Chartbook 261 On Europe: A failed project of state-capitalist relations? The Eurozone at 25 (part 2)

Viewed in conventional liberal terms, the EU is an innovative political project. Like other modern polities it has economic policy objectives - price stability, growth, full employment etc - which it realizes through a suite of instruments - monetary, fiscal, industrial, regulatory - framed by an institutional structure i.e. an independent central bank, national Treasuries with budget rules etc. The EU is a highly original political project and European Monetary Union - the Euro - is a work in progress, so getting the balance between fiscal, monetary and regulatory structures right, is tricky. In Chartbook 260, I reviewed various narratives of the development of the European Monetary Union over its first 25 years.

It is in this nature of this kind of approach to the EU’s history and purpose - call it the political history or political science approach - that you arrive at a sisyphean view of Europe as a polity engaged in an endless effort at institutional development, crisis-driven adjustment, construction and reconstruction. The ultimate destination remains open-ended, which suits a liberal worldview. The crucial thing is that the effort goes on. This is also the internal self-perception of the EU, as framed by Jean Monnet’s adage about Europe being the sum of the solutions to each of its crises.

But what if we stand back and adopt the more jaundiced and distanced perspective of political economy? What if we start from the premise that the EU is a regime organized essentially around the interests of a politico-business elite and their political constituencies? What if we - pass the smelling salts - think of the EU as a loosely and liberally articulated, state capitalism.

Clearly, I am using the term loosely here to gesture to any political economic analysis that recognizes the deep, essential and systemic imbrication of state and business interests. By using the label I do not mean to evoke a particular stage of historical development or to foolishly suggest that the US is essentially identical to China. The point is simply to disrupt the standard liberal distinctions between state-politics-policy and economy etc.

If we view the EU in those terms then it is one regime of “state capitalism” in a world shaped by other political economies in all of which state and business interests, elite politics and the functioning of capitalism are inextricably interwoven. Of course there are the Chinese and American variants of state capitalism, the Japanese, South Korean, Saudi and Russian, all variegated, none of them self-contained, all combined and interlinked in a process of uneven and combined development.

Viewed not as a polity with an economy to govern according to certain norms and principles, but as project of elite self-interest organized in a structure of state-capitalist imbrication, how would we judge the euro area’s development over its first 25 years?

For one thing this point of view reminds us that whilst EU governments spend an inordinate amount of time arguing about the arcana of fiscal rules and public debt, the first and most profound existential crisis of the Eurozone was triggered by a crisis of Europe’s banks. In the 2000s, in the “good”, early years of the Euro, Europe’s banks were truly in the forefront of a giant North Atlantic credit boom. Europe was the central interconnector in financial globalization.

The North Atlantic credit boom was centered on Wall Street and the City of London (then part of the EU), Frankfurt and Paris. European megabanks were significant players on Wall Street. There were regional hot spots of credit inflation on both sides of the Atlantic, in Spain as well as in Florida. Tellingly, it is conventional to date the beginning of “America’s” subprime crisis to the failure of a fund managed by Paribas, a French megabank, on August 9 2007. As far as the euro area was concerned, the real estate bubbles that wreaked havoc in Ireland and Spain between 2009 and 2012 were driven by private borrowing and lending, not public debt. And in Greece and Italy too it was the entanglement of bank balance sheets with public debt that threatened the nightmare of a doom-loop, in which sovereign and financial sectors destabilize each other.

It was a private sector crisis, as much as failings in public debt management that exposed the institutional deficits of the Eurozone. When the basic institutional issues of the euro area are described as being the lack of a fiscal policy to match its monetary policy, or the lack of this or that institutional mechanism, what we are failing to say is that these institutional deficits weigh as heavily as they do, because European capitalism does not self-regulate, it does not deliver the right kind of investment in the right places, or the right level of activity and employment. An account of the Eurozone’s institutional and policy issues without an account of European capitalism walks on one leg.

As we have learned during the current round of price hikes, even the issue of inflation - at the core of the ECB’s legal mandate - is not simply a generic macroeconomic problem, or a matter of “labour market pressures”. Price increases too are in large part a matter of political economy, a matter of profit-driven decision-making by more or less powerful business interests.

