Chartbook #39: Blackstone and baby formula - more tremors in the nexus of big money and China's state capitalism.

What have billionaire real estate deals and baby formula got to do with each other? They are both in the crosshairs of the mounting tensions between China and the West.

In the escalation of tension between the US and China, one major counterflow has been the circulation of big money from the West into China.

This is a key theme in Shutdown, where I look at the determined flow of Western capital into China, even in the face of the escalating tension between Trump’s administration and Beijing.

This extensive analysis of the China-positioning of Ray Dalio (of the Bridgewater hedge fund) is particularly striking:

For a running commentary on twitter, this is a great thread from the always excellent @70sBachchan

Many of the biggest financial names have been piling into the world’s second largest economy. Indeed, big Western money was flowing into Evergrande as recently as August, even as tensions mounted and the likes of George Soros sounded dire warnings.

Money flows in various forms - direct investment, acquisition of equities and corporate bonds, purchases of sovereign debt.

In the recent times, what is called “private capital” has been a growth area in global capital accumulation. Robin Wigglesworth of the FT gives a great explanation of this loosely defined field.

Basically, the phrase “private capital” is “handy short code for virtually any asset that is not publicly traded like stocks and bonds.” So private capital includes categories like private equity, venture capital, real estate deals. To extend the handy short code, it is big money deals in which large and wealthy investors deal directly with the businesses and assets they are investing in, sometimes by way of an intermediary like a private equity firm, or the boutique private equity branch of a big bank. It is a business driven by privileged channels of information, access and the ability to sustain illiquid and risky investments in the hope of greater profit.

It is very big business. As the FT reports: “explosive growth in areas such as private equity lifted the size of the overall private capital industry to $7.4tn at the end of 2020, according to Morgan Stanley. The bank expects it to hit $13tn by 2025. … Private equity still accounts for the biggest chunk of the private capital universe, with assets of more than $3tn …”.

