Chartbook #150: Why "cheap Russian gas" was a strategic snare but not the secret to German export success.

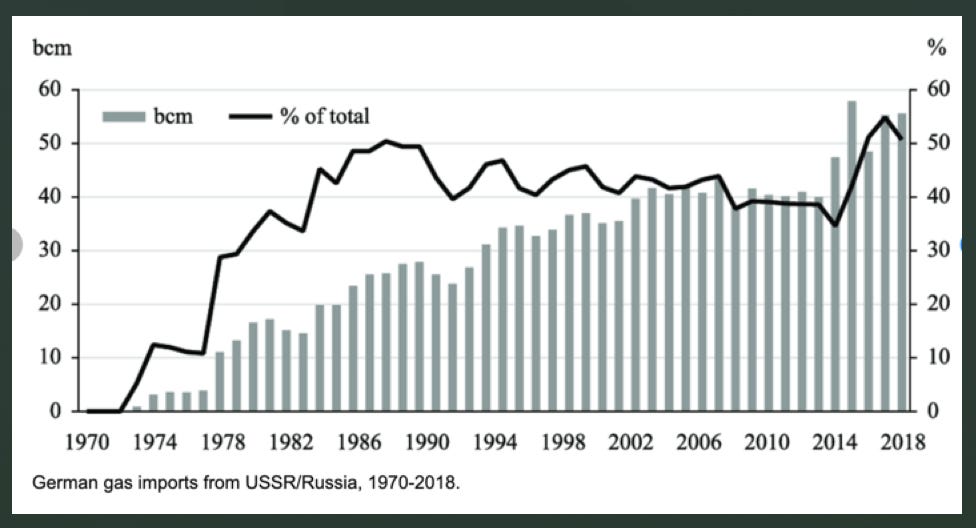

Right now German grand strategy is in the crosshairs of criticism. Germany is faulted for having appeased Putin. It is faulted for having neglected the Bundeswehr and on top of that, the Federal Republic is facing an energy crisis like none other in its history. Gas deliveries from Russia have been severely curtailed if not halted altogether, exposing the dependence of German energy consumers - both households and industry - on pipelined gas from the East. Critics of German strategy point out that the risks of dependence on Putin should have been obvious at least since the Russian annexation of Crimea in 2014. And despite that, the share of Russian gas in German consumption continued to increase not decrease. At the same time, Germany phased out its nuclear reactors and failed to accelerate the energy transition, leaving itself even more vulnerable.

As the cold weather of the autumn and winter approaches, Berlin faces not just an acute functional problem, but something akin to a legitimation crisis, a situation which I analyse at some length in the speech I was honored to give in memory of Willy Brandt in Berlin last week.

The video (in German) is here:

It is easy, and not just with hindsight, to find fault with German strategy in recent years - (whether Germany’s failings are really more egregious than those of neighbors like France and the UK, is a matter for another post). But if you really want to land a knock out blow on the German success story you do not simply argue that they got things wrong with Nord Stream 2. You argue that the entire image of German economic success that has overshadowed Europe in the last twenty years, is a mirage sustained by reliance on cheap Russian gas.

If the recent success of Germany Inc and the social market economy that rests on it, are, in fact, owed to naive deals with Putin, it would force us to rewrite the history of Europe in the last quarter century.

The idea that cheap Russian gas is the secret sauce behind German export success circulates widely in forums like twitter often in explicitly anti-German form. It can also be found in casual throwaway lines, such as the comment by Zoltan Pozsar quoted recently by Rana Foroohar of the FT.

“war means industry”, be it hot war or economic war, and growing industry means inflation. This is the exact opposite of the paradigm we’ve experienced for the last half century, during which “China got very rich making cheap stuff . . . Russia got very rich selling cheap gas to Europe, and Germany got very rich selling expensive stuff produced with cheap gas.”

Schadenfreude aside, there is an obvious appeal to such a narrative. Hubris gets its comeuppance. The unctuous narrative of German superiority through hard work, clean government and frugal living, is turned on its head.

But, is it true? When you start digging, it is striking how little evidence is offered for the “cheap Russian gas” thesis. Of course, high gas prices are currently crushing German businesses and BASF is screaming that the survival of the chemical industry in Germany is in question. Talk of deindustrialization stalks the land.