So, the first phase of the history of the Eurozone was dominated not by institutional politics, but by a runaway North Atlantic financial boom that ended between 2007 and 2012 in an epic bust. This wasn’t peculiar to the Eurozone. Europe’s institutional structure, or lack of it, modulated the shock and how Europe eventually ended up responding to the crisis. But the financial crisis itself was the driver, not institutional birth defects of the euro area.

Clearly, the impact of the euro area crisis for large parts of European society was appalling. In Southern Europe the depression was on the scale of the 1930s. A generation of young people were condemned to precarity and unemployment by terrible choices amplified by weak institutions. By contrast, financial elites were well protected. Banks were kept afloat and losses were apportioned, if at all, with scrupulous care. In distributional terms the inequality was stark. But this featherbedding of European finance, should not be confused with saying that the euro area’s policy-makers managed the crisis in such a way as to provide a strong platform for the recovery or long-run growth of European financial capital. Everything suggests the opposite. In this sense, the euro area crisis truly was an instance of Keynesian policy-failure. Everyone could have been better off with better policies and better institutions. The mismatch of institutions, policies, politics and economic realities is a problem at every level, for “ordinary citizens”, for the balance of European democratic capitalism, but also for the success of the EU as an elite state capitalist project.

To make this point, the comparison with the United States is telling. In the aftermath of the GFC, America’s financial system - ground zero for the crisis - recovered fast and hard. Assisted by state intervention led by both the Treasury and the Fed and expansive monetary policy (though not fiscal policy to the same degree) JP Morgan emerged as the financial titan of the Western world and Blackrock became the world’s leading fund manager. By contrast, Europe’s financial interests suffered a shock from which they have still not recovered.

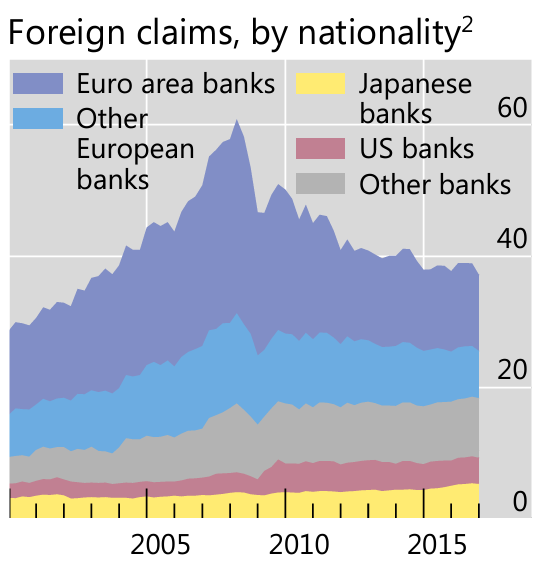

The contraction of Europe’s banks after 2008 was dramatic. Indeed, the contraction of Europe’s megabanks was so dramatic that it left a global footprint.

Source: Robert N McCauley, Agustín S Bénétrix, Patrick M McGuire and Goetz von Peter 2017

