America's big spending, German weapons, consolidating Permian & Kant and global chaos

Great links, images and reading from Chartbook Newsletter by Adam Tooze

Superstudio, Supersurface Sunset, 1971. Describing this radical Italian collective as “architects dreaming of a future with no buildings,” the New York Times has this excellent profile of Superstudio, stressing their place in a radical 1960s-70s generation:

The starting point of everything Superstudio did was dissatisfaction with the uniformity of modern architecture, which its left-wing members saw as an instrument of capitalism that disempowered the masses, robbing them of their individuality and freedom. Sometimes, they made fun of the status quo, or took it to absurd conclusions; other times, they imagined utopian futures.

Much of the best content is for the subscribers’ club only - join now here:

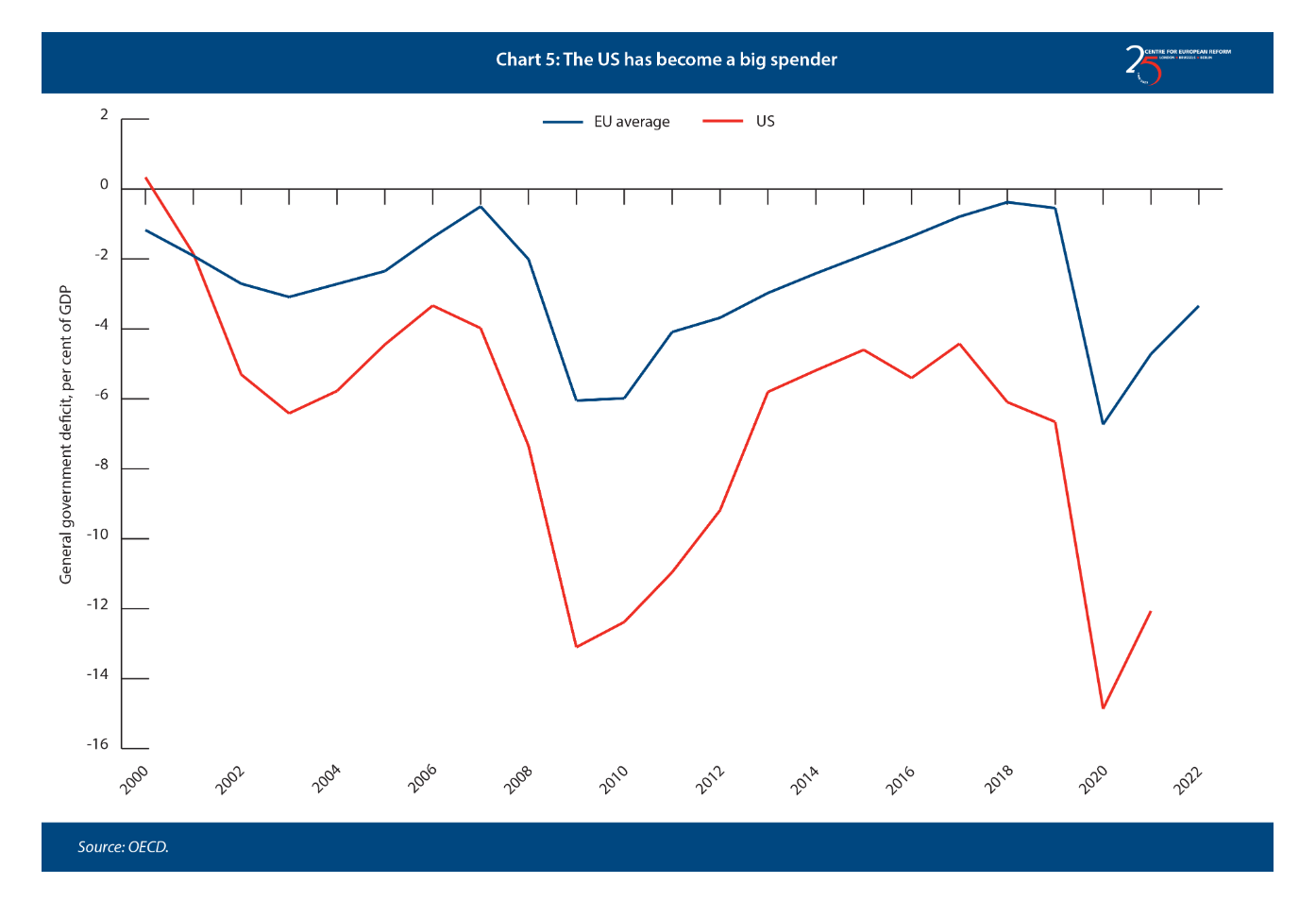

The trans-Atlantic fiscal difference

This jars with some of American anti-state ideology, you might think, but in fact fits with the grandiosity of imperial prowess and capitalist growth:

