Buybacks over investment in the US military-industrial complex. The Indian economy shifts gear. RAND on burden-sharing & Britain's wars of decolonization.

Great links, images, and reading from Chartbook Newsletter by Adam Tooze

Thank you for opening your Chartbook email..

Enrique Echeverría, “La niña y las brujas - Grupo Milenio”. Source: Excelsior

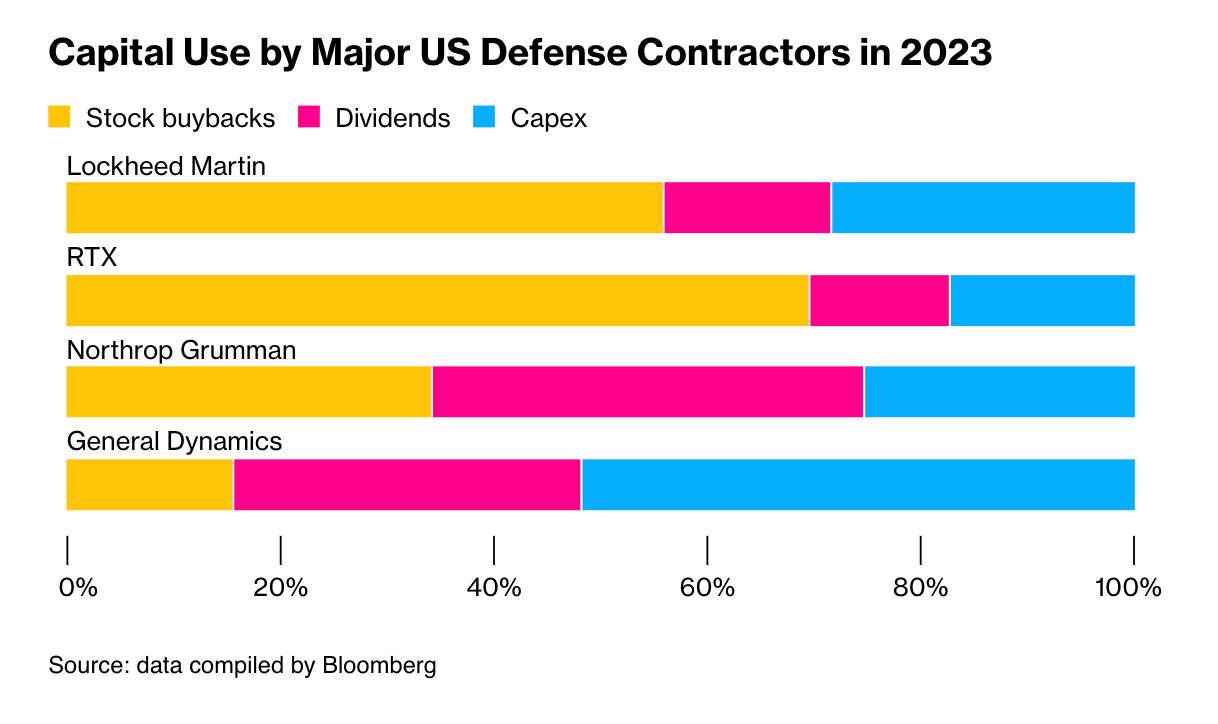

“The US defense industry is a bigger risk to America’s security and the credibility of our deterrence than China is,” Rahm Emanuel

American defense companies are hurting the nation’s security interests by prioritizing share buybacks over delivering weapons to the US military and its allies, according to the outgoing US envoy to Japan. Ambassador Rahm Emanuel said the firms are more focused on increasing their stock value than on investing in production capacity. This has contributed to delays in weapons shipments, which could harm US security and weaken American alliances, he said in an interview on Wednesday. “The US defense industry is a bigger risk to America’s security and the credibility of our deterrence than China is,” Emanuel said in Tokyo. … “I can’t tell you how many times here I’ve had to use my political capital to cover for their failure,” he said. One solution — he added — would be to ban defense contractors from buying back their own stock for several years if they fail to deliver orders on time.

