Chartbook #179 Finance and the polycrisis (5) The hunt for the next market fracture.

What will bend, what will break? That is the question about the global financial system that I have been asking in this mini-series on Chartbook.

The same question was taken up a week ago under the title “Financial instability: the hunt for the next market fracture” by a crack FT-team consisting of Eric Platt and Kate Duguid , Tommy Stubbington and Jonathan Wheatley and Leo Lewis.

The piece is so close to my own analysis that it caused me to pause and to compare notes. How do we think and write about stresses in the global financial system now?

Eric Platt opens the compilation with a short overview. His opening line aptly summarizes the common sense: “After a decade of falling interest rates and central bank largesse, global financial markets are facing a reckoning.”

This line is echoed by a roundup in the Economist.

The plunging markets are the result of a decades-old macroeconomic regime falling apart. High inflation, not seen in the rich world since the 1980s, is back, which in turn has brought to an end ten years of near-zero interest rates. As a result, the rule book of investing is being rewritten

Whereas the Economist goes on to assess portfolio allocation choices under the new circumstances, the FT team is more focused on the immediate anxiety of market fragility and as Eric Platt explains that is above all a matter of liquidity.

Soaring inflation is being met by rising interest rates, the slowing of central bank asset purchases and fiscal shocks, all of which are sucking liquidity, the ability to transact without dramatically moving prices, out of markets. Violent, sudden price moves in one market can provoke a vicious loop of margin calls and forced sales of other assets, with unpredictable results.

That in turn makes market participants very jumpy. In the words of one interviewee they start trading on “impulse”. And in our world of the polycrisis there are plenty of “impulses” to move the markets. As Platt summarizes it:

Disparate shocks — like the closure of the nickel market in London, structured product blow-ups, the bailout of European energy providers or the rapid pensions crisis in the UK sparked by turmoil in the country’s government debt prices — are being scrutinised as oracles of wider dislocations to come.

This strikes me as a fairly characteristic statement of the polycrisis condition.

Highly disparate disruptions, which are themselves the result of structural factors (e.g. reorganization of the UK pension industry), political decisions (Trussnomics) and macroeconomic policy (Bank of England policy) combine with the broader unwinding of the familiar lowflation setting against the backdrop of pandemic-recovery (oof the polycrisis stretches sentence structure) to leave market participants trying to figure out what is what. As Platt summarizes it, they are left asking the question: How does the clutch of disparate shocks we are experiencing in the current moment, relate to further dislocations that will be wider and are yet to come?

You might be tempted to say that this is the situation of every actor in modern history. But as The Economist points out, for several decades investors have in fact been able to operate within a framework that was defined by the mantra of TINA - There is No Alternative (to a risk-on strategy of yield and growth-chasing in a lowflation zero-rate world). Now we are in a world of TARA - There is A Real Alternative.

So, at least as far as recent decades go, this sense of disorientation is new. But how historically unique is it?

Is the current sense of polycrisis merely another symptom of the breakdown of neoliberalism, TINA etc etc? That was the case made to me recently by Paul Krugman. I will return to that in a future post.

In the mean time let us focus on the present and the question of what might break. Following Platt’s introduction, the FT essay consists of a series of short pieces by each of the contributors.

European repo markets - Tommy Stubbington

US Treasury market illiquidity - Kate Duguid

Japanese government bond market dysfunction - Leo Lewis

Stuck in (corporate and private credit) - Eric Platt

EM market defaults - Jonathan Wheatley

It’s a good list. I have many of the same items on my worry list too. But I also wonder whether it is significant that it is a list rather than a single “integrated” essay, as in The Economist presentation. Is the list a characteristic response to the polycrisis? Is that one of the things that triggers intellectual dissatisfaction with the polycrisis term? That it seems like a “laundry list”.

Lists lack structure. They beg the question of order and weighting. What is the underlying principle that organizes the separate points? Are they an expression of our mental incapacity to satisfying synthesize or to discern the deeper underlying logic? Are they, indeed, something worse, a failure to face up to the stark fact that at the root of everything there is one basic causal driver? Capitalism, for sake of argument. To that extent is the “baggy” (not to say carrier bag) theory of polycrisis an ideological snare, a failure of intellectual backbone, of moral fibre on the part of the analyst?