But it shouldn’t be surprising that BASF is talking its book. And the fact that a historic spike in energy prices causes problems for energy-intensive industries in Germany does not prove that low energy costs obtained by backroom deals with the Kremlin are responsible for the existence of the industry in the first place, or its competitive success in recent year. The influence of the industry and its short-sighted cost-cutting no doubt helped to create an infrastructural dependency, but that tells us little or nothing about sources of competitive advantage before 2022.

As Daniel Gros pointed out in August, if cheap gas from Russia had been a major factor in Germany’s recent economic development you would expect the country to have a high level of gas-intensity in GDP. The opposite is the case. Germany’s gas-intensity of economic activity is about half the global average.

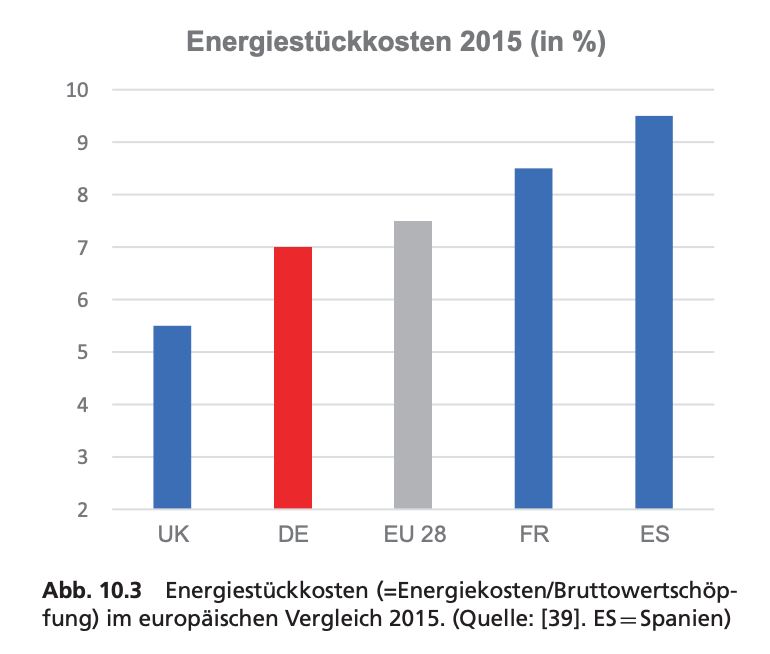

It is less surprising to find that the German economy was quite efficient in its use of gas when you realize that since 2008 gas costs in Germany have been far above those in the US and marginally above the European average. Thank you to André Kühnlenz for this handy graphic.

You can pull the European data from Eurostat here.

It is true that German gas prices are “cheap” compared to what businesses pay in Japan, where all gas has to be imported in the form of LNG. But compared to the bonanza in the United States, German gas prices have never been anything other than expensive.

Admittedly, the aggregate data compiled by Eurostat will not capture the kind of premium deal that a customer like BASF can command from its favored collaborator GAZPROM. So, let us allow that German industry may on average achieve somewhat better prices than the European average, how much difference could this possibly make to the competitive position of its exporters?

First of all let us remind ourselves of the structure of German exports.

Unsurprisingly, German comparative advantage is not generally in sectors where cost is the dominant factor. But, cost is always one element in a deal. However high the quality of German goods, the price matters. So, how big an issue are energy costs for Germany’s industries, not in an extreme year when gas prices have gone through the roof, but in the normal times before 2020 when Germany racked up its triumphs as the export champion of the world?