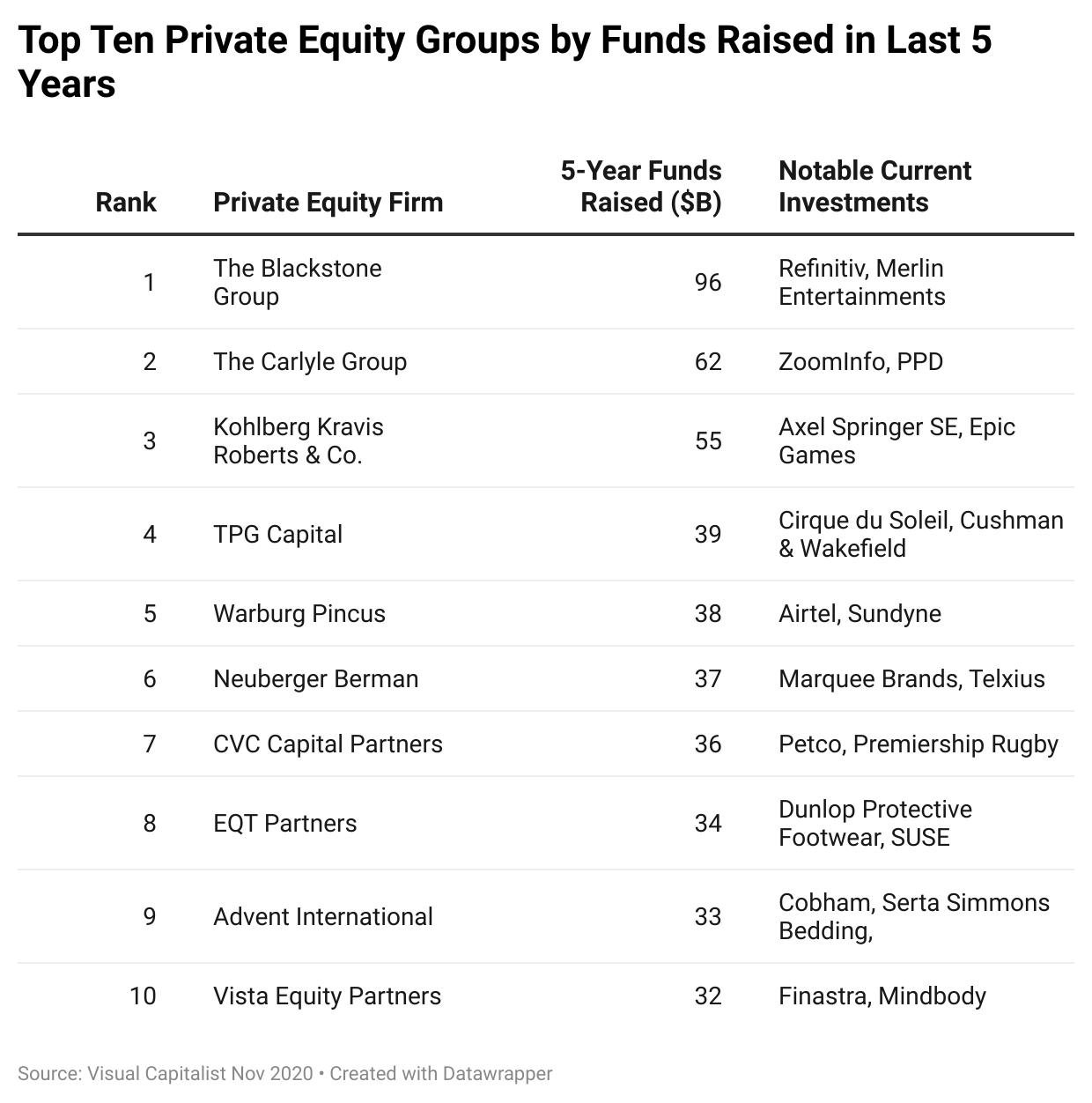

The whale in the private capital pond is Blackstone, with a balance sheet of $648 billion and $96 billion in new funds raised in the last 5 years. Stephen Schwarzman, Blackstone’s boss is a key figure in US finance and politics. As the FT comments, Schwarzman “is no stranger to navigating the choppy waters between Washington and the private sector”.

He is also one of the leading American money men in China. At their peak in 2016, China deals made up almost 40 % of Blackstone’s annual business. Even in the new era of escalating tension, Schwarzman has continued to cultivate his China-connections.

Unlike the managers of big banks or the people who make policy at asset managers, like BlackRock, Schwarzman has truly immense personal wealth. According to the internet, Schwarzman’s net worth is more than $36 billion, compared to barely over a billion for Larry Fink, who runs the far bigger BlackRock, or David Solomon, CEO of Goldman Sachs who is credited with $100 million.

Schwarzman has the means to endow Rhodes-style scholarships at China’s leading university. Both in the US and in China, he has top-level political connections and access to the wealthiest institutions and individuals.

As the WSJ reports, “Blackstone has ramped up investments in China in recent years, particularly in logistics parks and warehouses.” As of June 2021 it had 6 million square meters - 64.6 million square feet - of properties in China on its books.

In 2021, Schwarzman and Blackstone were negotiating a deal to buy out property group Soho China for $3 bn from two of China’s high profile tycoons - Pan Shiyi and Zhang Xin. The offer was made in June. It was conditional on Beijing’s “antitrust” approval. For a well-connected property deal that poses no real risk of monopoly, this ought to have been a formality. In the second week of September, amidst Beijing’s mounting crackdown on China’s wealthy elite, it became clear that approval would not be forthcoming.

A Schwarzman-backed private equity deal in China had gone bad. And that is very big news. It compounds the sense that China’s wealth elite are highly exposed. It puts in question the degree to which personal connections with senior figures in US finance still serve as a conduit between Beijing and the US.

It is not just a deal that broke down. The commentary in the West suggests that an entire model of independent private wealth accumulation and disposal is being put in question from the Chinese side. As the FT remarks, Soho China founders Pan Shiyi and Zhang Xin have been in the spotlight. “The colourful husband and wife pair has been synonymous with the development of the Beijing and Shanghai skylines and the subject of fierce discussion … “You want to flee with your money? You don’t want to stay here and lead us to common prosperity?” asked media personality Zhang Yixuan, writing on Weibo.”