…the US has for the last 20 years consistently run a much more aggressive fiscal policy than governments in Europe, with larger deficits in normal times and significantly larger responses to both the GFC and Covid. After the GFC – and even during the eurozone crisis, which started in 2010 – European countries reduced their budget deficits, sharply curtailing growth, particularly in 2010-13. Meanwhile, in the US the general government deficit stabilised under Obama’s second term and then started growing again under Trump. Thus, by 2019 European countries were on average close to a balanced budget while the US ran a deficit of more than 6 per cent of GDP. Following the Covid crisis, the US unleashed a much larger stimulus package, combined with a series of expensive spending programmes such as the CHIPS Act and the Inflation Reduction Act.

Source: Centre for European Reform

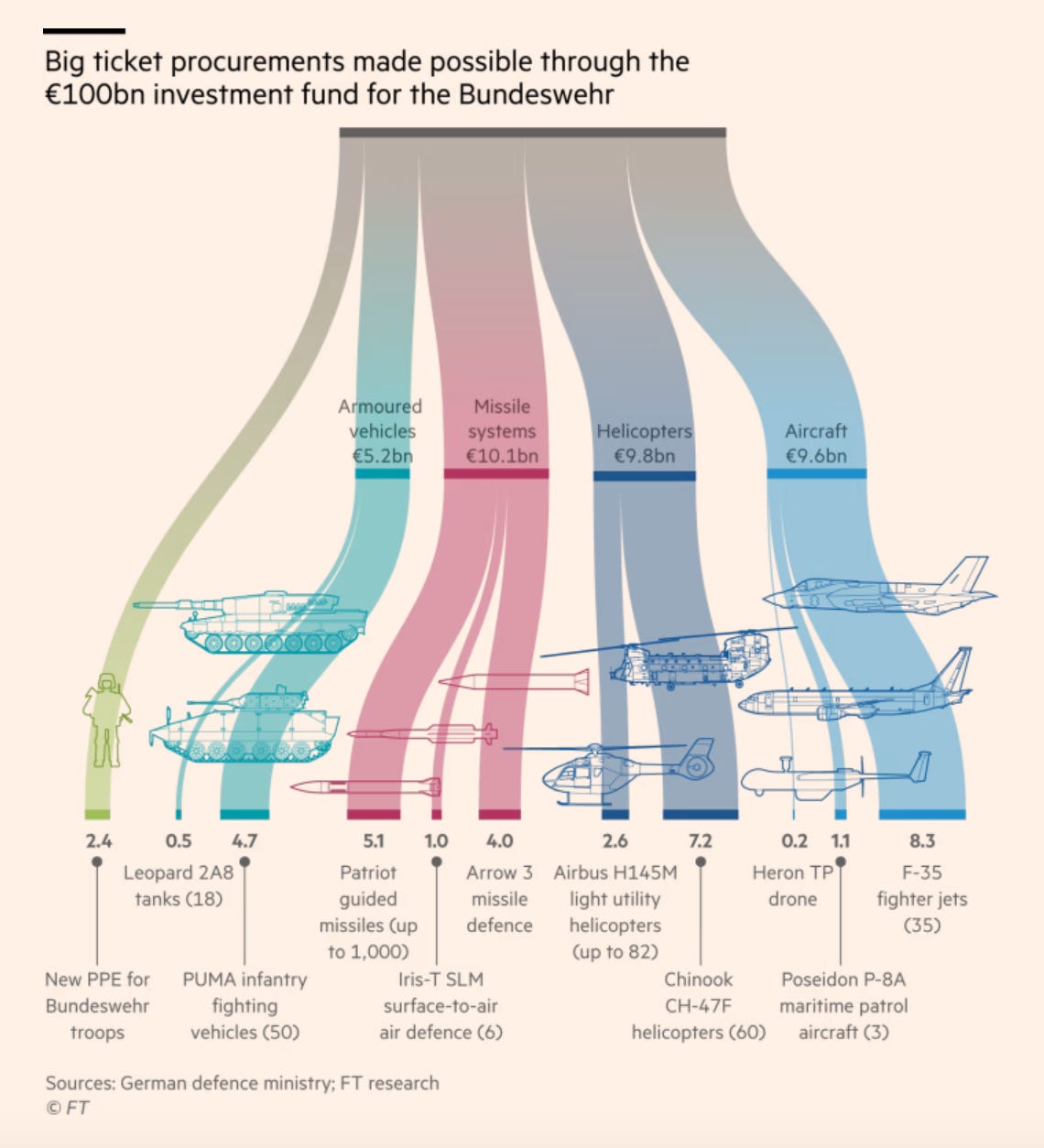

Bundeswehr procurement

Since the war in Ukraine began, it has significantly exacerbated the militarisation of the European Union, including its most powerful member with (supposedly!) the most hang ups about militarism:

Source: FT

How Indonesian investors picked up the capital-market slack

As foreign investors withdrew from Indonesian assets during the covid shock, the domestic ownership share of government bonds rose to 85.7 percent by end November, up from 80.9 percent in early 2022, and far above the pre-pandemic share of 61.4 percent in early 2020:

Source: World Bank

Chinese firewalls - a growing story

Subscribers only.

This newsletter takes time to write and is only possible because of paying supporters. For analyses like today’s focus on China-Hong Kong relations, changing natural gas markets and how racism structures municipal bonds in America, subscribe now:

Where is Germany now getting its gas from?

Subscribers only.

Consolidating Permian

The shale revolution that began about 15 years ago saw a proliferation of thousands of small-time drillers turn the global energy order on its head and restored the US to the status of world’s biggest producer. Today, as a multibillion-dollar wave of consolidation washes over the Permian Basin — the engine room of America’s oil industry — that landscape has been transformed. A handful of heavy hitters is now firmly in control. Diamondback Energy’s $26bn deal for rival Endeavor Energy this week brought to almost $180bn the value of an oil and gas dealmaking spree that has reverberated across the US shale patch since the beginning of last year as big, publicly listed players swallowed rivals. Just 10 companies will now control more than 6.4mn barrels of oil equivalent a day of the Permian’s output, according to Wood Mackenzie, a consultancy. Six companies will each produce more than 700,000 boe/d — more than some Opec member countries.