In 2023, Lockheed Martin and RTX spent a combined total of $18.9 billion on stock buybacks, compared with just $4.1 billion on capital expenditures, according to data compiled by Bloomberg. .. Limits on manufacturing capacity and lengthy administrative procedures have also caused delays in delivering US defense equipment to allies such as Japan and Taiwan. The total value of arms purchased from the US but not yet delivered to Taiwan was estimated at $21.95 billion as of November, according to Cato Institute, a US think-tank.

Source: Bloomberg

HEY READERS,

THANK YOU for opening the Chartbook email. I hope it brightens your day.

I enjoy putting out the newsletter, but tbh what keeps this flow going is the generosity of those readers who clicked the subscription button.

If you are a regular reader of long-form Chartbook and Chartbook Top Links, or just enthusiastic about the project, why not think about joining that group? Chip in the equivalent of one cup of coffee per month and help to keep this flow of excellent content coming.

If you are persuaded to click, please consider the annual subscription of $50. It is both better value for you and a much better deal for me, as it involves only one credit card charge. Why feed the payments companies if we don’t have to!

And when you sign up, there are no more irritating “paywalls”

China continues to flirt with deflation

For contributing subscribers only.

“Do not be fighting the last analytical war” Anatole Kaletsky’s four big questions about 2025

In thinking about 2025, it therefore seems necessary to focus on the unprecedented uncertainties of economic policy and geopolitics—the “known unknowns” that could transform investment conditions in the years ahead—rather than betting on market mispricings of economic data that reflect the now-irrelevant policy environment of the last few years.

Will Trump prioritize tariffs and deportations, or growth and inflation?

Will China and Japan decisively accelerate economic growth?

Will Europe abandon its budgetary rules and try a US-style fiscal expansion?

Will ending the wars in Ukraine and Gaza produce a global “grand bargain,” involving not just geopolitics but also energy, trade and finance?

