Chartbook #185 Inflation and distributional conflict - in 2023 not 1973! Also a response to the debate around that Blanchard thread.

2022 ended with the West’s two major central banks somewhat out of step again. The Fed is slowing the pace of rate increases. Meanwhile hawks at the ECB are signaling further steps towards severe tightening, even as inflation across Europe begins to cool.

Thinking ahead, on 28 November, one of Europe’s most prominent economists, Olivier Blanchard, published a piece in the FT reviving his call from 2010 for the world’s central bankers to revise their commitment to a 2 percent inflation target. Back in 2010 along with Giovanni Dell’Ariccia, Paolo Mauro, Blanchard called for a 4 percent target. In light of our recent experience, Blanchard has come to view 4 percent as too high. Empirical research seems to show that 4 percent is the level at which consumers begin to get jumpy about inflation. Inflation becomes salient and with that salience, the organizing sense of price stability is lost. But a 3 percent target still seems better to Blanchard than 2. More specifically, he warns that

when, in 2023 or 2024, inflation is back down to 3 per cent, there will be an intense debate about whether it is worth getting it down to 2 per cent if it comes at the cost of a further substantial slowdown in activity. I would be surprised if central banks officially moved the target, but they might decide to stay higher than it for some time and maybe, eventually, revise it. We shall see.

The hawkishness of recent comments from the ECB plus this scenario of agonizing and brutal efforts to squeeze inflation down from 3 to 2 percent may help to explain why Blanchard chose to end 2022 by launching a twitter thread, which has since kept the economics social media scene buzzing.

Is it surprising that Blanchard should lay out these elementary propositions? Only, if you start from a straw-man version of monetarism in which inflation is always and everywhere (nothing more than) a purely monetary phenomenon.

Setting that straw-man aside, a model of inflation without active price-setting does not make much sense. Someone has to raise their prices and then others have to follow. Otherwise no inflation.

You might say that Blanchard’s list of participants in the inflationary struggle is rather limited. A historical inflation theory would also require us to consider other stakeholders, notably bond holders. But they come into play less as drivers of the process than when we consider the political pressure that might be brought to bear to “force” firms, workers and taxpayers to stop the inflationary spiral.

On the other hand, Blanchard’s statement that inflation is “fundamentally” the result of distributional conflict, makes a lot of people antsy because a pure conflict theory doesn’t work. An inflation theory ultimately needs some mechanism of monetary expansion, otherwise the real value of the money stock is sharply reduced etc etc. One reading is that Blanchard knows this and doesn’t feel the need to spell it out. Another is that there doesn’t need to be a conscious political decision to offer monetary accommodate to the inflationary struggle, because credit expands endogenously.

So, if all of this is simply common sense, what is the kerfuffle about?

Is the most surprising thing that Olivier Blanchard is referring to distributional conflict? Blanchard is a high-status figure with standing in mainstream ranks. Claudia Sahm picks up on this, illustrating her latest post with some rather striking imagery!

Post-Keynesians Lavoie and Rochon immediately responded with a carefully worded tactical note on the question of whether the mainstream is once again appropriating postkeynesian views, or whether this might be the opening to more fruitful collaboration.