Pan Shiyi’s and Zhang Xin’s webpages at the Harvard Kennedy School Ash Center for Democratic Governance and Innovation are instructive:

Pan Shiyi is co-founder and Chairman of SOHO China, one of China’s largest prime office property developers. Born to a humble family in rural Gansu Province, Pan Shiyi’s has rise to success has made him a celebrity role model for aspiring entrepreneurs, a social media pioneer in China and a highly followed opinion leader with over 17 million fans on Weibo, the Chinese version of Twitter. Deeply committed to environmental causes, Pan Shiyi has been a leading voice raising public awareness for air pollution, leveraging his public profile to inform citizens about the dangers of PM 2.5 contaminants. He spearheaded efforts to develop Energy Saving and Air Purification systems for all SOHO China projects, challenging industries peers to follow suit. Openly crediting his personal success to the opportunities made available to him through China’s economic reform and growth, Mr. Pan is also an active philanthropist. He founded the SOHO China Foundation in 2005 with his wife Zhang Xin, and in 2014 launched the SOHO China Scholarships a US 100 million initiative to fund financial aid scholarships to Chinese students admitted to top international universities. Pan Shiyi and Zhang Xin are also members of the Breakthrough Energy Coalition, a group of global business leaders brought together by Bill Gates to invest in technologies that will transition the world to a zero emission energy future. Mr. Pan is currently a Senior Fellow at the Harvard Kennedy School.

Zhang Xin is the co-founder and CEO of SOHO China, one of the largest prime office developers in China. A renowned business leader repeatedly ranked amongst the “World’s Most Powerful Women”, Zhang Xin is acclaimed for bringing cutting-edge international architects to design iconic landmarks for Beijing and Shanghai. Her personal story emblematic of the “Chinese dream” has made her a social media celebrity with over 10 million followers on Weibo the Chinese version of Twitter. Born in Beijing, Zhang Xin moved to Hong Kong at age 14 where she worked as a factory girl for five years before making her way to England. She holds a Bachelor’s degree in Economics from Sussex University, a Master’s degree in Development Economics from Cambridge University and an Honorary Doctor of Laws from Sussex University. Zhang Xin sits on the Global Board of Advisors for the Council on Foreign Relations, and is a member of the Harvard Global Advisory Council. Deeply involved in philanthropy, Zhang Xin and her husband Pan Shiyi established the SOHO China Foundation in 2005, a charitable organization that promotes education to improve social mobility, and in 2014 launched the SOHO China Scholarships a US 100 million initiative to fund financial aid scholarships to Chinese students admitted to top international universities. Zhang Xin and Pan Shiyi are also members of the Breakthrough Energy Coalition, a group of global business leaders brought together by Bill Gates to invest in technologies that will transition the world to a zero emission energy future.

The Chinese media have been critical of the pair who have “spent more time outside the country recently, after their large donation to Harvard University and US real estate purchases made headlines”.

In the days after the Blackstone deal fell through, Pan and Zhang were seen in the stands attending the US Open tennis tournament in New York, attracting hostile commentary in China. “So they’ve already left,” said one social media user. “They transferred their assets out long ago,” added another.

Bill Bishop in the invaluable Sinocism newsletter remarks on the failed deal and the Chinese power couple:

”Unclear why regulators were taking so long to approve the deal, the SOHO founders had deep ties with now jailed Ren Zhiqiang, good for them to be outside of China now, can't imagine they can return any time soon, nor can Pan's oldest soon from a previous marriage, since he allegedly slandered PLA troops last year after the deadly fight with Indian troops.”

Why could Schwarzman “among the most influential of US dealmakers in China” not get his way? In a highly competitive real estate development market, antitrust cannot have been the real issue.

As one observer remarked to the FT what Beijing no longer seems willing to tolerate is the freedom of the most wealthy Chinese to do with their assets what they wish and especially those with a high, international profile: “We do know individual tycoons are being targeted. The government is saying you’re selling out, going to live in New York and moving your wealth offshore. No chance.” “The reality is that if you created a business in China that’s worth billions, you’ve done so with the blessing of the government, so it’s definitely the wrong time to be cashing in.”

In China there is plenty of big money interested in selling out. Currently, private equity groups have agreed transactions worth $26bn in China though a large part of that pipeline has yet to go through.

On the buyers side, every deal now has to be scrutinized for potential sensitivity. As high-profile fund manager Cathie Wood put it: "We have not eliminated our positions, but we have reduced our positioning in China dramatically and we have swapped some of our holders, which became losers, into companies that we know are courting the government with common prosperity".

Specifically, Wood’s fund, Ark, was investing in “companies seeking the government’s favour included JD Logistics, which Wood said was building infrastructure in third- and fourth-tier cities on extremely low gross margins. Wood also noted ecommerce platform Pinduoduo, which she said was investing heavily in the grocery sector and supply chains between farms and stores. “I think it’s basically investing for free to help the government,” she said, adding that certain companies appeared to be specifically “currying the government’s favour”.”