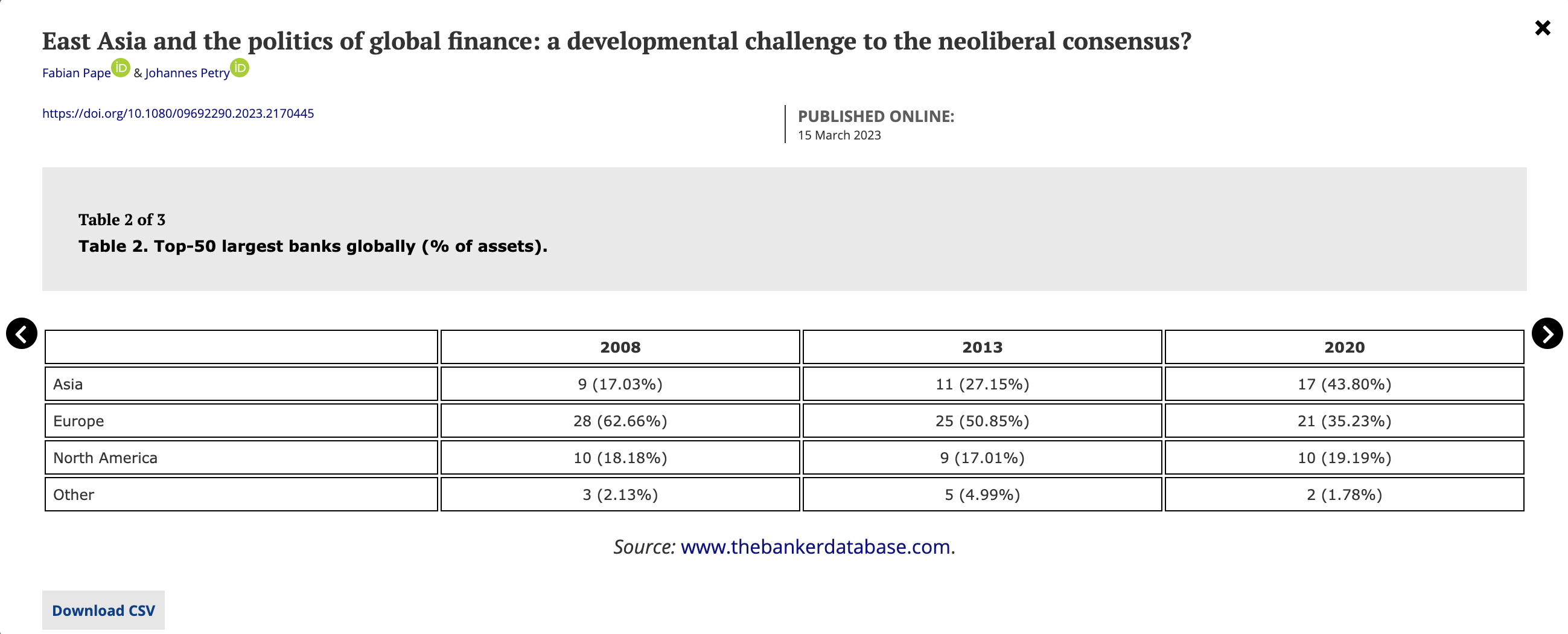

According to BIS analysis, what could be taken for general deglobalization of finance after 2008 was actually a more specific shock. It was the Europeans that deglobalized. Neither American nor Asian banks retrenched. As a result, the biggest emerging market banks, notably those in China and India, now tower above their European competitors.

Source: Paper and Petry 2023

This was welcome in the sense that it made European banks safer. Their capitalization improved. When COVID hit in 2020, the banking system was resilient. When a major European bank did collapse in 2023, it was Swiss, not a euro area G-SIB (global-systemically important bank). Deutsche Bank, widely viewed as the weakest megabank in the euro area, has survived. Faced with the shocks of the Ukraine war and inflation, Europe’s banks have sharply curtailed lending and hedged against rising losses on loans. According to ECB data, since Q4 of 2022 there has effectively been on net lending by European banks to the nonfinancial economy.