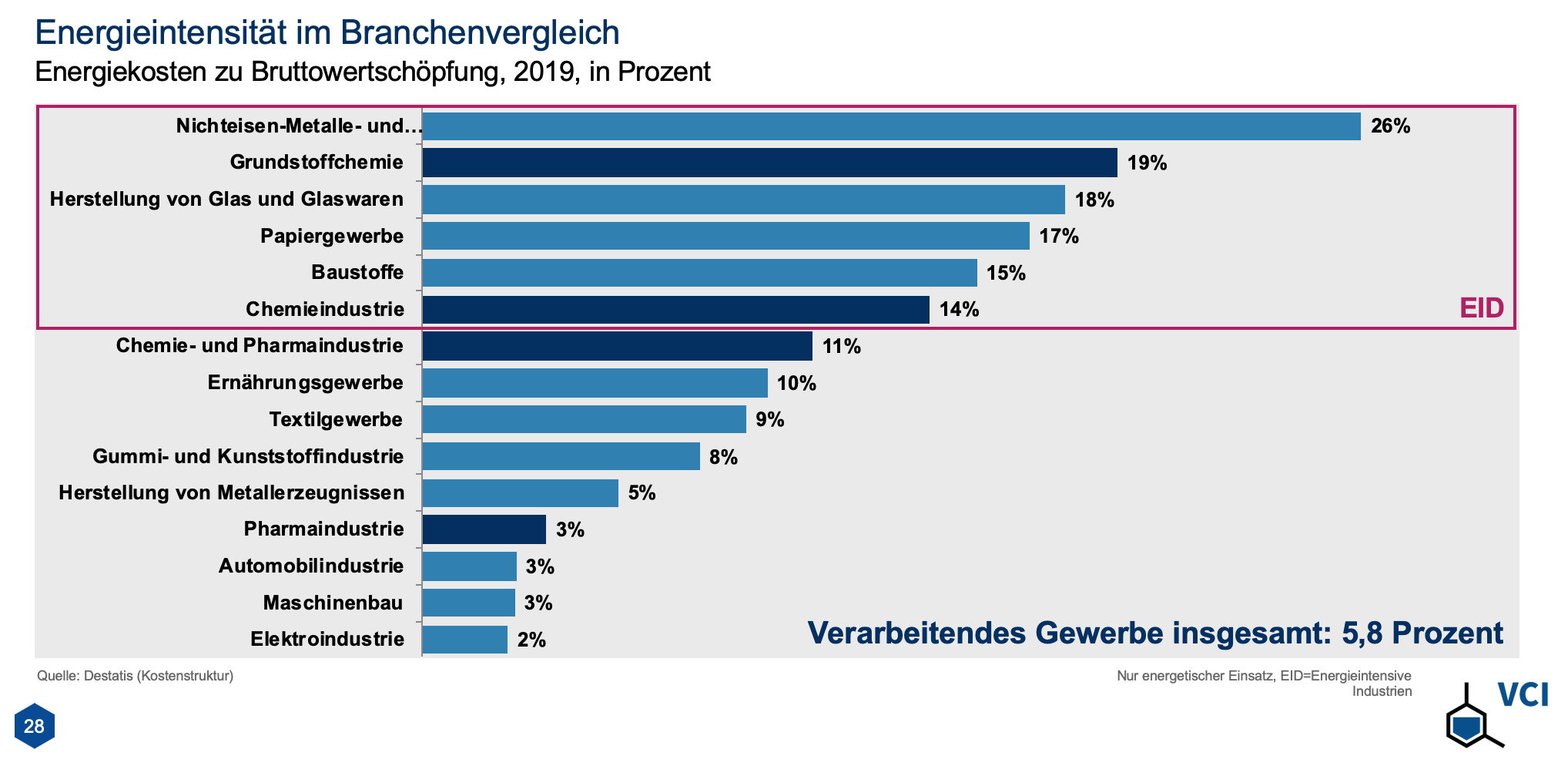

Figures for energy intensity are very revealing.

Source: VCI

For German manufacturing industry as a whole, energy costs amounted to 5.8 percent of gross value added. In the leading export sectors like motor vehicles and engineering the share was 3 percent. Though gas and electricity are indispensable and you cannot operate industrial processes without them, like other essential inputs such as protein and calories, greater and greater efficiency mean that energy accounts for a small and diminishing share of industrial costs.

Nonferrous metals was the most energy-intensive sector in Germany. It accounted for about 6 percent of exports. Chemicals, where energy costs accounted for 14-19 percent of gross value added, was responsible for roughly 10 percent of exports.