Obviously, I think not. In fact, I’m persuaded by the opposite point of view. If you are not willing to face the “baggy”, inchoate nature of our current situation, if you are not willing to take seriously the possibility that our situation is historically novel (as in a product of the “great acceleration”, of which there is a dawning awareness in social and environmental sciences since the 1970s etc etc) and that this fundamentally challenges our existing frameworks of analysis (as grasped amongst others by Ulrich Beck), then you are involved in a kind of escapism that may turn out to be dangerous. But let’s come back to that on another, more leisured occasion.

Let’s pivot, as we must in this day and age, from broad considerations of the anthropocene and the polycrisis to more technical issues of macrofinance. Because, as you would expect, there are some really interesting features in the FT’s list.

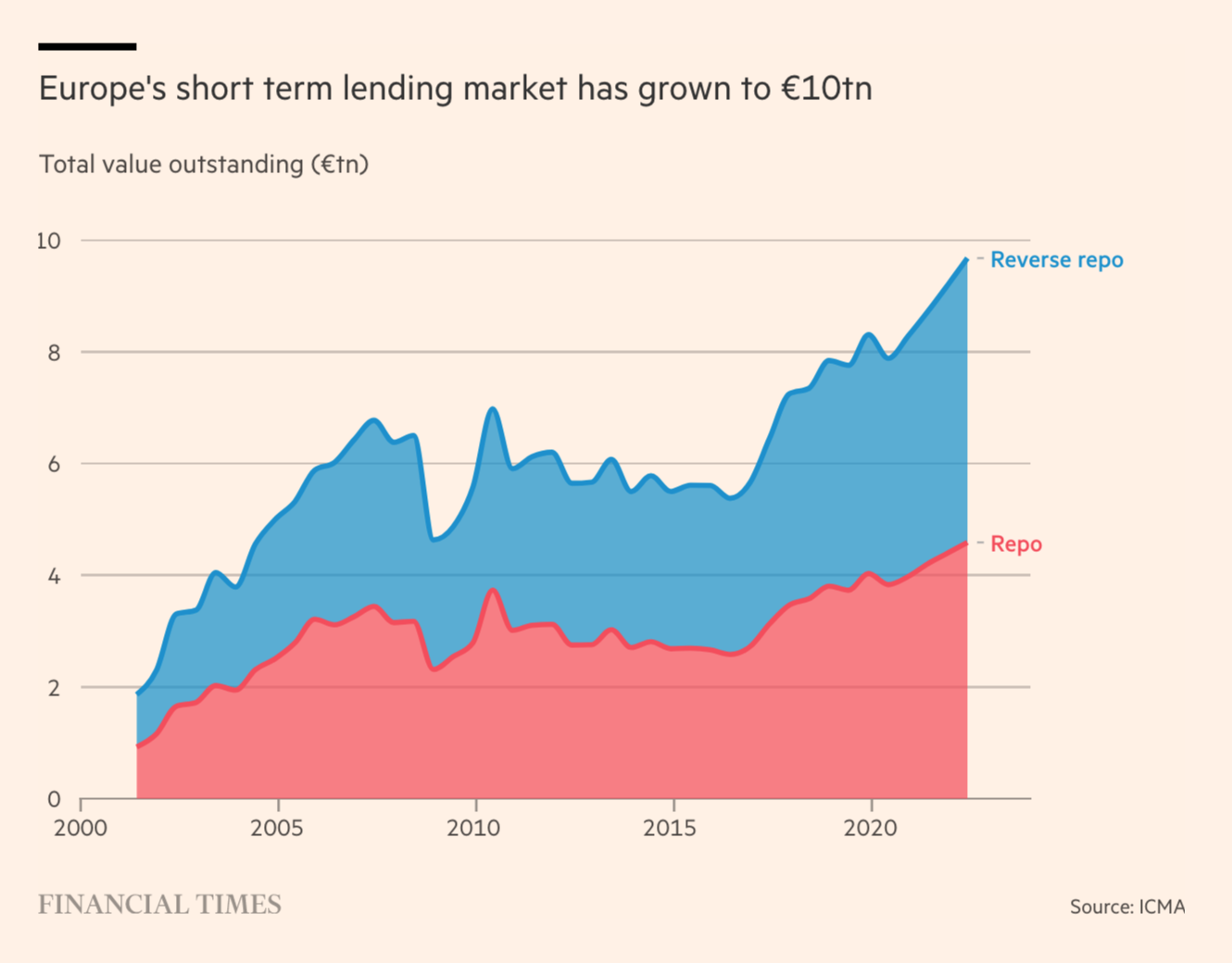

I did not have the Eurozone repo market high enough on my list of worries. One thing that Tommy Stubbington highlights is just how big the Eurozone repo market has become.

