey’s remarks in October 2022.

Back in October 2025, after a conversation in New York with friends in British politics, my sense of dysphoria was such that I raised the issue of the Bank of England openly in the FT

Since 2008, the UK has slid into a deep economic and political predicament. Growth has stagnated to a degree far worse even than in the 1970s. The Tory leadership’s wager on the Brexit referendum spectacularly backfired, leaving the UK isolated from Europe and at the mercy of its special relationship with the US, many of whose political class regard the UK as a basket case. After years of austerity, the Labour party lurched to the left and then back to the centre. The Tory party has been eclipsed by the populist nationalism of Reform. Any British government should be worrying first and foremost about how to restart growth. Instead, Keir Starmer is beset by shades of the gilt market panic triggered by the Liz Truss government in 2022. The debt level is higher than in recent years, but there is no cause for panic. UK debt is at far from critical levels and of long duration. Whether you want to “take back control” or launch progressive economic policy, a democracy dogged by fear of bond market vigilantes is unhealthy. In a country that is a monetary sovereign, this climate points to one thing: a disconnect between the government and the central bank. Since 1997, the independence of the Bank of England has become a sacred cow. But independence is what you make of it. And in the wake of the gilt market crisis of September 2022, relations between the Bank of England and the UK government need a reset. In normal times, there is no doubt that an inflation-targeting independent central bank can serve a country well. But since 2008, the UK and other advanced economies have not had the luxury of such simple problems. To their credit, central bankers around the world have not stood on orthodoxy. After 2008, the US Federal Reserve rescued the global banking system and, through quantitative easing, it stabilised the Treasury market in the face of huge deficits. In Europe, things were trickier. Both the Bank of England under Mervyn King and Jean-Claude Trichet’s European Central Bank played cat and mouse with national governments. This was a high stakes wager that between 2010 and 2012 escalated bond market tension and triggered a disastrous turn to austerity. Shaken by the impact of those shocks, their successors, Mark Carney and Mario Draghi adopted a more protective stance (assuming you were not the government of Greece). Recall that Draghi’s legendary slogan, “Whatever it takes”, was uttered to face down the City of London’s bond vigilantes. In 2015, Draghi launched QE — financial repression by another name. In 2016, Carney used the authority of the Bank of England to stabilise markets following the vote for Brexit, an exemplary demonstration of how central banks can underpin democratic choice, even when those choices are wrong headed. All these were independent central bankers steeped in the best practice of the 1990s, who recognised that historic crises demanded radical action. It was the price surge of 2021-2023 that poisoned the atmosphere. Though the shock came mainly from the supply side, central banks ended up in the dock. Nowhere more so than in the UK. The Bank of England reacted with aggressive normalisation. Faced with a cost of living crisis, the governor called for workers to accept real wage cuts. In early 2022, as gas prices were at record levels and Russia’s army was poised to invade Ukraine, the Bank adopted a stringent programme of quantitative tightening, elevating interest rates. When the Truss government got itself in trouble, the Bank took almost a week to come to the rescue. Rather than enacting a charade of normality, it is time to recognise that in 2025 the UK faces a period of historic transition. To meet this challenge, what is needed is a new concordat with the Bank. This should not ignore inflationary pressures or the long-run trajectory of debt, but should affirm the priority of reviving investment-led growth. One could follow Donald Trump in demanding interest rate cuts. The Bank could shadow the ECB in its commitment to capping Eurozone yields. But the top priority should be to lay the ghost of September 2022. The Bank’s slowing of QT last month was a concession. An immediate and complete end would send the right signal. Such a concordat will not by itself restore sanity to politics, solve the housing problem or rebuild the NHS. But it would help to lift the fear of bond market crisis, which is paralysing the effort by democratic politicians to answer the fundamental questions facing the nation.

Now, that call for a new concordat between government and Bank of Englands seems more urgent than ever. The problem is that in October 2025, Starmer still had some authority. Today the government is in tatters. And when you are the “under the harrow” - to echo a phrase of Montagu Norman’s from the 1920s - it is the worst possible time to consider institutional change. To make general arguments at a time of crisis can only seem like special pleading rather than a general argument for long-term change.

The same, unfortunately, is also true for the other basic institutional reform that Britain urgently needs i.e. the abolition of the out-dated first past the post electoral system and its replacement by a moderated form of proportional representation.

And thirdly - whilst we are saying the quiet parts out loud - Britain needs to reopen the question of EU membership. What the local election results of 2026 show is that this remains a key issue. And what they also show is that there is a clear majority that would favor a return.

Until these basic features of Britain’s political economy are addressed the country will carry on its politics as though in a haunted house, governed by governments that lack actual majorities, conjuring up false constraints whilst ignoring the real ones.

This one is for DG and MI.

I love writing the newsletter. If you enjoy it too and fancy buying me a coffee once a month, you know what to do. Click below!

When Burnham says 'not in hock to bond markets' he means exactly this. The question is whether a Burnham government would have the political capital to attempt a new BoE concordat, or whether the gilt market reaction to his candidacy - 10bp this morning alone on the 10yr - makes that conversation impossible before it starts.

He'll be inheriting Starmerite Labour's mandate, not his own - and a party that just tore itself apart won't suddenly unite behind such a significant leftward shift on fiscal policy

Thanks, that was excellent (also the link to Paul Mason - that provided a great explanation for amateurs like myself) and I have learnt a lot!