Source: Gavekal

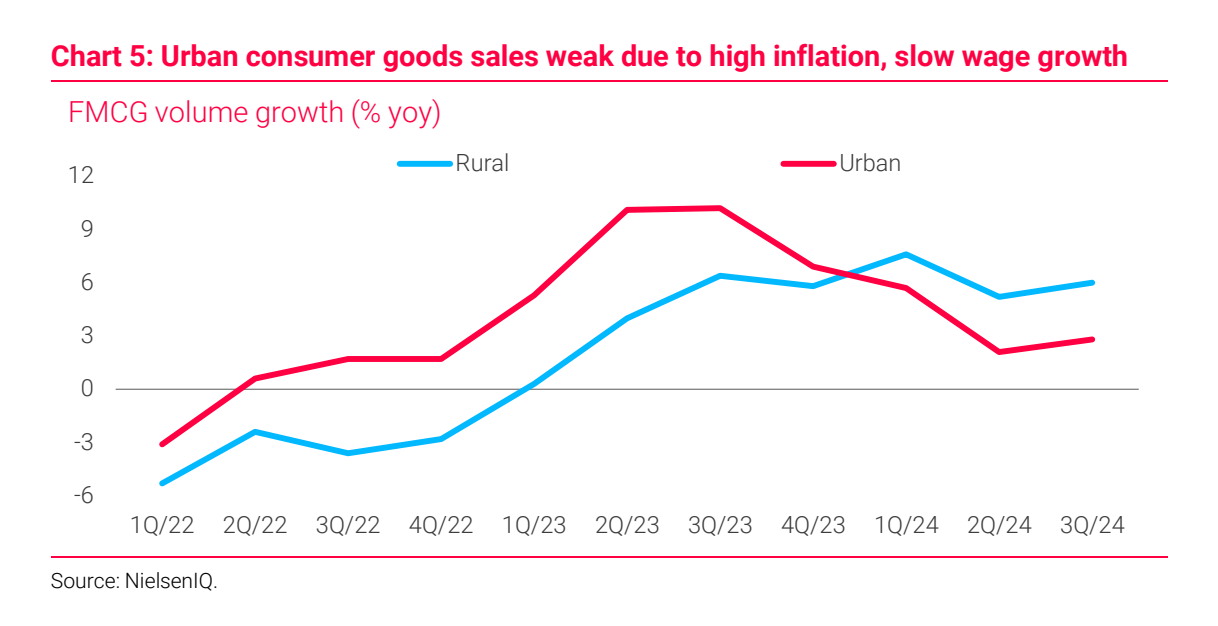

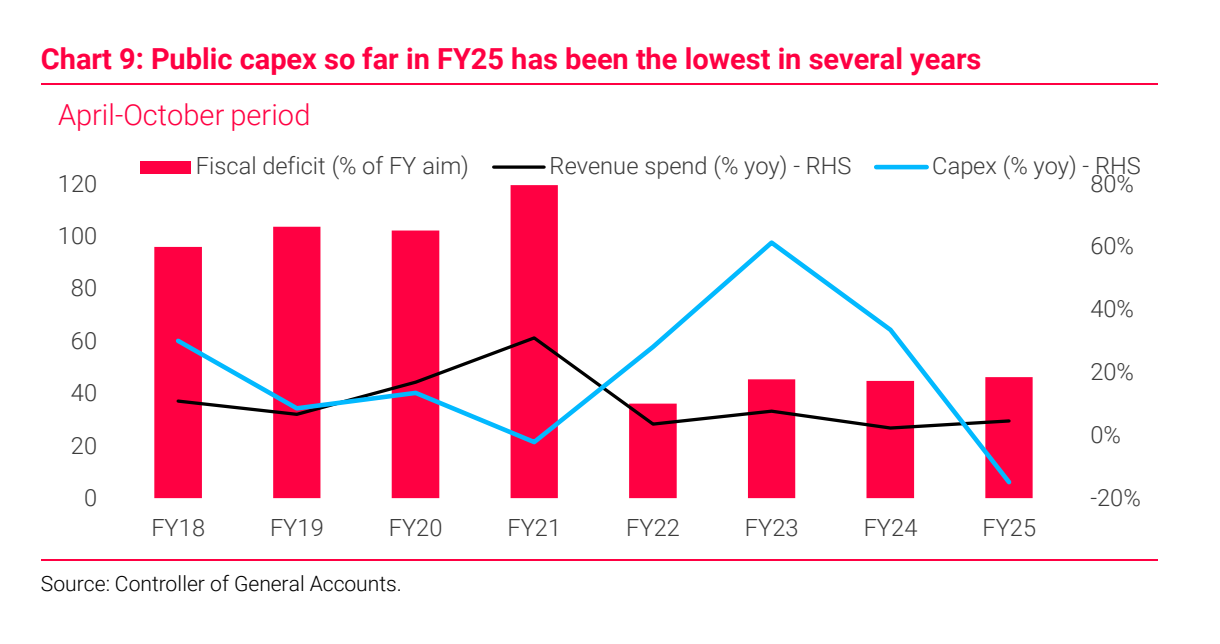

If Indian growth is slowing this is driven above all by a cooling off of the urban economy.