The issue in the repo market is that quantitative easing purchases by the ECB means that there is not enough super safe, short-term government debt in private hands for large-scale investors to use as the basis for short-term cash loans. Excess demand for that category of debt means that prices are high and yields low counteracting the effort by the ECB to raise interest rates to counter inflation. The result is an unstable tug of war. The securities industry is lobbying for the ECB to ease the tension by introducing the kind of standing reverse repo facility that the Fed put in place in 2013 with which to supply the US Treasury market with a flexible supply of collateral. But the ECB has actually pushed back against the idea. Watch this space.

On the other side of the Atlantic the Treasury market is not looking healthy either. I reviewed the wide-ranging debate about Treasury market conditions in Chartbook #172. In her contribution to the FT roundup Kate Duguid nicely summarizes the position by stressing that structural distortions may now be so severe that it may not even take a major shock, as in 2020, to unleash a self-propelled round of fire sales.

“… in the event of a crisis, structural problems may exacerbate any sell-off, as was seen in March 2020. But the current liquidity issues in the Treasury market also mean it may not take an event as disruptive as the onset of a global pandemic to spark a big sell-off. If some mis-step prompted a dash for cash, investors could have trouble selling Treasuries, leading to huge swings in prices, producing big enough gaps in prices to lead to forced selling.”

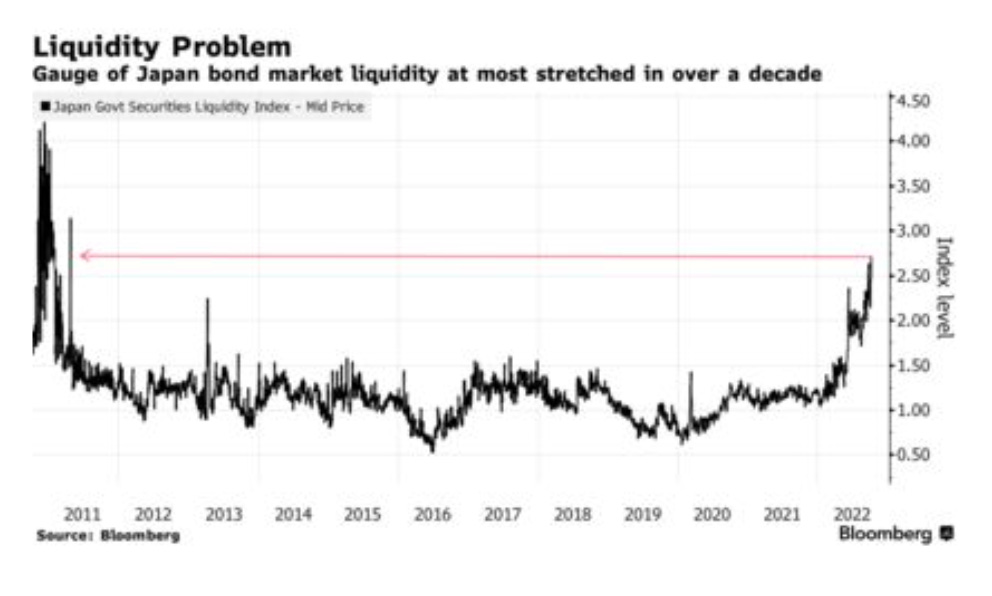

Both the Eurozone and the US sovereign debt markets are clearly sticky right now. But if you want to see a government bond market that is altogether ruled by central bank policy, look to Japan. The Japanese market is dominated by years of yield curve control exercised by the Bank of Japan, which have driven interest rates to zero and held them there. The question here is if and when the BofJ might shift position. The interesting point noted by Leo Lewis is that there is a significant difference of opinion between Japanese and Japan-based analysts who remain convinced of the BofJ’s commitment, and foreign analysts who don’t find it plausible that the Bank of Japan can in the long run buck the global trend towards higher rates. Something has to give.