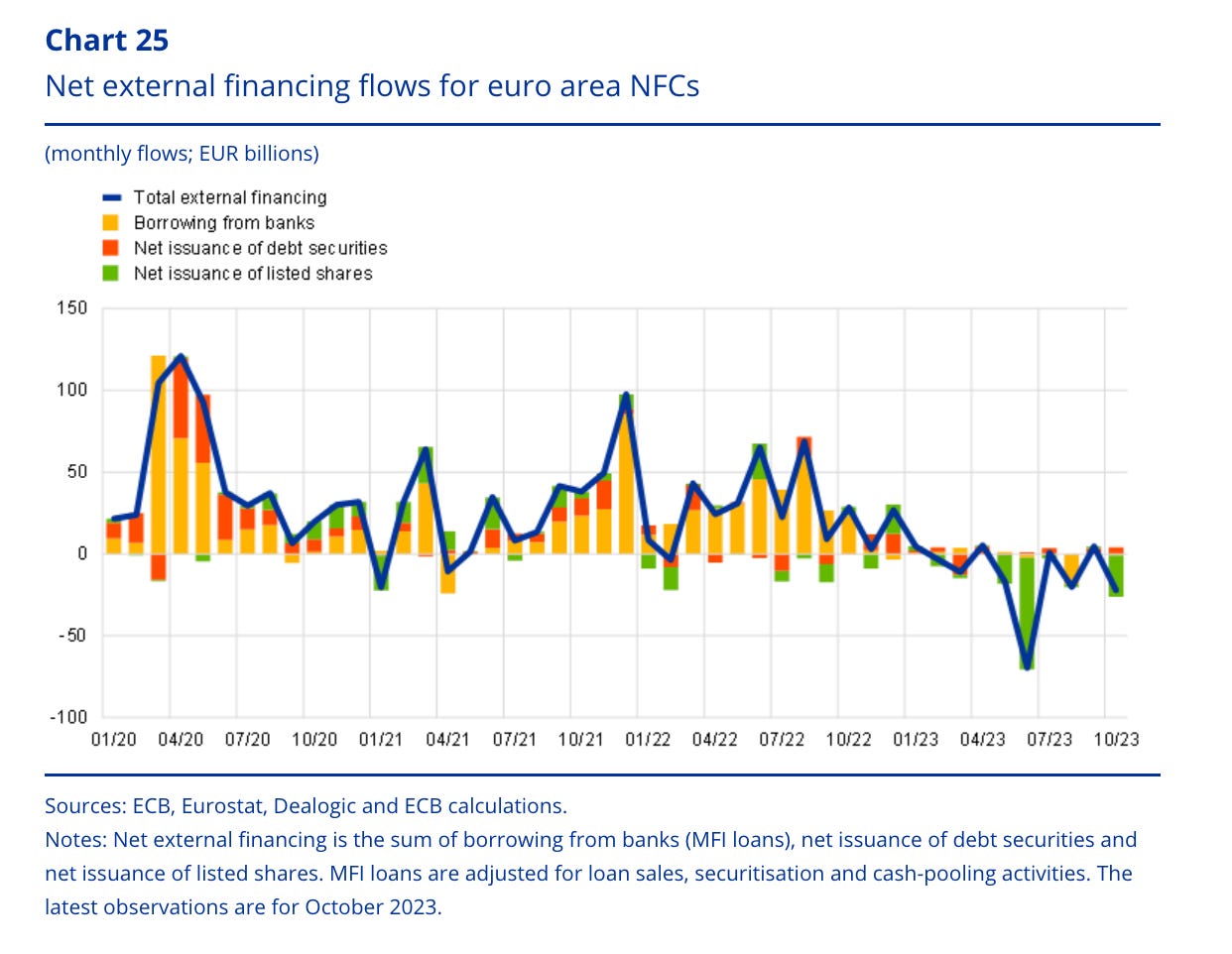

The scale of the collapse in lending comes sharply into view if we set it against the 25-year history of the euro area. We are at a standstill last seen in the depths of the euro area crisis.

Source: ECB Financial Stability Review Nov 2023

This is bad news for the European economy. And despite this retrenchment, serious concerns about financial stability remain. Europe’s banks are seriously exposed to commercial real estate loans, which are going bad on both sides of the Atlantic. There are also worries about bank ties to nonbank financial actors - money market funds on both sides of the Atlantic that provide short-term funding, which could be pulled in a crisis. All of this is offset to a degree by a recent surge in profitability and robust banking capital.