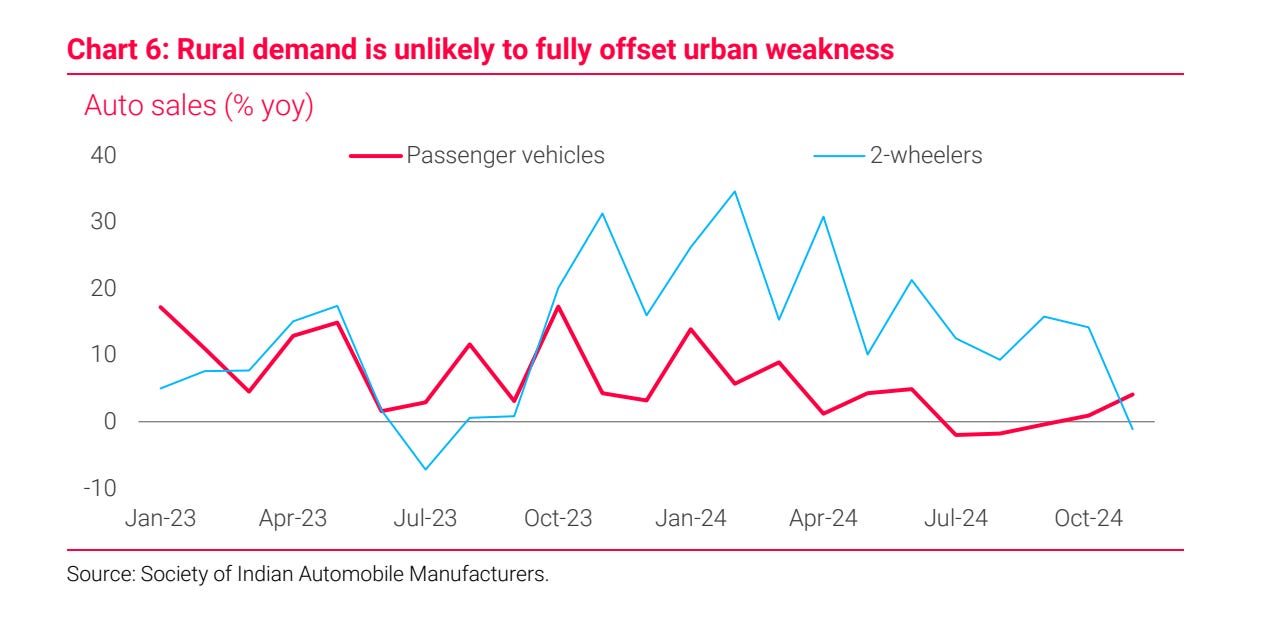

The hope is that rural demand will offset urban weakness. But the signs from the rural economy are not encouraging with demand for entry-level vehicles falling.

Public capex, a key growth multiplier in recent years, slowed sharply in the first 7 months of FY25 due to interruptions from elections and heavy rains. ◼ States mirror central trend of slower public capex; meanwhile, welfarism is on the rise with 9 states undertaking cash transfers for women voters in FY25

Source: Shumita Deveshwar in Global Data

Enrique Echeverría, “Crepúsculo” (1968).