Half of the sought-after Midland sub-basin, which makes up the eastern part of the Permian, will be controlled by just two companies: ExxonMobil and Diamondback. In the past four months alone, Exxon has announced a $60bn deal for Pioneer Natural Resources, the biggest producer in the Permian; Occidental has agreed to snap up CrownRock for $12bn; and Diamondback announced its purchase of privately held Endeavor. (Another pending $53bn deal by Chevron for Hess gives the supermajor shale assets in the vast Bakken oilfield of North Dakota.) Over the past five years, under pressure from Wall Street, publicly owned companies have pulled back from the costly pursuit of volumes and sought to channel cash back to shareholders. Private operators — less constrained by market demands — drove much of the Permian basin’s growth, responding to higher prices by rapidly raising production. Now, as those companies are absorbed by larger public rivals, the potential for surges has faded once more. Diamondback said it would remove drilling rigs from the field after its acquisition, while insisting it could keep gradually growing output regardless. That adherence to strict exploration plans suggests the US shale energy industry will shift further away from its role as a swing supplier, able to quickly turn up the production dial to douse price rises as it did early in the boom. Consolidation will, however, enable producers in the Permian to remain profitable even during commodity slumps. Wood Mackenzie believes operators can shave about $5 a barrel off the break-even costs of drilling that sit at about $30-$35 a barrel in the basin. West Texas Intermediate crude settled at $78 a barrel on Tuesday. One way of driving down costs is by joining together nearby acreage, enabling companies to operate across large swaths rather than piecemeal parcels. They can extend the length of horizontal oil wells they drill and centralise their infrastructure above ground.

Source: FT

Kant and global chaos

Subscribers only.

How racism is built into a quiet but totally crucial corner of Wall Street

Subscribers only.

Superstudio, Atti Fondamentali. Vita - Supersuperficie. Pulizie di primavera, 1971