This year the Bank of Japan has engaged in bond purchases at a rate not seen since 2017. To ward off speculative attacks it has offered on occasion to purchase unlimited quantities of 10-hear Treasuries. As a result it now owns half of Japan’s government debt.

In the meantime Japan’s bond market no longer works like a “normal” market. What this means is that for three sessions strait in October the Japanese 10 year bond failed to trade at all.

“There is no incentive to buy the 10-year notes from a carry income perspective or for trading purposes,” said Ataru Okumura, a strategist at SMBC Nikko Securities Inc. in Tokyo. “It’s hard for investors to hold 10-year bonds for the longer-term as the sector being the BOJ’s yield curve target makes it expensive relative to other parts of the curve.”

As one market participant observed:

“I hope the BOJ will realize soon that it’s destroying the bond market,” said Ayako Sera, a strategist at Sumitomo Mitsui Trust Bank Ltd. in Tokyo. “It could at least stop conducting the fixed-rate operation every day once the Fed stops hiking rates.”

Even allowing for the exceptional circumstances in the 10-year bond market, which is where the BoJ concentrates its interventions, the overall liquidity in Japanese government debt has fallen to levels not seen for more than a decade.

In short, the major public debt markets of the world - US, Europe, Japan - are looking far from healthy. In addition there are concerns about the corporate debt market on both sides of the Atlantic.

I addressed the European corporate debt crunch in an earlier Chartbook in this series. Recently, Eric Platt and Harriet Clarfelt warned of the shock to the US junk-bond market. Issuance so far this year has fallen to levels not seen since 2008. At $101bn they are less than a quarter of the issuance of $464bn in 2021. This is hardly surprising in light of the collapse in prices.

Less debt issuance points to funding stresses for business. But that is what one would expect at this point in the business cycle. That is bending not breaking. As far as financial stability is concerned the big concern is that a fire sale dynamic might develop that would destabilize open ended bond funds. They remain one of the critical weak links in the global financial system.

Finally, Jonathan Wheatley, addresses concerns about risks in the emerging market economies. Currently, the credit rating agencies say that 26 developing countries are either at risk of default or already in default. This is alarming, but as Wheatley points. out the scale of the problem is not systemic. As Wheatley reports, the “15 countries with bonds trading at distressed levels in October made up just 6.7 per cent of the benchmark JPMorgan EMBI sovereign eurobond index”. This may be callous, but it is reassuring from the point of view of overall financial stability. As Wheatley points out, however, beyond the immediate crisis cases a more serious concern should be that contagion may spread to larger EM economies. Recently, Poland, Colombia and South Africa have all seen yields on domestic 10-year bonds rise to record levels.

In recent weeks, the market situation for the big EM has eased somewhat. Colombia has been welcomed back to the market. With all the talk of the Fed easing the pace of monetary tightening, is the worst of the shock over? It would certainly be nice to think so.

But, debt levels are high. After the initial shock of rates rising, the system will have to adjust to living at those elevated levels. In that scenario, the sustainability of the Bank of Japan’s position is a huge question mark. There are major institutional fragilities in repo markets and in open-ended investment funds. All three major sovereign debt markets are showing signs of dysfunction. And one thing we must count on is that there will be more shocks to come.

****

Thank you for reading Chartbook Newsletter. I love sending out the newsletter for free to readers around the world. I’m glad you follow it. It is rewarding to write, but it takes a lot of work. What sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters, press this button.

Several times per week, paying subscribers to the Newsletter receive the full Top Links email with great links, reading and images.

There are three subscription models:

The annual subscription: $50 annually

The standard monthly subscription: $5 monthly - which gives you a bit more flexibility.

Founders club:$ 120 annually, or another amount at your discretion - for those who really love Chartbook Newsletter, or read it in a professional setting in which you regularly pay for subscriptions, please consider signing up for the Founders Club.

To get the full Top Links and become a supporter of Chartbook, click here

Can't look at Japan without looking at Norinchukin. The interest rate risk in their banking book is off the scale: https://www.netinterest.co/p/farmers-that-finance-the-world