In June, Hong Kong private equity company Primavera Capital Group bought the infant formula business of Reckitt Benckiser, paying $2.2bn. A few months later, it is far from obvious who would be interested in such a business. As one analyst remarked, “(a)nyone looking to buy or sell companies in that space needs to have a rethink. China is looking carefully at anything that increases the cost of raising children.”

Yup. You read that correctly. The fact that Beijing is trying to contain the cost of baby formula is causing ripples in the global business press.

As one “senior partner” in a “large US-based private equity company” remarked, China is “too important to walk away from”.” And Wood agrees, “we won’t give up on China because they are so focused on innovation and they are so inherently entrepreneurial”.

But picking winners was key. And it is Beijing setting the rules: “If foreign capital assists the people of the country, or doesn’t get in their way, I think you’re fine.” What it is now crucial to avoid is making a “lot of money” in a way that could be seen as profiting “off the people”.

Yup. Once again, you read that correctly. In China … in China … Western investors are picking low margin, common prosperity-winners, that don’t appear as though they are “profiting off the people”. Whereas at home ….

What is going on?

For Lingling Wei of the WSJ the conclusions are dramatic. Whatever line you choose, whether “profiting off the people” or not, Western money needs to be aware that it is now operating in a regime that is operating under different rules.

“Mr. Xi isn’t planning to eradicate market forces … “, Wei says, “but he appears to want a state in which the party does more to steer flows of money, sets tighter parameters for entrepreneurs and investors and their ability to make profits, and exercises even more control over the economy than now … he aims to rewrite the rules of business in what could someday be the world’s biggest economy.”

To confirm this judgement the WSJ has tallied over 100 regulatory actions, government directives and policy changes since late last year.

To describe Xi’s political economy, Wei adopts the concept proposed by Barry Naughton of a “government-steered economy.”

“At internal meetings”, Wei reports, “Mr. Xi has talked about the need to differentiate China’s economic system.”

Wei does not go on to elide Xi’s politics with Maoism, but she does point out that:

“… when the Chinese Communist party celebrated its centenary on July 1, Mr. Xi donned a Mao suit and stood behind a podium adorned with a hammer and sickle, pledging to stand for the people. After the speech, he sang along with “The Internationale” broadcast across Tiananmen Square.”

Once dismissed as mere gesture, China watchers - Wei comments - are now taking Xi’s ideological posturing deadly seriously.

In Wei’s writing in the WSJ the historic break is registered in unselfconsciously sentimental terms as a contrast between Xi’s stern, Mao-suited posturing and the fate of Yu Minhong - the “Godfather of English Training” - the boss of a big private tutoring firm, who was reduced to tears during a recent company meeting. The stock price of his firm has been crushed as a result of new official regulations.

And no one is safe from the turn.

Liu He, once Xi’s right-hand man when it came to economic policy, is alleged to have been forced into “Mao-style self-criticism” for failing to stop the ill-fated launch of Didi’s share offering in New York. As Wei doesn’t fail to remind the readers of WSJ: “Self-criticism … is a practice Mao borrowed from Stalin and remains alive and well in Mr. Xi’s China.” From Xi to Stalin.

And the piece concludes with a flourish. Wei reminds us that in 2018 Xi made clear in the pages of Qiushi that he regards state capitalism “as a transitional economic form”, which “will complete its historical mission and withdraw from the historical stage.” The new buzzword in Beijing is “boluan fanzheng, or bringing order out of chaos”.

A note on Chartbook

I love putting together this newsletter and I love the fact that it goes out free to many readers. But if you are enjoying the read and can afford to support the project, please consider signing up for one of the three subscription options.

The annual subscription: $50 annually

The standard monthly subscription: $5 monthly - which gives you a bit more flexibility.

Founders club:$ 120 annually, or another amount at your discretion - for those who really love Chartbook Newsletter, or read it in a professional setting in which you regularly pay for subscriptions, please consider signing up for the Founders Club.

I live most of the year in Wuhan. Everyone in China knows what's going on, but the garbage I read from every Western fund manager that thinks they have a handle on the situation is mistaken. This is the first piece by anyone in the West that is starting to connect the dots. Good job.

Western elites (and many in the media who report on them) are unable, as a matter of instinct or training, to take others' ideological or moral commitments seriously. That's led them into such confusion during the Trump years and so it's no surprise to see them stuttering in confusion by the same in China.