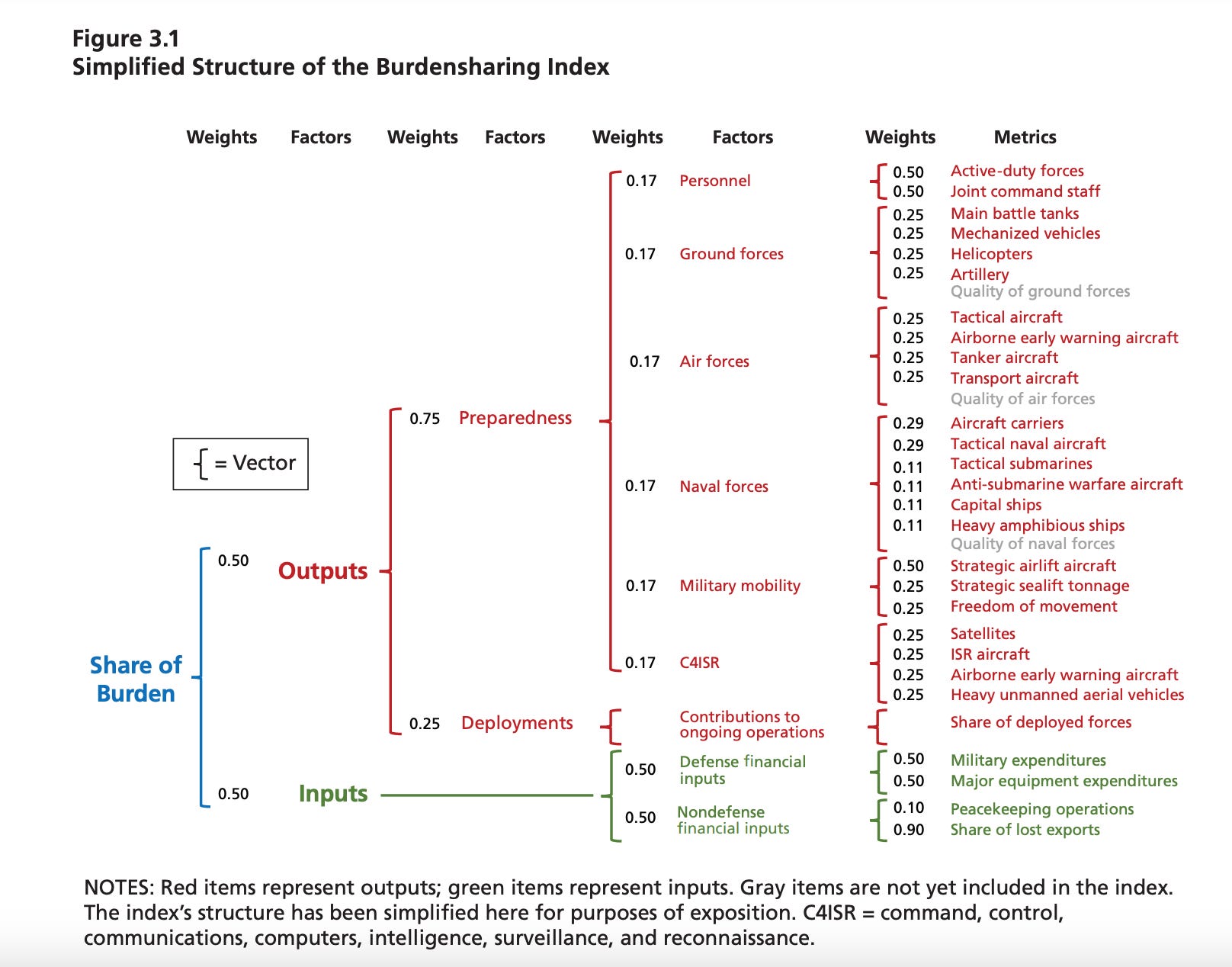

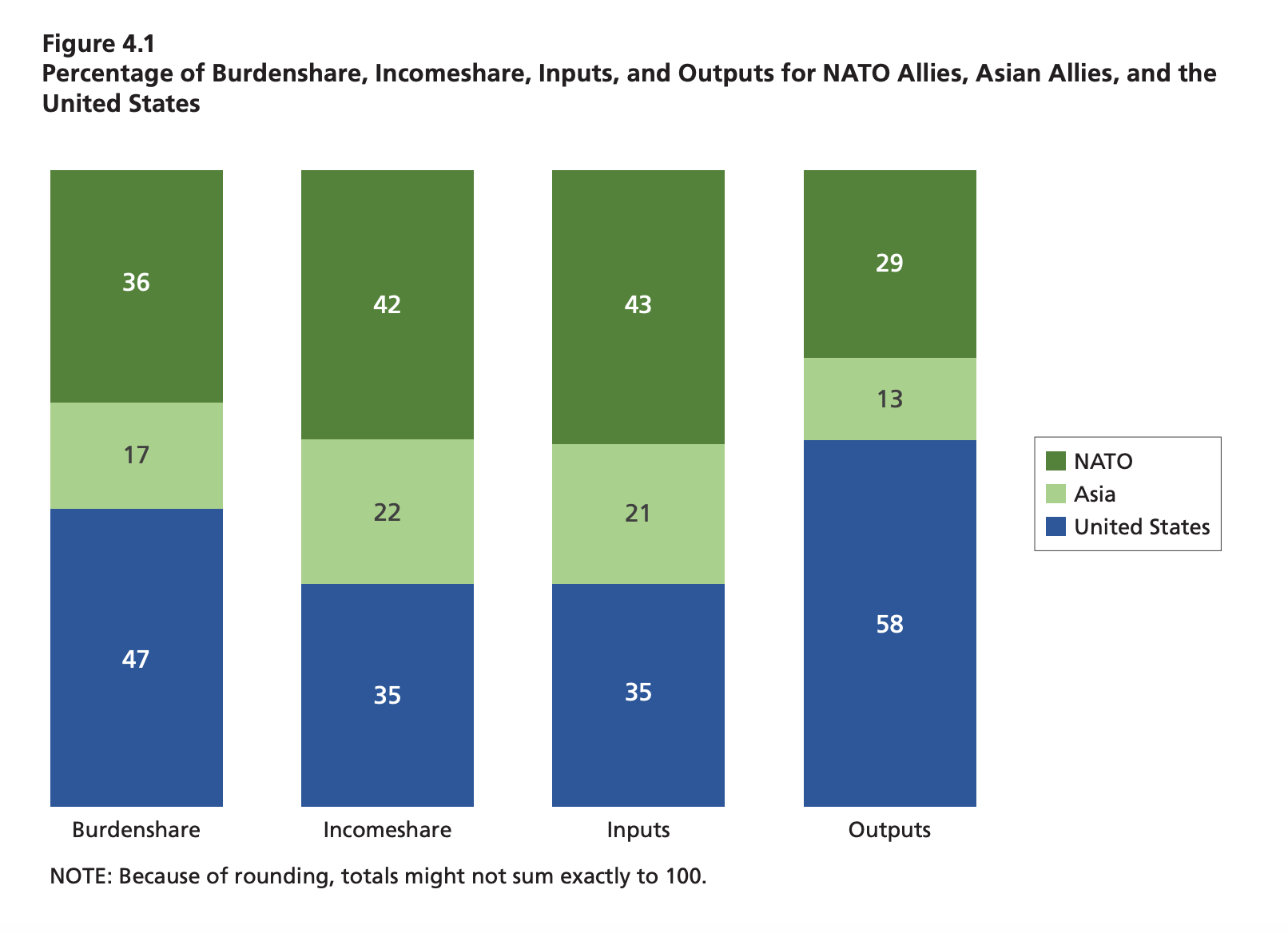

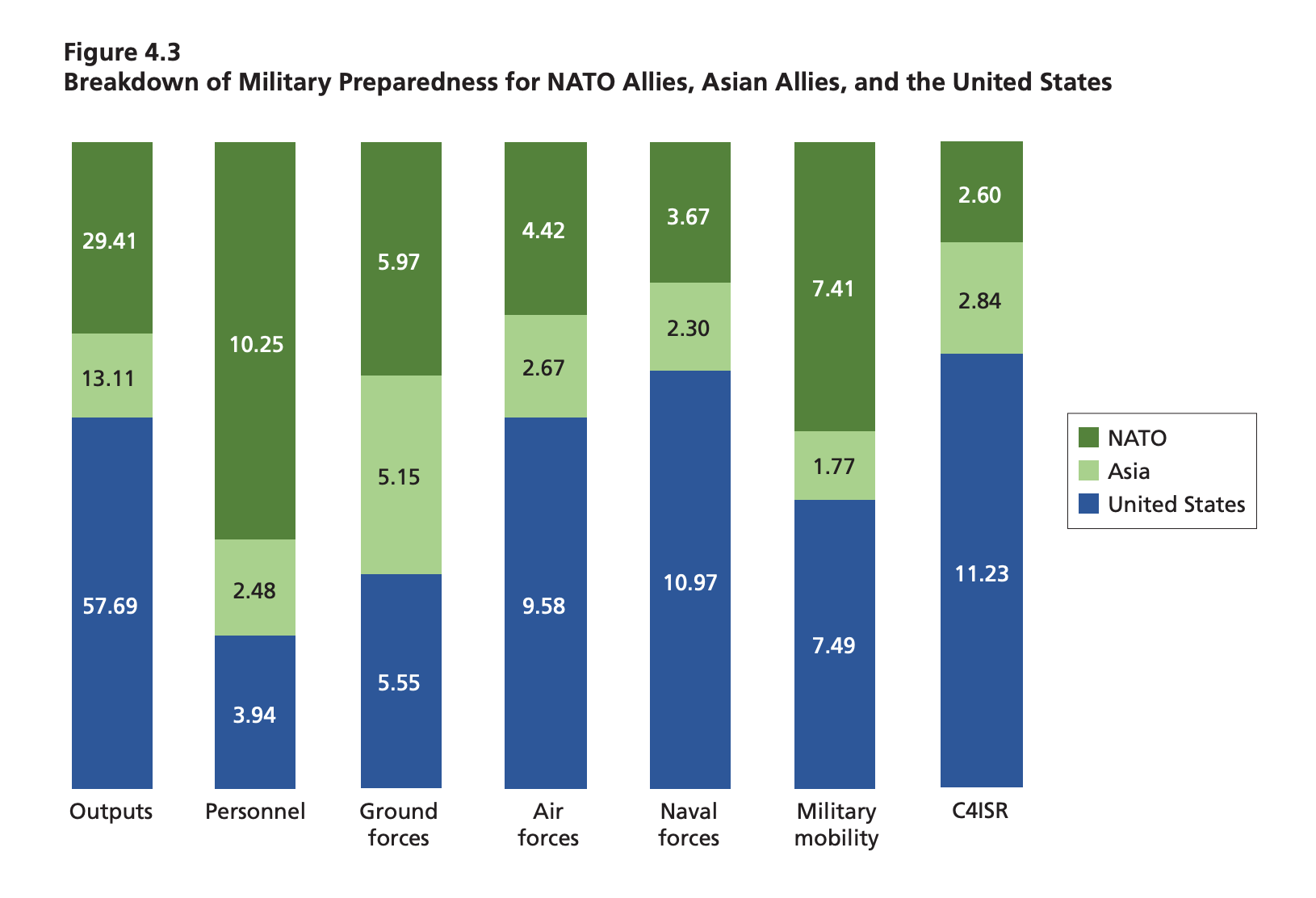

Forget 2 per cent — there is a better way to measure global security contributions King Mallory

In a report for the Office of the Secretary of Defense, Rand calculated the security-oriented contributions and capabilities of our global alliances, from submarines to satellites. We counted every tank, tanker and tactical aircraft. We included total defence spending, but also contributions to peacekeeping missions and the costs of enforcing economic sanctions. When we recently updated and re-ran the numbers from our original 2017 report, we found that the US share has been decreasing since the end of the cold war, when it stood at 53 per cent. By 2023, it was around 39 per cent. That’s not a small number — but it’s also not a flashing red sign that we’re being taken to the cleaners. The other Nato countries accounted for an almost equal share, 38 per cent. Asian countries provided another 13 per cent, and allies in the Middle East and South America provided the remaining 10 per cent. That answers the big question: “What can each ally bring to the table in time of war?” There’s a related question, of course: how much should each ally provide, given the size of its economy? To get there, we divided each country’s share of the