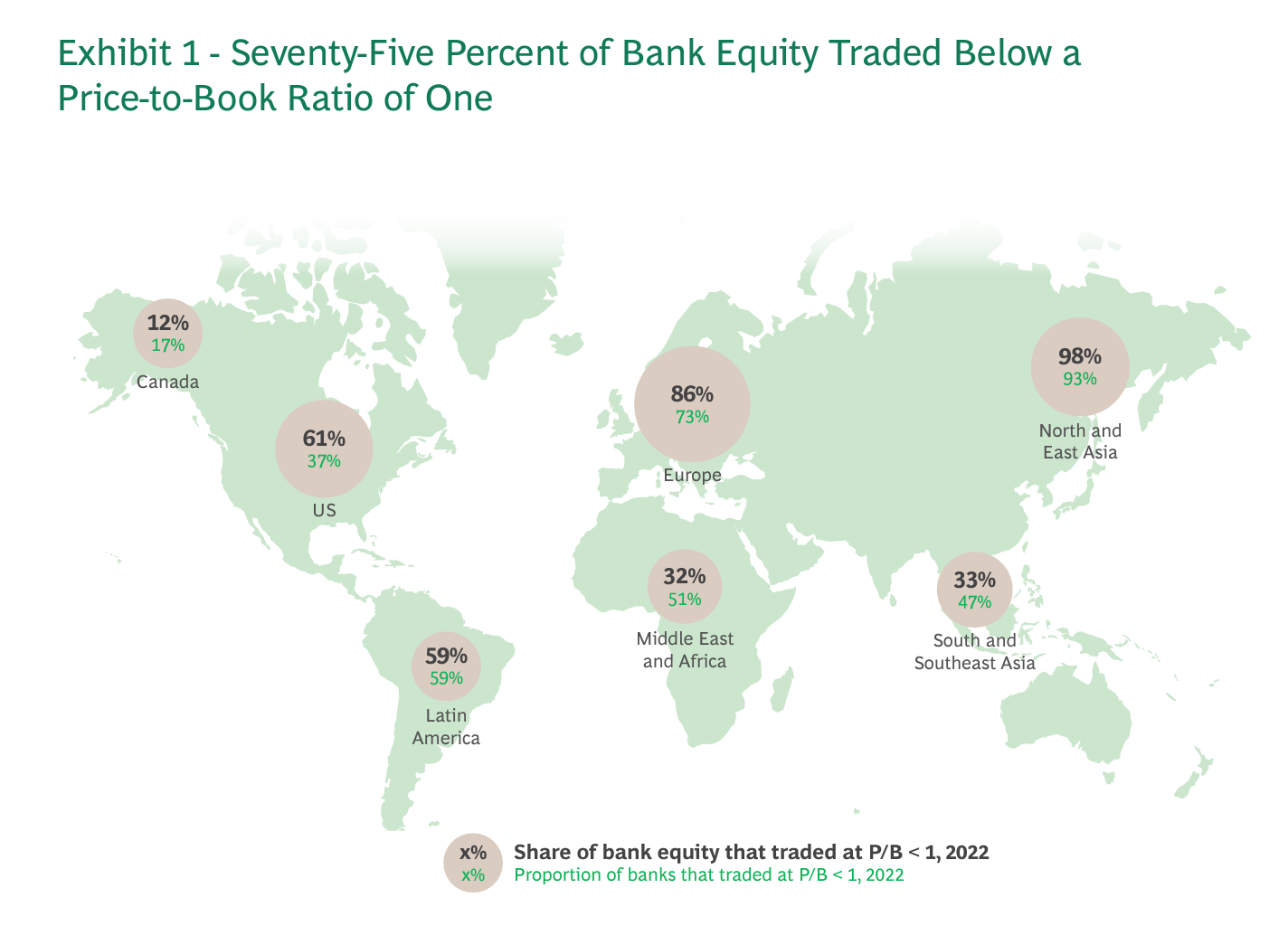

But stepping back from immediate questions of financial stability, what is more striking is the long-run development of the European banking sector. As Patrick Jenkins remarks, judged by conventional business school criteria, the vast majority of Europe’s banks should simply no longer exist. Their underlying assets are worth more than the price put on them by the stock market as corporations. They should be broken up and sold off.

“At business school,” said the seasoned banker, “they teach you a simple lesson — if a company is trading for a sustained period below the value of its net assets then it should be closed down or broken up.” … 73 per cent of Europe’s banks are trading below their book value. The vast majority of them have been doing so for more than a decade. Welcome to the realm of Europe’s zombie banks.

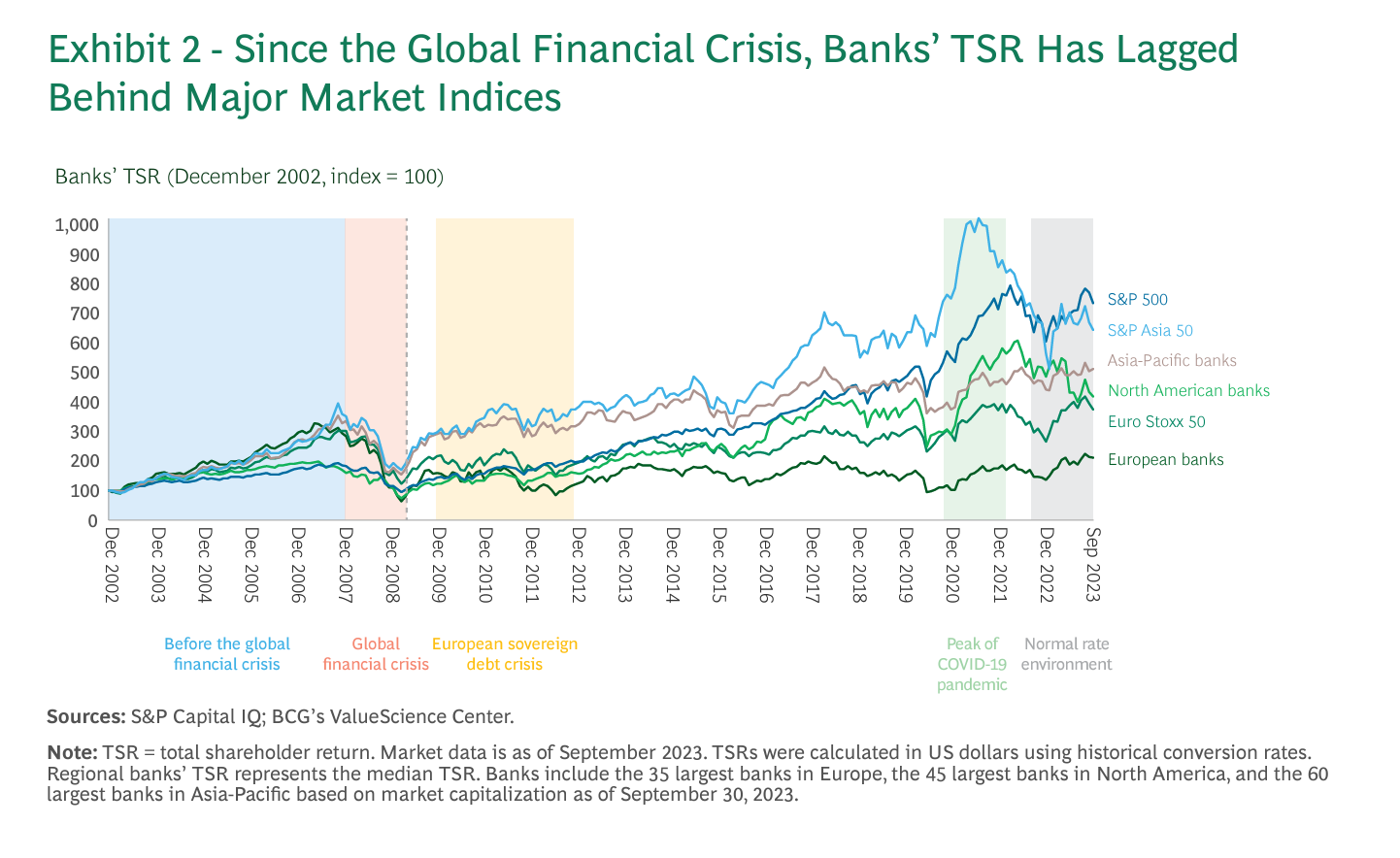

Banking is a tough business. Europe’s banks are not alone in facing uncomplimentary stock market valuations. As a recent sudy by Boston Consulting shows East Asian banks are even more undervalued than those in Europe. But compared to their US counterparts, European banks are hugely depreciated.

Looking at the historical record it is clear that the collapse in European bank stock valuations occurred after 2008. This was initially in line with the experience of US banks, but since the euro area crisis, their trajectory has progressively diverged.

Source: BCG

The ECB is not indifferent to this situation. You might not think that it was a legitimate purpose of a taxpayer-funded public institution to take a view of bank profitability. Europe’s banks are after all privately owned. Their shareholders are often not even European. But the ECB is very concerned and it is macroeconomic and macroprudential logics that form the bridge in the state capitalist synthesis.