Obviously, with current energy prices at their shocking levels, both those sectors, along with the paper industry are under intense pressure. The situation of the chemicals industry, where gas is used not only for energy production but also as a feedstock, is particularly difficult. But in more normal times, even if we allow that Germany benefited from discounts on Russian gas, how much difference is that likely to have made to sectoral competitiveness on global markets, let alone German industrial export performance overall. What are in play are at most a few percentage points of value added.

Interestingly, in 2015 the well-respected Frauenhofer Institute did a series of in-depth studies on the sensitivity of production and employment in German industry to energy prices. At the time the question that concerned them was the impact of removing the privileges provided to export-exposed industrial companies in Germany’s electricity pricing system. This is interesting not because it directly addresses the question of Russian gas, but because it allows us to gauge the amount of support provided to Germany’s most favored industrial sectors by exemption from electricity levies. The result of the Frauenhofer study was surprising mainly because the estimated impact was so small. All told the economists suggested that raising industrial electricity prices to the level paid by household and small businesses might cost 4 billion in exports and 15,000-45,000 jobs, of which at most 35,000 would be in manufacturing industry. In light of that fully worked out macroeconomic assessment, how large would we expect the effect of a putative “cheap Russian gas”-subsidy to be.

Taking energy costs as a whole in relation to gross value added across the entire economy, Germany before the crisis was certainly in a somewhat favorable position relative to its European neighbors, but by no means in a league of its own. And it enjoyed that position not because of lower energy costs but because of greater efficiency in the use of energy.

Try one last thought experiment. In light of the chart above, do low energy costs help explain the success of UK manufacturing in recent years? Or, if you prefer the comparison, does Italy’s heavy reliance on Russian gas, second only to that of Germany, explain the performance of its exports since the early 2000s? Neither question suggests a plausible narrative and we should avoid drawing simplistic conclusions in the German case as well.

In the genre of Fin-fiction, the story of German exporters suffering their comeuppance at the hands of bad king Putin, is more a morality tale than convincing economic analysis.

German energy policy has been a disaster. There is no reason to pile on with exaggerated claims about the economic significance of cheap Russian energy imports.

This thread by Miłosz Wiatrowski-Bujacz makes the point very well:

It wasn't "naive". Germany could have a functional economy, or it could have NATO expansion. It tried to have both, and when these conflicting agendas came into conflict, they chose poorly.

Now EU will spend $1T to enforce an agenda that consists of NATO expansion, and no federalism for Ukraine.

But hey, NATO was irrelevant 15 years ago and NATO is not irrelevant now. The US sickness for pursuing military solutions to adult problems has a new constituency.

Strategic snare? While definitely not the only source of German economic success, having reliable, cheap source of energy and predictability of prices through longer term contracts made (and still makes) perfect economic sense and immensely benefited German economy. Soviet Union / Russia delivered without missing a beat for 40+ years through all the geopolitical turmoil and numerous provocations that invariably came from the West (ridiculous Skripal and Navalny affairs come to mind).

In the current crisis the EU political class proved itself to be:

(a) pathetic hypocrites because they never sanctioned Saudi Arabian oil no matter how many Yemenis they bombed or starved with their blockades, this way they also exposed their own deep racism as obviously for these beacons of liberal values blond European lives are infinitely more important than brown Arab ones.

(b) compradors, not better than ones in Columbia or Guatemala - working in interest of US but not their home country or EU as a whole. It was entirely predictable that sanctioning / boycotting Russian gas (and other commodities) will cause economic and social hardship, yet none of these geniuses wanted to seriously engage either on Minsk I or II, or in December of 2021 when Russia offered a new European security architecture with NATO which would have prevented the war, they dismissed it and openly mocked it.

(c) plain morons - take for example Ursula Von den Leyen's recent tweet how Ukraine will supply EU with electricity this winter, alleviating the energy crisis in EU while providing much needed funds for bankrupt Ukraine. Well, Russian reply didn't come through twitter but they promptly blew up CHPP-5 (biggest combined coal power and heating plant in Ukraine, finally taking a page from NATO playbook against Serbia, Libya, Iraq) giving the clear message that if soon EU doesn't push Ukraine towards some negotiation, this winter EU will have to supply Ukraine with some power, in addition to provide for even more refugees from frozen lands.