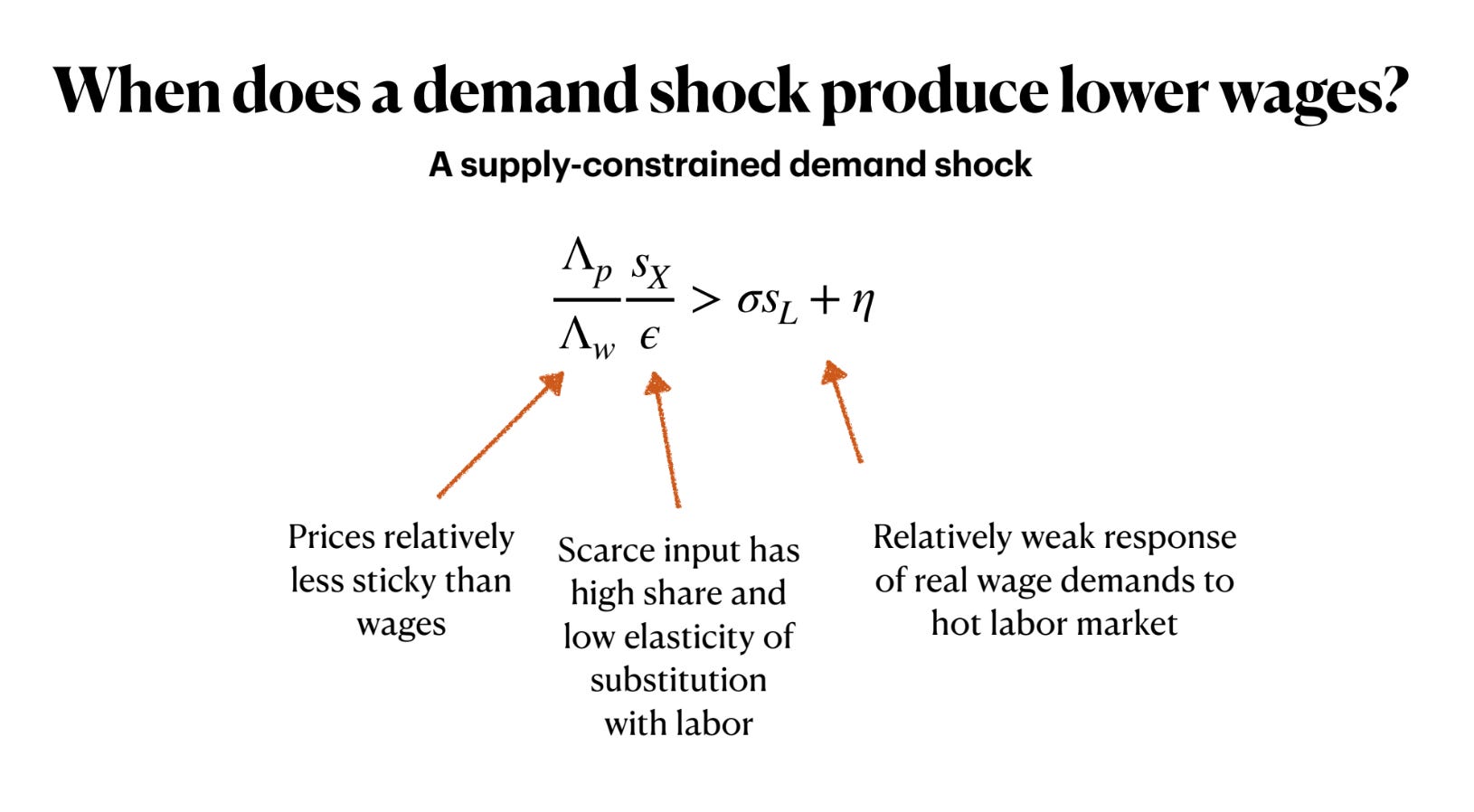

Meanwhile, Guido Lorenzoni and Iván Werning who hold jobs at Chicago Booth and MIT cheerfully chimed in to say that they had just finished a paper in which they had painstakingly demonstrated that wage-price spirals can happen in standard New Keynesian models and that an aggregate demand stimulus can, in fact, lead to lower real wages, but that running the economy hot may also be optimal.

So as Sahm points out, there is actually quite a lot of variety of thinking about inflation out there. Certainly, as far as Blanchard is concerned his willingness to talk about distributional struggle should be no surprise. He is a smart and open-minded person, more a door-opener than a gatekeeper. He was a student in Paris in 1968. He read Rowthorn, the British Marxist and sometime editor of Black Dwarf, and formulated his own version of the price setting model already in the 1980s together with Kiyotaki.

Source: IMF

So, if the content and personage are not surprising, to me the really noteworthy thing about the conversation is its other-worldly quality. Blanchard’s argument for a 3 percent landing zone for inflation is well taken. He is no doubt right about that. And the current inflation is a major distributional event, like any 8-10 percent inflation must be, however short-lived (not to say transitory). But how much conflict are we actually seeing? How much struggle? Perhaps with the exception of the UK, where there is something akin to a general crisis of legitimacy, has there ever been an inflationary process more docile than this one?

Outside the more conservative corners of European central banking is there anyone, anyone at all, who is seriously worried about wage-price spirals? Here is Isabel Schnabel the “German voice” on the ECB:

As Schnabel says, real wages have fallen and now price inflation is cooling too, not just in the US but in Europe as well. The most powerful industrial trade union in Europe, IG Metall, settled for a deal which even The Economist magazine had to concede was an exercise in moderation. The service sector union, Ver.di with strong representation in the public sector may take a more militant stand. But since many public sector services aren’t directly priced, the feed through from wages in the public sector to prices is indirect at best.

This does not mean that the current inflation does involve elements of a social process that could metaphorically be described as struggle. But the “struggle” in question is between different groups of producers over the size of their mark-ups and how much they can pass through to their customers and ultimately households as final consumers, another group that Blanchard does not mention. This kind of supply-side driven inflation has been modeled in an interesting way by Isabella M. Weber† Jesús Lara Jauregui‡ Lucas Teixeira§ Luiza Nassif Pires.

But to call this kind of cost pass-through, “conflict inflation” is to stretch what classic political economy or sociology intended when it referred to conflict. In general at least, divisions between producers and arguments over mark-up, do not have the same strategic or political importance attributed, for obvious reasons, to conflicts between employers and employed, capital and labour. Even when price surges rip through the budgets of poor people, unleashing the discourse of a cost of living crisis and demands for price controls and excess profit taxes, the politics are those of welfarism and distribution, not the politics of power and control. You don’t have to fetishized the process of production to acknowledge the difference here.

In light of the current situation I can’t help feeling a sympathy for those who are impatient with arm-waving about conflict theories of inflation and wistful reminders of corporatist days gone by,.

To my mind the most remarkable bit of the Blanchard thread are the concluding points where he refers to what is simply plain old corporatism as a “dream”.

And then observes that what is lacking is “trust”, rather than organization, a balance of power and a political process that is open to the direct discussion of distributional issues, rather than deliberately and strategically closed against them in the name of higher values like “price stability”. In those lines power, interests and political economy evaporate and are displaced by social psychology, in the form of trust. If these are really the grounds for an inner-disciplinary reconciliation across the camps of economists, it is surely a suspect reconciliation at best.

And the puzzle is that Blanchard is far from oblivious to all this. See for instance his comments here:

Obviously, it is true that fighting the so-called second round reaction involves accepting the distributional status quo as a given. This was made abundantly clear in the reactions to Andrew Bailey’s comments about wage restraint.

But important as that point is, the more important question is why in 2023 we are still talking about a situation half a century ago. What we most urgently need is not so much a revival of conflict theories of inflation that were appropriate to the 1970s and 1980s. What we need is an adequate model of inflation and policy-making under conditions prevailing in 2023, of extreme asymmetry of bargaining power, deadlocked democratic politics and a consequent lack of social contestation, even when real wages are taking a painful hit. Wherever we stand on the politics of organized labour, it is incumbent on us to at least register the novelty of the situation.

****

Thank you for reading Chartbook Newsletter. I love sending out the newsletter for free to readers around the world. I’m glad you follow it. It is rewarding to write, but it takes a lot of work. What sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters, click here:

I can't help tying this discussion with Michael Pettis book "Trade wars are class wars". The issue is real of global demand. For real shift in power to labour and for real wage growth, you need structural changes in big surplus economies of China, Germany, Korea and Japan. A higher share of national income to GDP will result in higher wage growth across the globe. And if not managed appropriately, can result in wage price spiral.

But that seems unlikely and hence the world can easily revert back to a deflationary environment with even a mild recession (and without further disruption in energy supplies)

"What we need is an adequate model of inflation and policy-making under conditions prevailing in 2023 of extreme asymmetry of bargaining power, deadlocked democratic politics and consequent lack of social contestation, even when wages are taking a painful hit."

Maybe it is time to explore and articulate more clearly the type of potential massive bureaucratic involution, or new logic of domination that has taken place in the United States over the past 60 years in which no real opposition to the status quo is allowed to exist--alluded to immediately above in your description of the asymmetry of bargaining power and lack of social contestation now predominant organizationally in our country.

This extremely successful strategy of basically sponsoring one's own opposition ( i.e. one example being labor unions encased and controlled within a more powerful corporate/ bureaucratic state) may have now reached a dead-end since such a strategy now only seems capable of generating greater economic, political and cultural instability.

How about thinking about the necessity of creating social space for real opposition in order to save our society!