The European economy needs credit and no credit will flow if Europe’s banks are not profitable. And the stability of banks depends on their reserves and those depend on profit. Thus the ECB justifies an in-depth examination of why European banks are less successful at earning profits than their American counterparts. The internal, mainstream, “political science” perspective on the EU and the cynical elite-centered political economy view are not separate, they are joined at the hip.

This ECB report merits further attention in a subsequent newsletter but the key argumentative line is the following.

America’s megabanks have established a dominant position for themselves in investment banking, including in European investment banking services. Ranked in order by overall investment banking earnings, the top five firms in Europe, Middle East and Africa are JPMorgan, Goldman Sachs, Bank of America, Citi and Morgan Stanley.

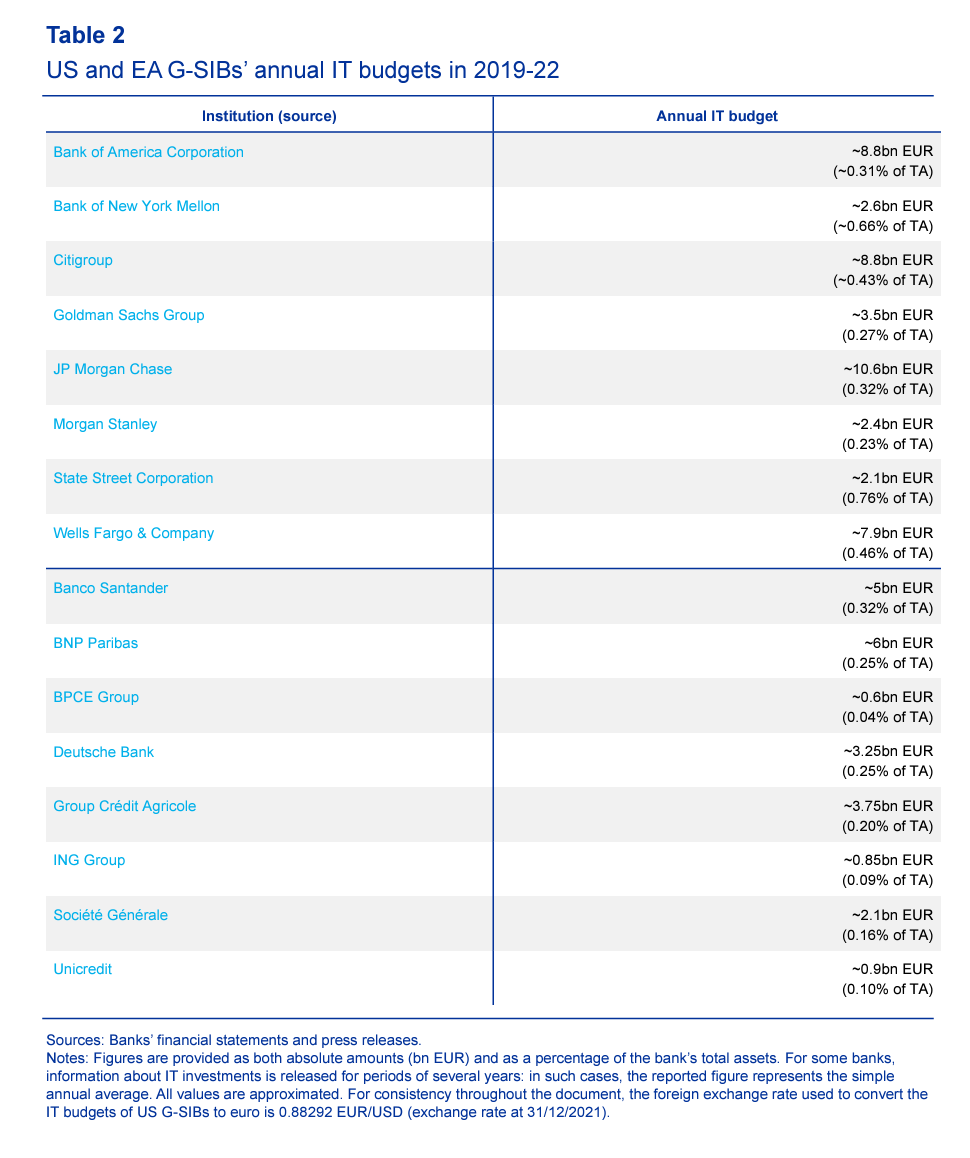

IT holds the key to the future of 21st-century banking. According to the ECB’s analysts the IT investment of America’s top 8 megabanks exceeded that of their 8 largest European counterparts by 46.7bn EUR to 22.5bn EUR.

Size matters in driving this difference. But so does business strategy and that in turn is conditioned by profitability and the availability of funds for investment. It is not just that their balance sheets are bigger. In relation to assets US bank IT spending is 0.36% of total assets compared to a comparable figure of 0.19% in the euro area.

As the European banks have fallen behind and become undervalued a self-reinforcing loop kicks in. Were Deutsche Bank, for instance, to want to takeover its last remaining German rival, Commerzbank, or ABN Amro in the Netherlands, it would have to raise funds. To do so it would need to issue shares. But its shares sell at a 40 percent discount to the book value of its tangible assets. So this makes it prohibitively expensive to raise the capital necessary. Rather than expanding, Deutsche concentrates on slashing costs by shedding jobs.

But, as the ECB team insists, it is not just business strategy that matters here. Business strategy reacts to macroeconomic environment, which is set by the institutional structures and policies pursued by the ECB and other key euro area policy makers. There is a dialectical back and forth between structure and agency. And in the euro area this has not worked to the benefit of Europe’s financial interests.

… banks’ return on equity (ROE) has fluctuated around 5% in the EA, but around 10% in the US, indicating a profitability gap of around 5 percentage points…. Our analysis highlights two main drivers of US G-SIBs’ higher profitability. First, the higher income from fees and commissions and trading of US G-SIBs explains the bulk of the difference in ROE. Second, EA G-SIBs are still dealing with legacy nonperforming exposures built up during the Global Financial Crisis (GFC) which have driven up the associated impairments and provisions expenses beyond that of US peers. …, our main conclusion is that the higher profitability of US G-SIBs compared with their EA peers can largely be explained by their different business strategies, which are closely linked to the differing macroeconomic environments and financial systems in which these banks operate.

The upshot as the euro area reaches its 25 year anniversary. If it has not failed, as a project of state capitalism it has not prospered either. And senior officials in the euro area are remarkably frank in admitting as much:

“The European Union needs more giants like JP Morgan”, remarked Andrea Enria, the outgoing chair of the ECB’s Supervisory Board, in December 2023, in his farewell interview with ECB President Christine Lagarde. Enria is, one might say, a “typical” member of the EU elite: Bocconi and Cambridge trained, a central banking economist and regulator. He openly identifies the interests of the EU and the euro area with a state capitalist vision shaped in the Wall Street image.

Insofar as Europe has a banking champion that can contend with the big US banks it is BNP Paribas. It is the only EU bank that ranks in the top 10 in terms of investment banking revenue.

But rather than European, BNP is quintessentially French, enjoying an extraordinarily tight network across French public service and business. As the work of Cornelia Woll shows in 2008 BNP Paribas stood at the heart of network of political and business influence that if anything resembled that which organized the crisis response in the US between Wall Street and Washington.

Amongst historians of economic policy there is little doubt that over the course of the last 25 years, it is the Italian and French view of central banking that has won out in the management of the ECB over the conservative orthodoxy of the Bundesbank. What is less often remarked is that it is also French financial capital that has done far better than its German counterpart over the last quarter century. At the 25 year mark, whether the Paris-Frankfurt axis can provide a platform for the successful development of Europe as an elite project, in the face of tough global competition, is an open question.

As an economist I make a pretty good retired English professor, but if I may say so, I find that your analysis begins at a high level of abstraction & ends with a plunge into details without ever making a strong argument for the former causing the latter. You could be quite right about the superiority of your analysis over that of the conventional wisdom, but I don't think you've made your case.

Stepping further back and looking at the polycrisis, there is a fundamental question about the role of capital and it's expectations of continued privileged position in terms of rates of returns and power. Pick up on the Piketty analysis, and the questions are also about the growing economic disparities that are inherent in the current capitalist system. Then the observation can be that the rates of return in the US are too high, rather than being too low in Europe.