collective defence burden by its share of total allied GDP. Anything over 1 meant that a country was bearing its fair share, measured in capabilities, not just spending. Nineteen countries met that mark in 2023. The US at 1.07 trailed Nato, whose ratio stood at 1.10, and was just ahead of France and the UK. Eastern European nations were among the top performers — no surprise, as they watch neighbouring Russia brutalise Ukraine. But Greece, Italy, Poland and the Netherlands were up there, too. South Korea also stood out, despite US claims a few years ago that it was shirking its defence obligations. This ratio is one way to identify countries that could be doing more. Canada needs to double its defence spending to reach Nato’s target. Slovakia is far behind its neighbours in central Europe. Australia and Brazil should be able to afford more of the collective defence burden. A surprise appearance among top contributors was Spain. It has one of the lowest defence spending rates in Europe, well below Nato’s target. But according to UN Comtrade data it has suffered in enforcing economic sanctions against Russia, losing more than $10bn in exports since 2018.

Source: Financial Times

RAND’s remarkable study of burden-sharing within the Western alliance

Source: Rand

Breaking down burdensharing

Where the soldiers went.

“Colonial violence was a fact of life in postwar Britain.” So begins the third paragraph of Age of Emergency: Living with Violence at the End of the British Empire, Erik Linstrum’s detailed and often painful study of the colonial wars in Cyprus, Kenya, and Malaya—with occasional forays into Palestine and Ireland—that scarred those landscapes and peoples indelibly. This was the era of decolonization, and these were among the many colonies—not just British—that in the decades following the Second World War successfully, if at huge cost, threw off the yoke of European colonialism. Successive British governments deployed brutal military tactics to quell anti-colonialism, wiping out entire villages, destroying food crops, establishing detention camps, and killing indiscriminately. Linstrum’s aim, in this fascinating book, is to demonstrate both the widespread acceptance by the British public of both the need for such campaigns and the use of violent tactics and the numerous voices of dissent that quickly emerged to question them.

Source: Philippa Levine on Erik Linstrum. Age of Emergency: Living with Violence at the End of the British Empire., The American Historical Review, Volume 129, Issue 4, December 2024, Pages 1825–1826.

Enrique Echeverría, “El umbral de lo abstracto - Museo de Arte Moderno”

Source: Chapultepec

If you’ve scrolled this far, you know you want to click: